Adyen

The standout payments player from 2 years ago deserved an update.

Disclaimer: This newsletter is provided for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities. The author did purchase shares after writing this.

Introduction

Why we ignored Adyen for years — and why we’re revisiting it now.

We also explore parallels to Apple under Steve Jobs, despite operating in a very different industry. Our thesis is that Adyen is still building their moat.

Lastly, we’ll look at valuation — where the market offers us this 40% net margin payments leader still growing 20% at a 4% owners earnings yield + net cash.

Two years ago, we studied the payments industry and Adyen stood out with their impressive merchant list (Netflix, Spotify, Booking etc), remarkable financial figures and market share gains.

Yet the stock was expensively priced, and we struggled to fully convince ourselves of the durability of the company’s edge. That edge had long been explained by two things: higher authorization rates through a single integrated platform, and seamless global expansion enabled by Adyen’s banking licenses across the world.

The Dutch Investors argued in a podcast in October 2025 that Adyen did not have a durable competetive advantage at all. Durable is perhaps the key word here, as it’s very clear that Adyen must have something special in order to capture market share for 2 decades in a row — including delivering payment solutions to the likes of Netflix, Uber and Spotify around the globe. And doing that while delivering industry leading net profit margins, around 40%.

Another point brought up in TDI’s podcast, was Adyen’s unique (in the payment sector at least) ability to grow without having done a single acquisition. But, just 8 months later, that changed, with the acquisition of Talon.One and Orb so far in 2026.

We’ve come to a different conclusion on Adyen than what we have found from others online, and thus decided to do a writeup. We will try to answer why Adyen’s sudden acquisition spree makes a lot of sense. And, why Adyen keeps hoarding cash, refusing to listen to shareholders asking for dividends and (more so) buybacks.

We’ll also argue why we think the most frequently read framing of Adyen’s moat is getting outdated (single integrated platform, no m&a and higher authorization rates), as we think those where just the first step of Adyen’s evolution.

To illustrate the shift, just listen to Adyen’s co-CEO Ingo’s first statement of Q1 2026:

What we are seeing across our customer base reinforces a structural shift in where value is created in payments.

Table of Content:

Where Value is Created in Payments

Why Investors Lost Interest

The Direction of the Moat

Dynamic Identification

Similarities to Apple under Steve JobsInadequate Capital Allocation?

Adyen’s Acquisitions in 2026

Valuation

Where value is created in payments

Historically, most value in payments was created at the moment of transaction. The winners were those that could improve authorization rates, optimize routing, increase reliability, expand geographic coverage, and lower acceptance costs.

Those capabilities remain important today. In fact, they may still the foundation of Adyen’s strong competitive position among large enterprise merchants. However, payments are increasingly becoming embedded within broader merchant workflows, where there’s untapped potential for a company like Adyen to solve more problems for their merchants.

This shift is particularly relevant given current market sentiment. Many listed payment processors trade at low valuation multiples, reflecting investor concerns that payment acceptance is becoming increasingly commoditized. Fintech researcher Jevgenijs Kazanins illustrated the “crowded field” by his tracking of 80 publicly traded fintech companies. Given that every one of those 80 companies trade below all-time-highs and at low valuation multiples, there’s little doubt the market starts pricing in a future where payment processing gradually generate less economic value over time.

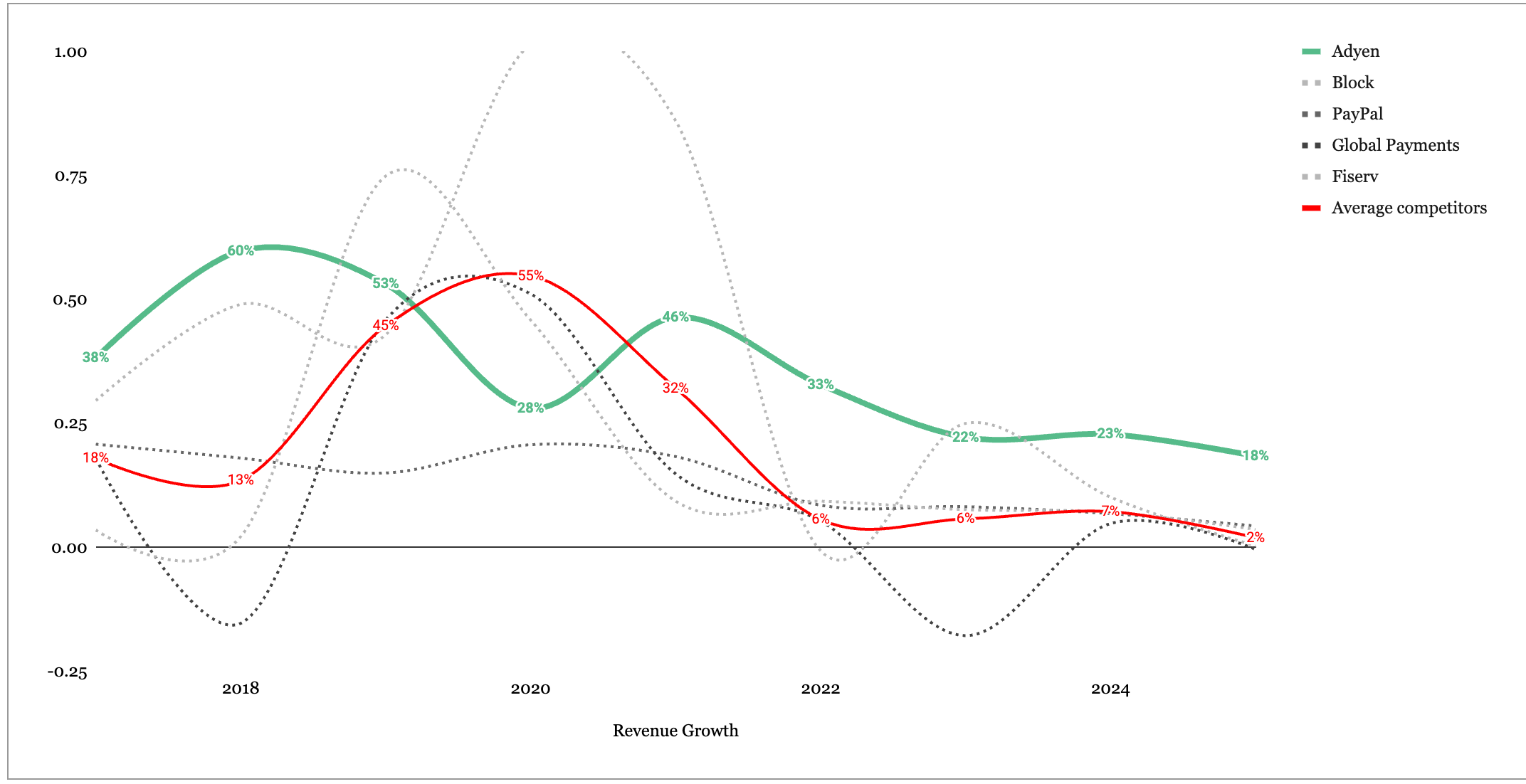

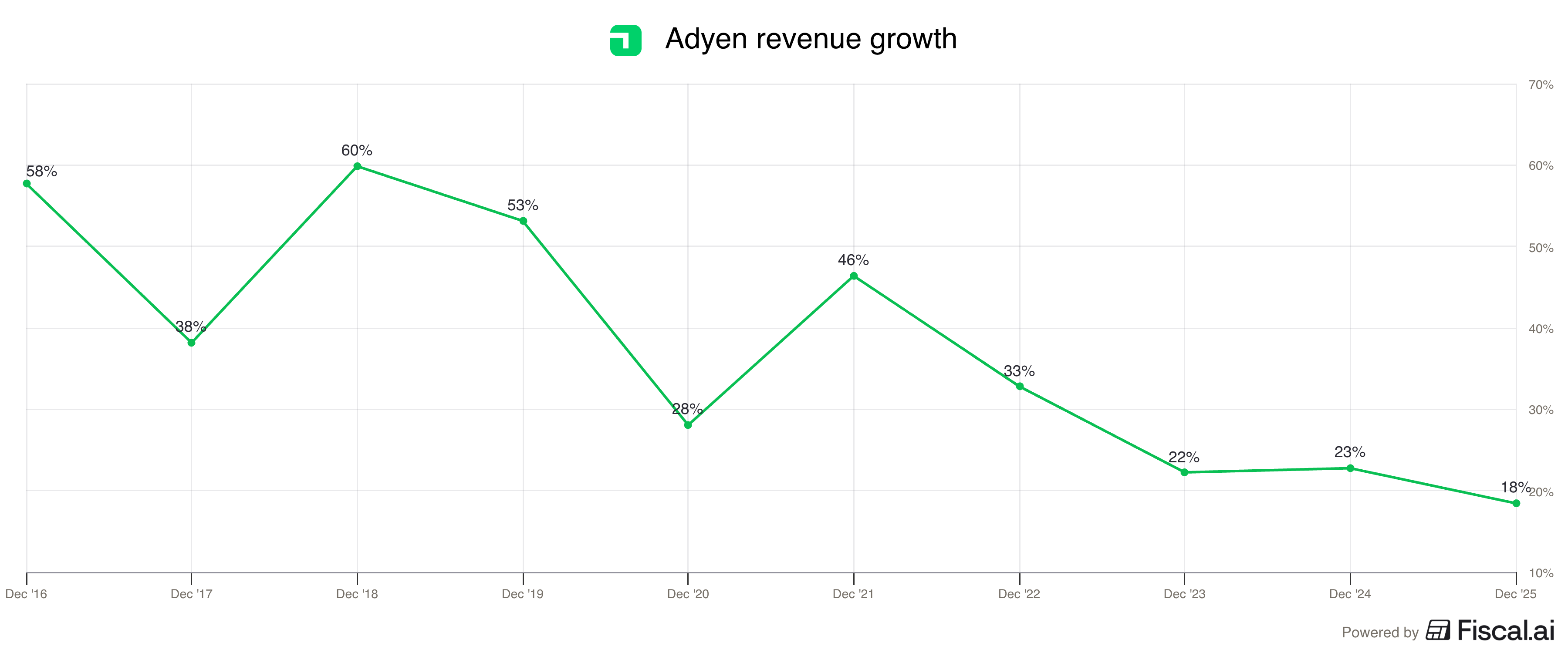

You can see Adyen’s topline growth vs other listed payment companies below. Since 2022, they’ve compounded roughly 15% faster than the average here. The numbers suggest Adyen has something very unique.

Our view on the competetive threat to Adyen is somewhat different. Payment acceptance has historically been an attractive business, but the strongest companies are increasingly those that solve a broader set of merchant problems.

Rather than competing solely on processing costs, they are becoming infrastructure providers that help merchants operate, grow, and scale globally.

Adyen appears to be one of the companies benefiting from this shift, as evidenced by its continued share gains against larger incumbent processors.

The most obvious example of value creation outside the moment of payment, may be the intersection of payments + software in the real world. Some first-movers in this space are Toast and Shift4, both capturing majority market share within verticals like restaurants, hotels and stadiums — by having capabilities that those offering just one piece of the pie can’t match. They did not win customers by lowering price, but by solving more problems for its merchants than just payments.

In Adyen’s instance, the story is more complex. Their initial success likely stemmed from their ability to go very deep on a single problem: payment acceptance. But in doing so, they set up an excellent integrated platform perfect to layer new competetive advantages on top of. Perhaps the most obvious example being Unified Commerce (both physical and digital merchants), where these merchants can leverage Adyen’s technology to recognize shoppers that have purchased either place. That’s much harder to achieve if your solution is stitched together from many vendors.

Another one is Adyen Uplift, which predicts which payment options to show, when to use fraud measures and not, and where to route payments to achieve the lowest costs and highest acceptance rates. They’re also trying to predict what loyalty tools to apply to which shoppers (Talon.one acquisition).

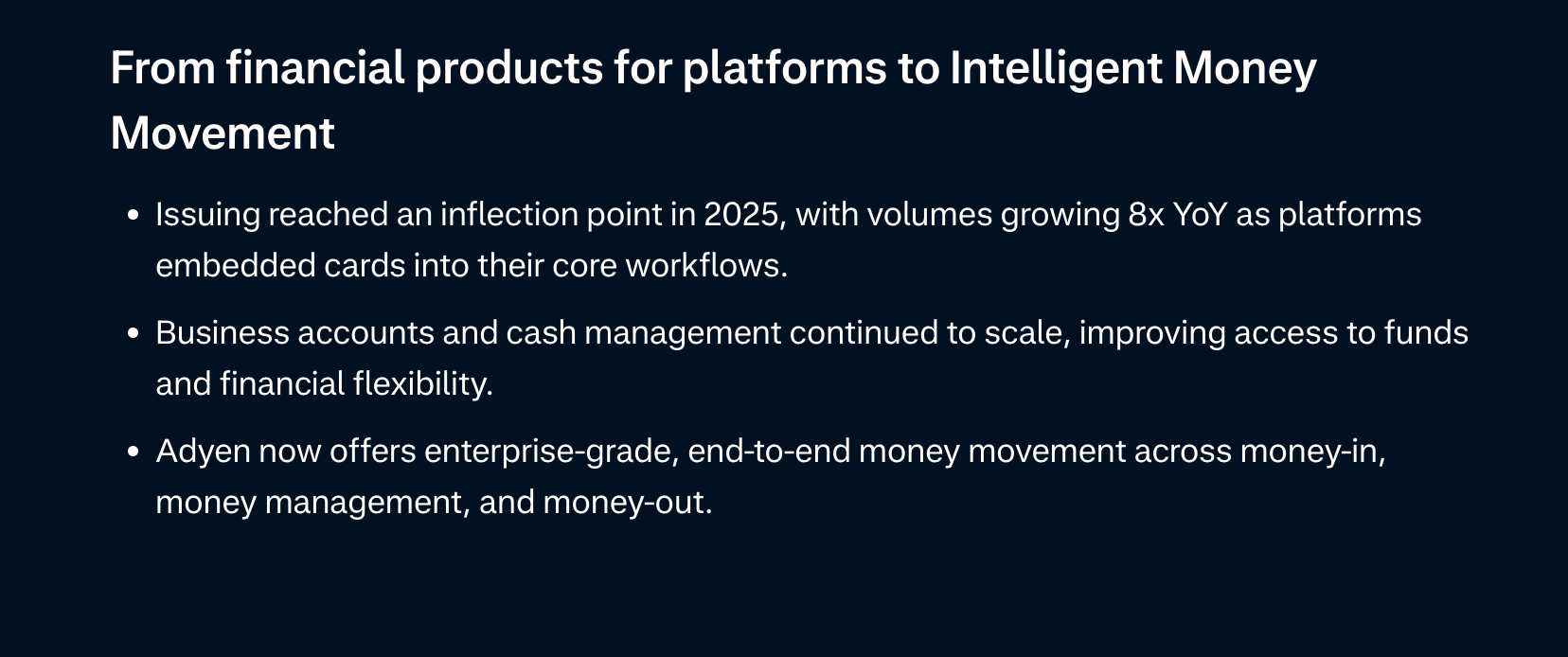

Another problem, quite different, is how enterprise customers typically have 40 bank accounts and their CFO’s spending a third their time managing this complexity. By using Adyen as the primary banking connection, CFO’s can centralize flows and more easily manage working capital in real time. This Intelligent Money Movement is an interesting development, and listening to management, this continues to scale.

Another one, is how Platform customers, like Deliveroo, can deliver Adyen-issued cards to their drivers, enabling them to receive their money right after delivery. Normally, drivers would have to wait for a payment reconciliation for this. Adyen is changing the money movement to become faster and more intelligent. And the proof is in the figures: “Issuing volumes growing 8x YoY as platforms embedded cards in their workflows”.

We believe Adyen’s key edge to follow is the below, which we’ve heard numerous times in our research about Adyen, both from Adyen themselves but more importantly from it’s merchants.

Adyen is a subscribtion to innovation

Why investors lost interest

And why the opportunity exist today?

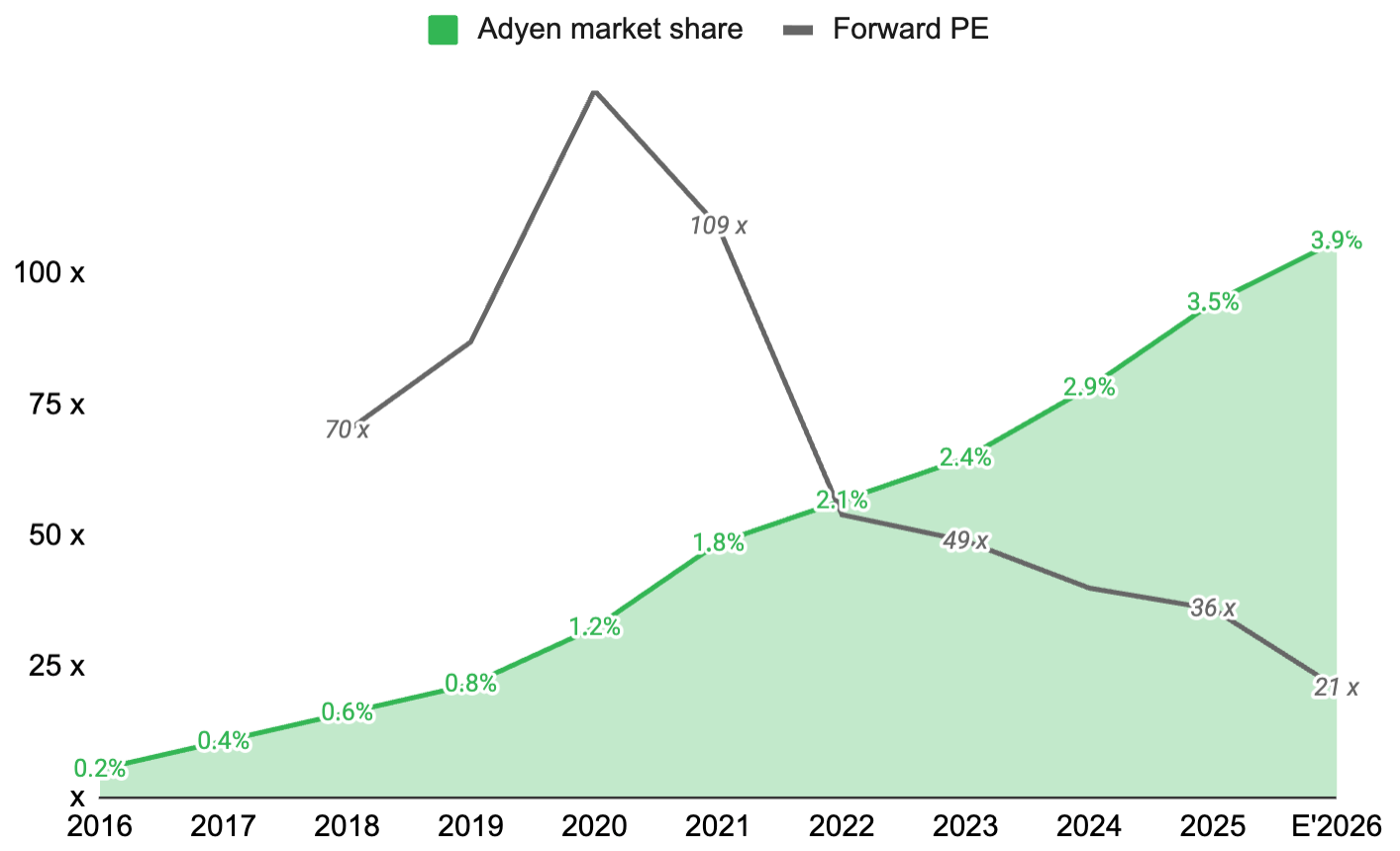

The first explanation is simply that expectations where too high. In 2021, the company traded north of 100x Price to Earnings multiple. Even after more than an 80% drop in the valuation multiple (20x), the stock is just now priced closer to the market average.

Part of this is also explained from a broader selloff in payment stocks, with the likes of Global Payments, Fiserv and Paypal trading at single digit earnings multiples for 2026. On a relative basis, Adyen is therefore still trading at a premium multiple, and other payment peers have seen a similar drop in it’s shareprice.

Competetively, the market may also have been spooked by private companies like Stripe and Checkout.com gaining market share rapidly. From the table below, it’s clear that Stripe especially is firing on all cylinders (also boosted from acquisitions).

When comparing Adyen to Stripe, it is important to recognize that the two companies have historically approached the market from opposite directions. Stripe initially focused on startups, software companies, and digital-first merchants before gradually moving upmarket. Adyen, by contrast, built its business around large enterprises and is now expanding deeper within those organizations. While both are competing for the same attractive payments market, the opportunity remains large enough for multiple winners, as illustrated in the table above. And both seem to increasingly solve more problems outside of payments.

When investors hear news about Stripe or Checkout.com winning high-profile partnerships — such as Stripe’s recent integration with ChatGPT-enabled shopping — it is easy to assume that Adyen’s weak share price reflects a deteriorating competitive position. In reality, Adyen’s business is largely invisible to the average consumer despite its enormous scale. The company operates behind the scenes when we pay for our Spotify or Netflix subscriptions, book accommodation through Booking.com, or order food delivered by a Deliveroo or Just Eat Takeaway rider.

Adyen has also deliberately avoided aggressively pursuing small and medium-sized businesses, a market that often requires a large salesforce and significant customer acquisition efforts. Instead, the company remains focused on larger enterprises and, increasingly, highly complex organizations. Its expansion into Platforms further signals an ambition to enable other businesses to scale rather than compete for direct customer attention. Adyen does not appear interested in being the most visible player in the industry; it is focused on operating where it can create the most value.

It seems like where Stripe scale rapidly by going wide with a lot of merchants, Adyen rather goes really deep with fewer merchants. Best exemplified with Stripe having roughly 25x as many merchants as Adyen(5mill vs 200k), despite market share being much closer to eachother.

A few additional factors may also be weighing on investor sentiment. The company’s CFO is leaving the same year that Adyen completed its first two acquisitions, creating uncertainty around an important strategic shift. There is also frustration among investors who have watched the stock lose roughly half its value over the past five years while management has shown little interest in actively “fixing” the share price.

At this year’s AGM, for example, one shareholder repeatedly challenged management on why the company does not repurchase shares or pay dividends, arguing that its capital allocation strategy was inadequate. Management’s response was calm and straightforward.

First, they view their strong balance sheet as an enabler to obtain regulatory licenses and launch financial products more quickly and efficiently. Exemplified with their A- credit rating from the S&P.

Adyen’s fortress balance sheet may also help land big deals. For global corporations outsourcing mission-critical operations, a vendor's long-term solvency is a key consideration. Adyen’s substantial cash reserves mitigate counterparty risk, providing the financial reassurance necessary to win and expand large-scale enterprise contracts.

Moreover, management believes it can create more shareholder value by reinvesting capital into growth, demonstrated by the two acquisitions completed this year. But they also stated no intention to hoard cash forever. Given the roughly €4 billion net cash position to Adyen, we may start seeing capital returns or more reinvestments (like the two acquisitions) going forward.

The last clear reason we see, is a revenue deceleration from the high levels sustained through 2021. But even a 20% currency-neutral growth they target this year and for the next few would go under rapidly gaining market share in almost any industry, also payment processing. Thus, we don’t see this as a structural problem, rather that Adyen’s smaller base was much easier to grow from earlier in their journey.

For those familiar with McKinsey’s base-rate studies on growth persistence, Adyen’s trajectory is notable. Companies starting at ~35% growth typically see a sharp normalization, with average growth falling to ~15% by year three and ~7% by year five. Against this backdrop, Adyen’s deceleration from ~mid-30% growth in 2020–2022 to ~21% in 2023–2025 is meaningfully stronger than the base-rate expectation. And management expects the 20%-rate to continue for longer than 2026.

We don’t see why Adyen’s growth story is over. But the stock is priced for this to continue to decelerate.

To conclude, once Adyen’s multiple have moved closer to the average business out there, we should start asking ourselves — will this above-average business (20% growth + 45% net margins) really move towards average already?

The answer of this should lie in the direction of their Moat.

The Direction of the Moat

The key question for us in evaluating Adyen as an investable idea is not what the moat is today, but where it is going. We are looking at a highly technical company in an industry we can’t fully understand. More specifically, we cannot precisely judge how difficult it would be for a legacy processor to replicate Adyen’s single integrated stack.

But we can observe something more important: whether replicating Adyen seems to get easier or harder over time. Our analysis lead us to believe the answer is the latter.