2025 Letter to Readers

5 Key Lessons of the Year, 3 best Ideas Currently and Portfolio Results.

Last year, we shared five key lessons from the year and presented an investment idea we had just initiated ourselves — Medistim. While we can’t promise that this year’s idea will match Medistim’s +70% return, we hope this letter is still an enjoyable read.

As Christmas is a time for tradition, we’re keeping a similar format this year, albeit with new lessons and a new idea. Remember, nothing I write constitutes investment advice. Please do your own due diligence.

We would also like to extend a sincere thank you to everyone following along. The chart below shows the growth in followers on this Substack since we started in 2023. This is a hobby project for us, which we enjoy a lot. Our full-time work now involves operating two small private companies, and we hope to bring the lessons learned from running them back into our greatest passion: investing.

5 Biggest Lessons this Year

1) Don’t drive looking in the rearview mirror

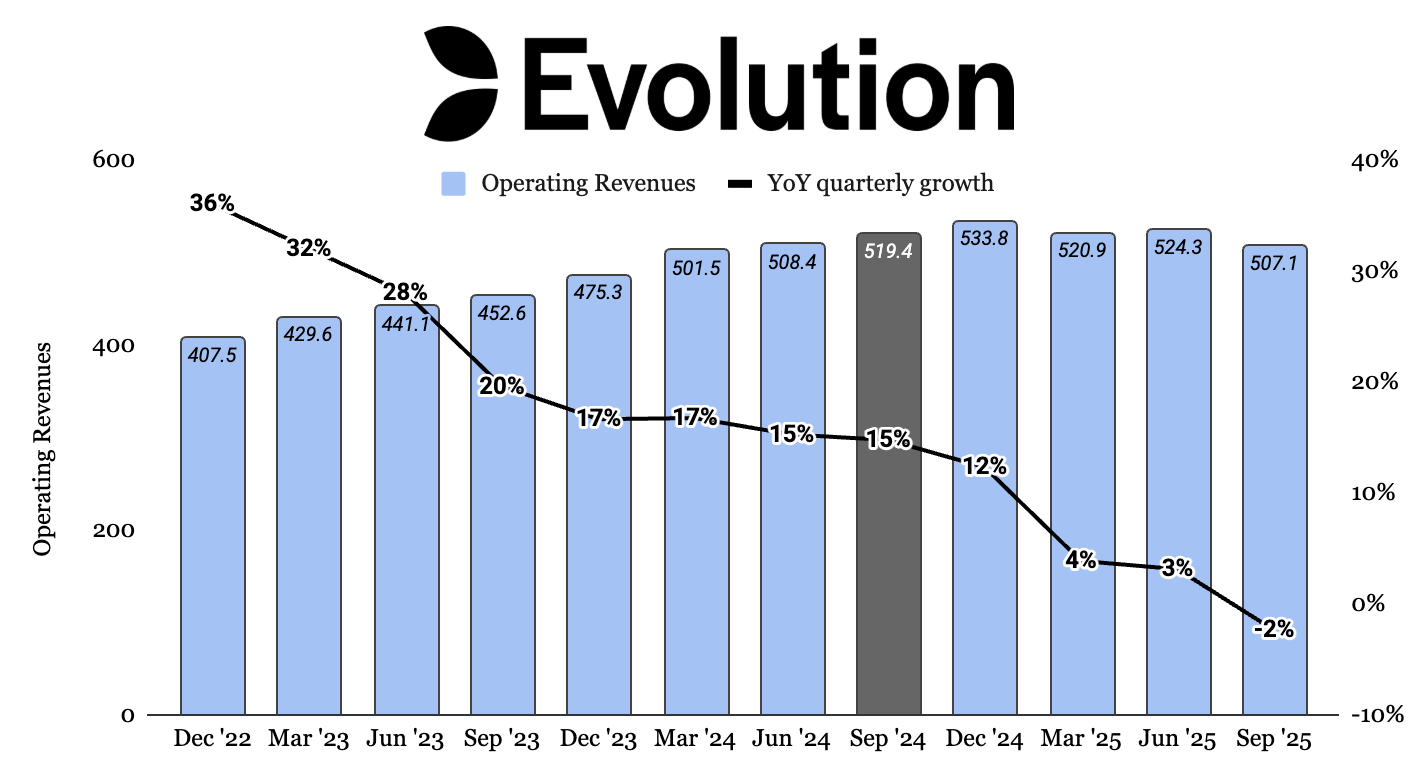

Our biggest mistake this year was Evolution AB. We bought in late 2024, impressed by strong past results, a historically cheap ~15x P/E, and a high dividend + buyback yield — assuming growth might slow from the then 15% rate, but remain solid.

Several risks were already visible at the time, but we had not done the depth of work required to truly understand them. Instead, we relied to heavily on strong past performance, giving us unwarranted confidence that the business would largely continue its historical growth trajectory, albeit at a slower pace.

Lesson learned: By overweighing historical results, we underestimated forward-looking risks and overestimated our understanding of the business. While the stock may work from here, we acknowledged how wrong our initial analysis was, and therefore concluded to sell it. We also recognized that rapid growth often carries lagging risks, which proved to be employee dissatisfaction and security weakness.

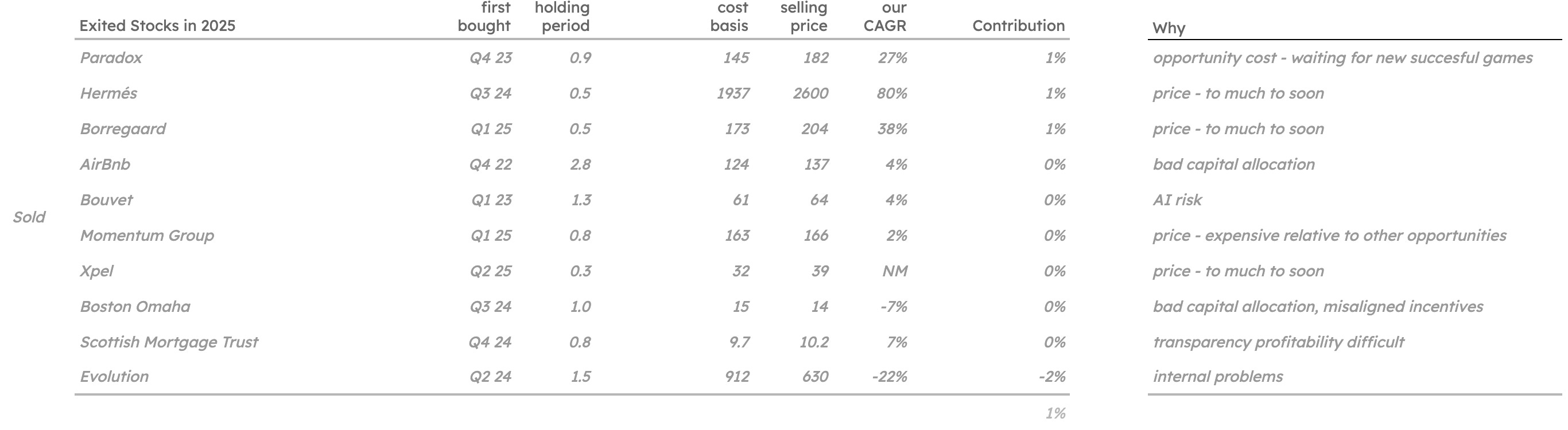

Evolution ultimately contributed –2% to our Total Invested Capital, as shown in the table of all exited positions below. Despite this, the aggregate result from all exited positions this year was +1%, helped by Hermès, Paradox, and Borregaard.

Looking at the number of exited positions above, we had unusually high turnover this year, but all these holdings were relatively small at less than 5%.

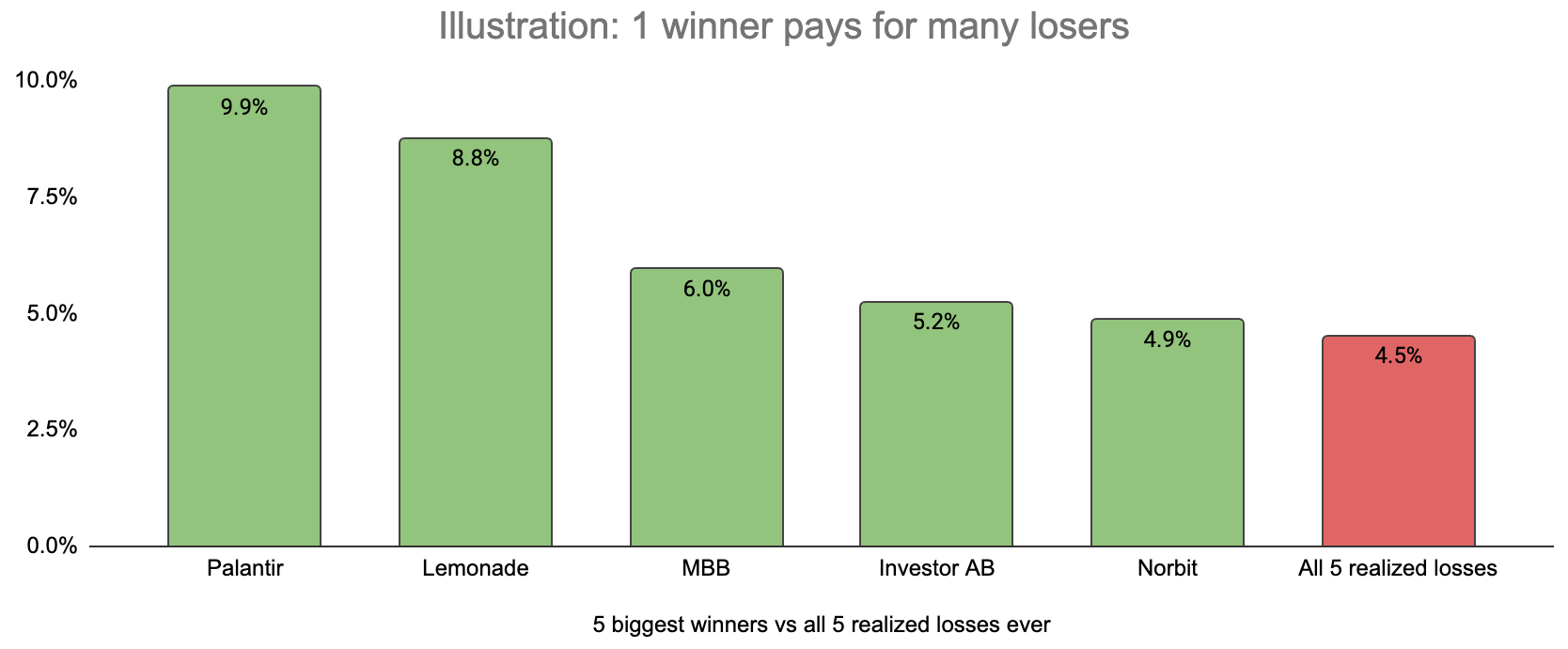

2) One winner pays for many losers

Evolution now ranks as our biggest realized loss to date. Still, as the Exhibit III illustrates, a single large winner can more than offset all our realized losses to date. We have exited 19 stocks in total since we started investing late 2021. You can see the assymetry of investing starting to show itself in the return contribution from our 5 biggest winners to date, versus our 5 losers.

This underscores a core principle of portfolio construction: long-term returns are driven by asymmetry. If you can consistently avoid large permanent losses (>50%) while allowing a small number of positions to compound meaningfully, the winners will largely determine overall returns.

One approach is the venture-capital model—small allocations across many highly speculative bets. However, we believe superior risk-adjusted returns are more often achieved by prioritizing downside protection while allowing upside optionality to run.

Accordingly, we look for businesses with some form of downside protection: robust balance sheets, durable unit economics, and business models that reduce the risk of catastrophic loss. Certain business models are particularly well suited to this, a topic we will return to in the next lesson. REQ Capital, for instance, has previously highlighted Programmatic Acquirers as an attractive example.

3) Serial Acquirers = low risk, high return business models?

That said, the Serial Acquirer space has become increasingly crowded, making valuation risk a central concern. Even over long horizons, this matters. A multiple compression from 30x to 20x P/E translates into roughly a 4% annual headwind over ten years—longer than most investors’ actual holding periods.

By contrast, Holding Companies — with fewer, larger acquisitions (think Berkshire, Fairfax, Brookfield, Investor AB, Scottish Mortgage, MBB) — have historically traded at persistent discounts to the market. Even after doubling recently, MBB trades around 13x P/E adjusted for net cash and significant NAV discounts, which we view as undemanding given its track record.

We find this structure compelling, with a great example being Scottish Mortgage Investment Trust — participating in upside from a number of exceptional investments (e.g. Amazon, Nvidia, SpaceX) with diversification protecting the downside.

We recommend Tresor Capital if you find interest in Holding Companies.

4) Acquired vs Organic Growth

It seems to us many investors view organic growth as “free”.

While that may be true for your toll-booth business model (think Visa), most companies are not like this. Most companies need to reinvest capital to grow.

With hindsight, reinvestment stories like Amazon and Constellation Software look obvious. In reality, their peak reinvestment years showed little free cash flow (measured as operating cashflow - investing cashflow) and muted reported profits, weighed down by depreciation, amortization of acquired intangibles, and heavy spending on growth. Yet, both returned exceptional long-term returns. We believe the key was not to see whether growth was acquired or organic, but rather how much capital was invested and what returns those investments made on aggregate.

To us, it seems investors looking at Shift4 would prefer their Capital Allocators to build a factory for $1,000 rather than acquire the exact same factory for $500.

With Shift4’s strong multiple contraction in recent years, we think the market is telling us they disagree with how Shift4 management goes about growing their business. We think studying the playbook of Constellation Software, shows where to look.

The previous CEO of Constellation, Mark Leonard, previously stated that they noticed better returns from acquisitions than organic reinvestments. In essence, they are agnostic to the source of growth — they care only about the return. This probably also means there may come a day when they shift their investment spend towards more organic initiatives, if they see that offers more potential.

We believe Shift4’s management team operates under a similar philosophy, but with a different growth playbook. Their primary objective is to scale their payment offerings across as many merchants as possible, but their method of customer acquisition (CAC) is unconventional:

The Traditional Friction: Competitors often rely on broad marketing campaigns to convince individual hotel or restaurant owners to replace their entire infrastructure — which could be a high-friction, low-conversion process.

The Shift4 Shortcut: Instead of “hunting” merchants one by one, Shift4 acquires entire customer cohorts by purchasing companies that solve a single piece of the merchant’s puzzle (e.g., a specific software tool or giftcard solution).

The Cross-Sell Engine: Shift4 lowers its CAC and gains a “warm” lead. They found it far more efficient to cross-sell a broad payment suite to an existing customer than to acquire a new one from scratch.

And with Shift4’s heavy acquisition spend in recent years, most recently with the luxury retail giant Global Blue, they now have a simpler avenue to grow “organically”. And they can benefit from the existing relationship from the likes of Global Blue, and perhaps even combine the technology of Global Blue into a common product.

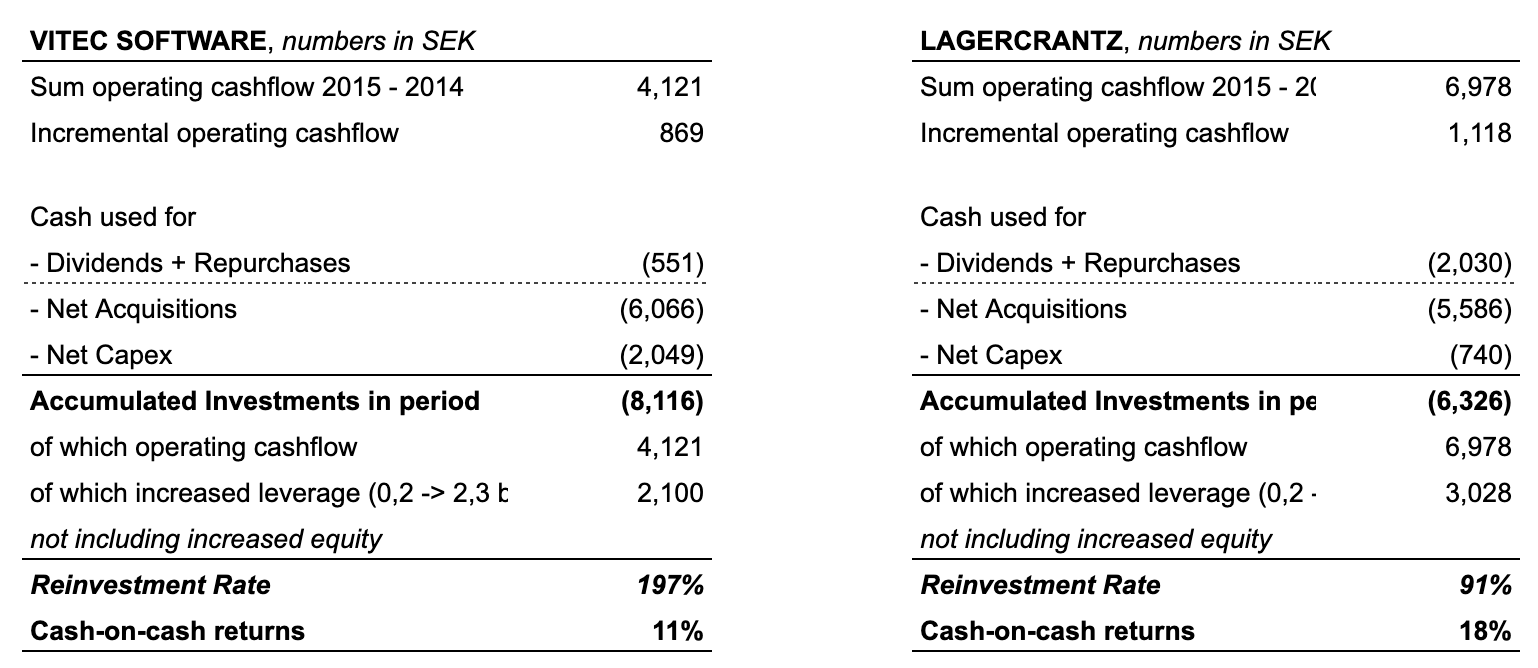

5) Cash-on-Cash returns — Good way to evaluate growth?

With the recent example of Shift4 in mind, we think comparing reinvestments in vs growth out, is the ideal way to evaluate companies reinvesting capital.

Amazon is perhaps the best example, with consistently expensive looking Price to Earnings and poor traditional return on capital metrics. That was because current P&L profits where punished from reinvestments. However, if investors instead focused on the growth in operating cashflow, and consider what portion of existing capex would actually be necessary to sustain operations — the business quality would appear clearer. And if that growth vs the corresponding capital invested was considered, the Cash-on-Cash return would be much higher than ROIC, ROE or ROCE.

In order to do such an approach, we would only need the growth in operating cashflow, and the cumulative investments into key buckets. We have shown the 10y Cash-on-cash returns of Vitec & Lagercrantz in Exhibit V below.

Both companies delivering fast growth, but Lagercrantz requiring less capital in order to do so — thereby not requiring more debt and issue equity to fund this.

Last Years Top Idea

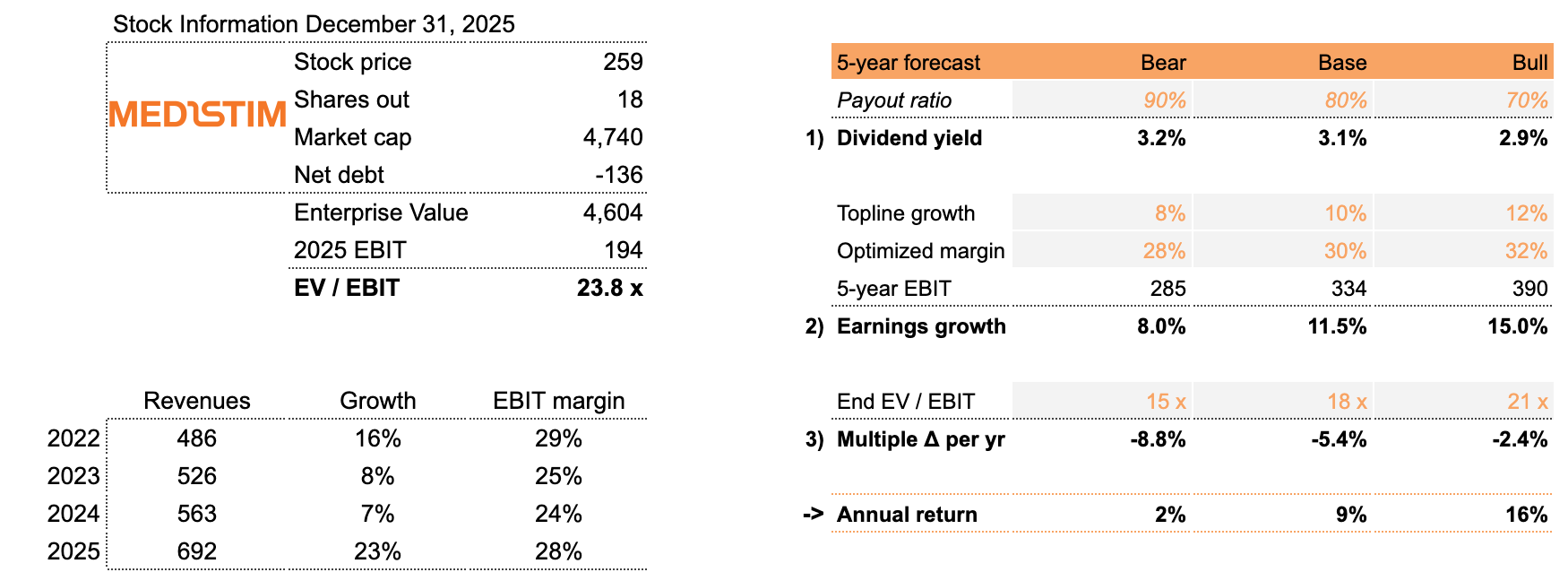

Last year’s pick, Medistim, has delivered strong fundamentals, and the stock is up more than 70% this year. With roughly 23% topline growth and 16% profit growth from expanding margins, much of this shareprice gain also reflects valuation expansion.

Our 5-year forward return estimate now sits around 9% in our base case — less compelling than it appeared last year. Still, we continue to hold every share, despite Medistim now carrying the highest multiple among our holdings at 24x Enterprise Value to EBIT. We believe Medistim can continue their historical growthrate, due to structural tailwinds and new innovations enabling more pricing power, like we’ve seen in their US pricing this year (occured last half 25, becomes tailwind for H1 26 figures).

Best Ideas 2026

This year, we highlight three ideas for paid members. Two are existing holdings that we added to meaningfully during the year, and one is a new position, inspired by another Substack writer.

The new idea is a stable, low-growth business trading at a very low free cash flow multiple. It operates in an unpopular industry facing structural competitive headwinds. As is often the case, the market has largely thrown the baby out with the bathwater, despite this company being only marginally affected by the industry’s broader challenges.

Crucially, the stability of the underlying business provides meaningful downside protection. The upside depends on the company successfully transforming itself into an advantaged acquirer — an outcome the board and operators have clearly articulated as a strategic goal. Notably, the team involved has a long track record of doing exactly this, and appears unusually capable for a company of this size.

The two existing ideas are long-standing core positions. Over the past year, their fundamentals have strengthened, while their share prices have been flat or declined. We much prefer this to weakening fundamentals, especially when we have the opportunity to add more.

If you’re not a paid subscriber, we still want to thank you for following along. We’ll leave the 3 most popular free writeups to date, if you would like to take a look there.

Wish you a happy new year,

Cheers Ole