Bench and Watchlist - Q1 2026

Cover: Harvia, Momentum Group, Scottish Mortgage, AG Barr and GCI Liberty

This issue is free for all subscribers.

Summary:

Not every position earns its place. This quarter, one didn’t — and we exited before it could do real damage. That’s the bench working as intended, a key part of how we think about portfolio allocation. A topic we’ve found surprisingly harder than finding great ideas.

Alongside that, we go through three bench holdings (small weight) and two watchlist ideas — including a defensive UK compounder at ~12x earnings, a John Malone-linked spin-off trading at ~11x cash flow, and a holding company with exposure to the AI buildout.

Disclaimer: This newsletter is provided for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities.

We recently made a mistake. After our recent Serial Acquirer writeup, we initiated a small position in Momentum Group — while passing on Lifco, a clearly better business at a slightly higher multiple. Lifco’s quality became even more evident after Q1 2026: Momentum delivered -6% organic growth, Lifco came in positive, as usual. The market reacted accordingly, sending Momentum Group down ~17%.

So why did we choose the cheaper, lower-quality alternative?

We had studied Lifco years earlier at roughly half the price. That reference point probably stayed with us — making it harder to justify buying a better business at a higher price. This is a classic case of anchoring bias — something we’re aware of, yet didn’t fully overcome here.

The important safeguard here was position sizing. Momentum was intentionally kept small. The “bench” is designed exactly for these situations: to let conviction either build or fade before a position earns meaningful capital allocation. In this case, conviction faded, and we exited with a modest loss.

This stands in contrast to our investment in Norbit three years ago. We scaled in gradually, conviction strengthened with each report, and it has since become our largest position today.

This experience reinforced something we increasingly believe: finding great businesses is often easier than allocating well between them. A structured bench makes that allocation process meaningfully better, at least in our experience.

Why the Bench matters

Over time, we understand businesses better — both their strengths and their flaws. Our decision-making seem to improve the longer we’ve followed or (more so) owned something. Keeping new positions small gives us time to refine our view before they meaningfully impact returns. If we sized up Momentum Group immediately to 10%, we wouldn’t have a similar opportunity to reassess without impacting returns similarly

Another lesson this year is what a lack of diversification brings — volatility.

Volatility is often viewed as a measure of risk, we think the bigger risk lies in not being able to participate in upside, for instance with the exceptional earnings from the Google and Amazon’s of the world, or the recent rally in energy-related stocks.

However, predicting which style wins when is hard.

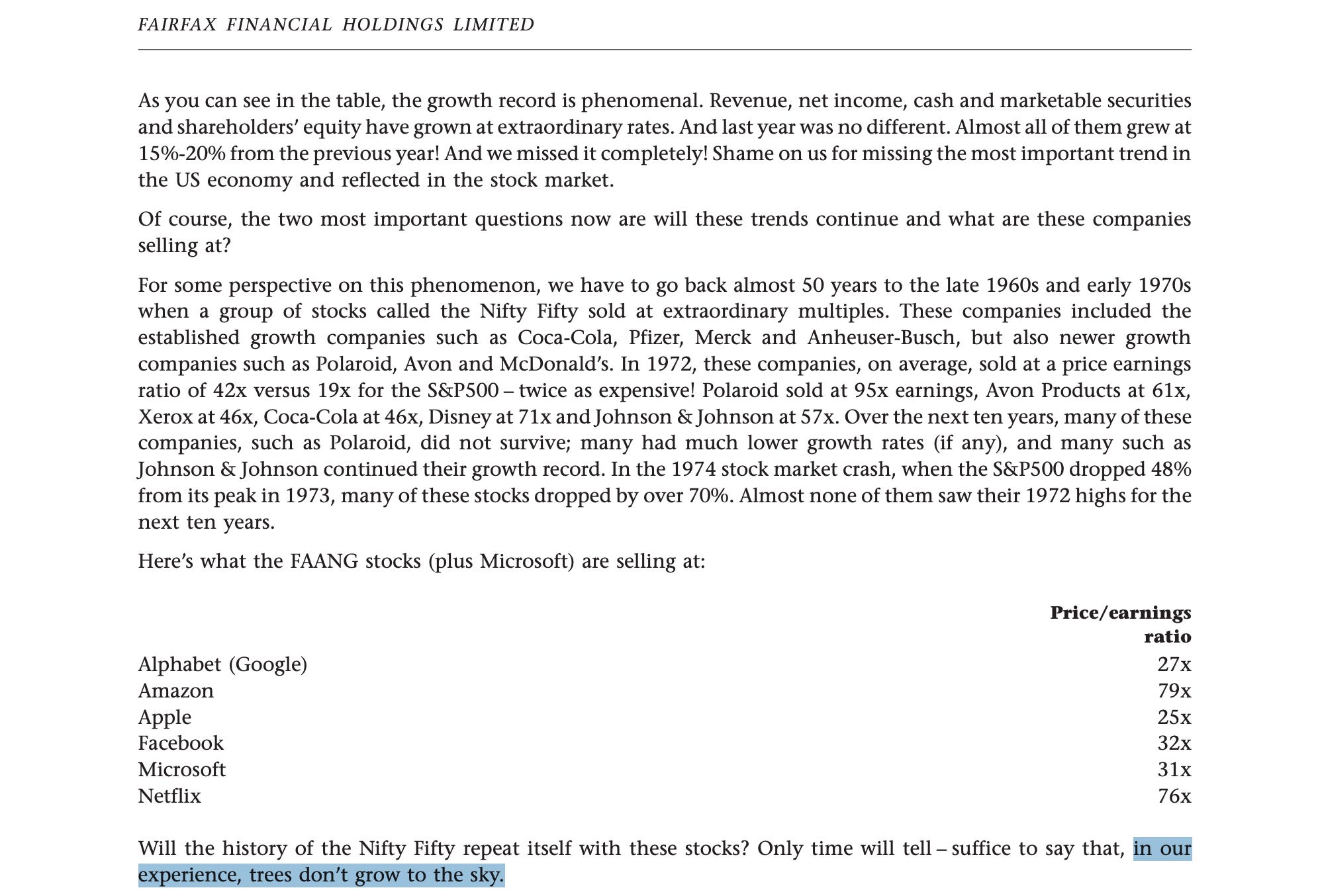

Fairfax Financial — a stock that seems to appear every so often in our X feed — is a good illustration. In their 2019 Annual Report, they called out FAANG stocks as trading at absurd valuations. With the benefit of hindsight, that call was spectacularly wrong: those stocks have since returned 3 to 6 times. Similarly, Fairfax themselves have delivered similar returns over the same period, through an entirely different approach.

There are a few lessons here. One is simply how extraordinary businesses like Google and Amazon have proven to be. Another is that predicting the future is genuinely hard. A third — and the one most relevant to how we think about the bench — is that there are many roads to Rome (Fairfax’s approach worked well too).

Given the challenge in predicting the future, we are now more mindful of using the bench and watchlist to look for traits our current key holdings lack. For instance, our latest bench addition, is a defensive consumer business trading at 12x profits, expecting double-digit growth this year.

It’s a very different business from what we currently own: 95% of revenues in their home country gives minimal risks from tariffs and geopolitcal instability. And the defensive traits means it usually performs well in tough economical times.

Similarly, on our watchlist, we have one idea that benefits from the current AI investments. Exposure our portfolio currently lacks. We’ll now go through our 3 Bench Holdings (<3% weight) and 3 Ideas on our Watchlist.

Harvia (3% weight)

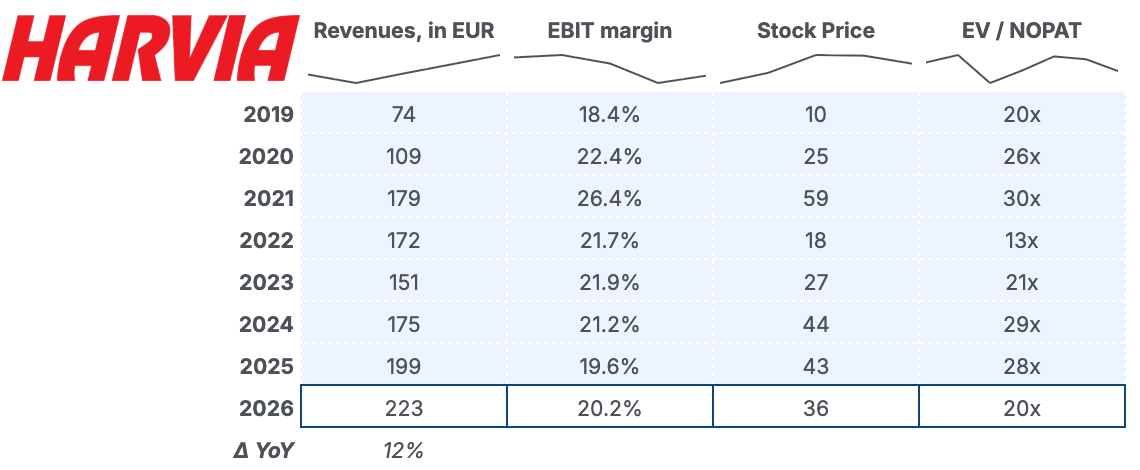

Harvia is the leading player in a historically 5% growing global sauna market, now expected to grow faster going forward. A leading brand with stable operating margins around 20% and efficient scale-advantaged sourcing + production. Taking a consolidator role, by buying up attractive assets within the fragmented sauna industry. Significant growth markets: US, Japan and China to name a few, whereas replacement demand provides recurring revenues in well-established markets closer to home (Finland).

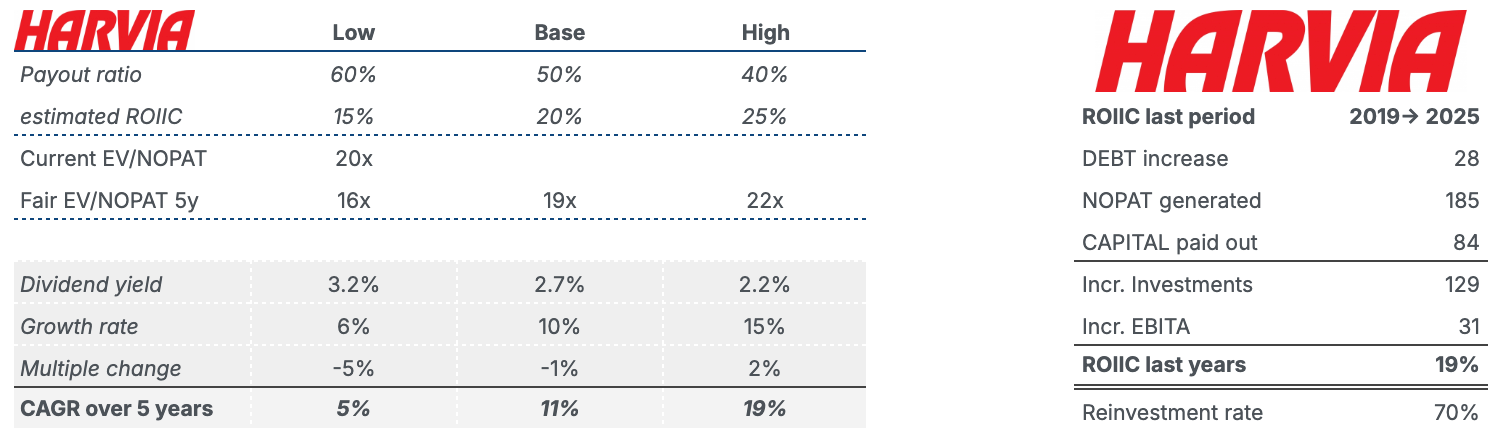

To fuel the significant growth Harvia has had, we estimated a ~70% reinvestment rate, while paying out a 50% dividend payout ratio (both in relation to NOPAT). Net Debt to EBITDA have remained stable around 1x, exactly what a high ROIIC business enables — growth, free cashflows and low debt. We estimate around 19% ROIIC.

We believe Harvia is well positioned for double-digit profit growth, while paying a 2%+ dividend yield. Given the growth potential and market-leading position, we think the stock is fairly priced around 20x EV / NOPAT today (36 EUR per share).

We have avoided making Harvia a larger position so far, due to the price tag well north of 20x EV / NOPAT for a long period. Recent share price pressure provided an attractive entry point. We’ve owned Harvia for a year now, and consider scaling it up.

Scottish Mortgage Investment Trust (watchlist)

We’ve learned that we prefer sleep-well businesses — steady growth, lots of free cashflows and easy to understand businesses.

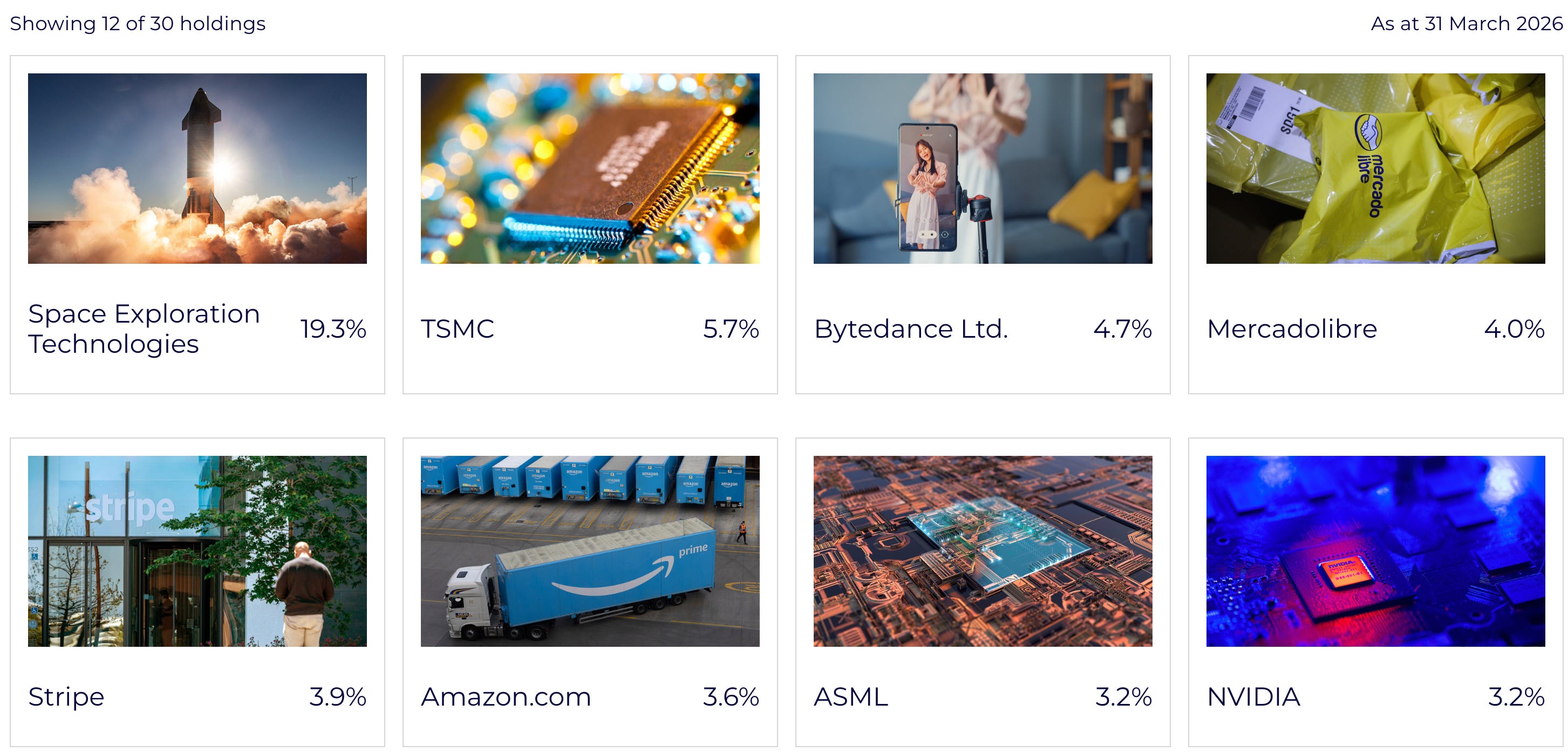

However, the recent AI buildout we did not participate in would require a different investment style. One which the Scottish Mortgage Investment Trust have finetuned over a century. Early investments, fast growth and Long holding periods.

They benefited from Nvidia’s and Tesla’s surging demand, transitioned those position into more Taiwan Semiconductor and ASML. Further, they invested in the private companies SpaceX and Anthropic, both of which could IPO at multiples higher prices than what Scottish Mortgage paid for their ownership stake.

We think Scottish Mortgage is a great way for us to outsource research into the type of companies we would not have an edge in studying, while getting exposure to the largest megatrends of the world. In the last years, they’ve also demonstrated that they’re willing to buyback their own shares when trading at a large discount to NAV.

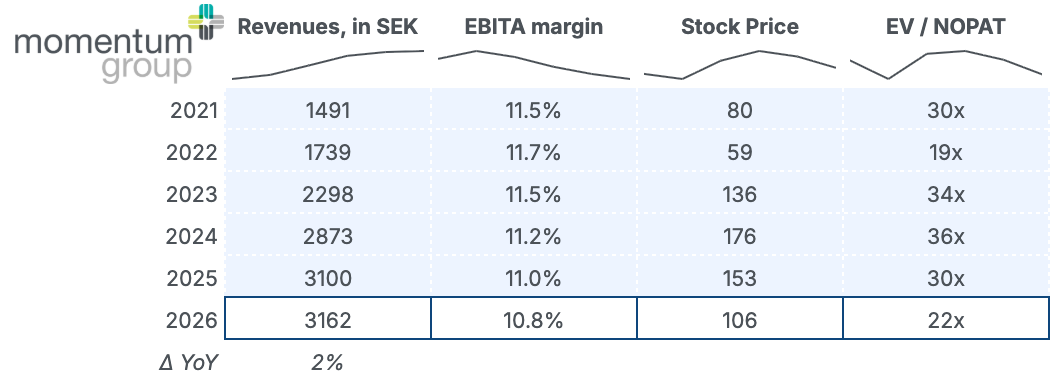

Momentum Group (recent sale)

An industrial market leader comprising 37+ decentralised businesses. We covered the company in our Serial Acquirer Writeup; key figures are shown below.

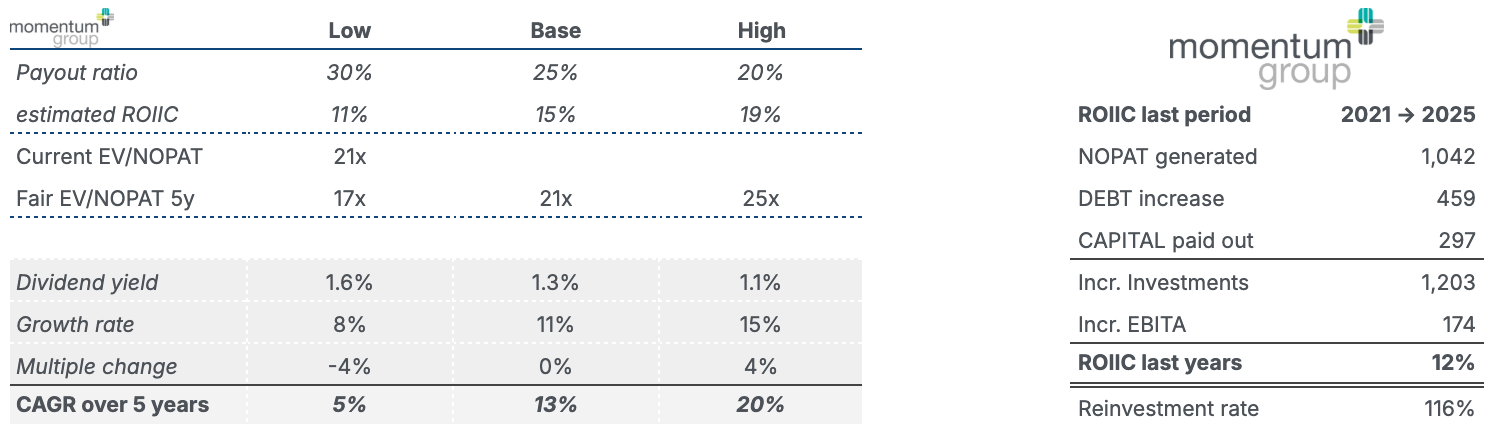

In our ROIIC calculations, we’re including our expectations for 2026, which is now showing flat EBITA and negative organic growth, which hurts ROIIC, as plenty of investments will occur this year. 12% ROIIC is not the return we’re looking for, but this is calculated from peak margins in 2021. The comparison point is more favourable from 2019 or 2022 for example.

Organic growth of -6% is not necessarily structural, but it reinforces an initial concern: Momentum Group operates with structurally lower EBITA margins than peers such as Lifco, potentially signalling lower underlying business quality. This concern is further amplified when compared to other industrial acquirers—AQ Group, Lagercrantz, and Diploma—which continue to deliver solid organic growth.

We also note a shift in tone from CEO Ulf Lilius. In Q4 2025, commentary pointed to improving conditions into 2026. However, in the Q1 2026 call, that optimism appears to have faded, with guidance now implying a weaker outlook for the year.

Our long-term view on Momentum Group remains positive. Nevertheless, we expected the Industry segment, given its exposure to aftermarket demand, to show greater resilience. However, the recent performance suggests that a significant share of revenues remains tied to underlying activity levels, making the business more cyclical than initially assumed.

The challenge is compounded by valuation. Even after a ~17% share price decline, the stock trades around 21x EV/NOPAT, offering limited margin for error alongside a modest ~1% dividend yield.

From an opportunity cost perspective, alternatives look increasingly compelling. Volati trades at a ~40% discount, with indications of exiting its current downturn and a planned spin-off of its most cyclical segment — potentially leaving a higher-margin quality core. Alternatively, one could justify paying a ~20% premium for Lifco, given its superior margins, more consistent organic growth, and similarly disciplined acquisition strategy.

We have not reached a final conclusion, but for now, we do not plan to increase our position in Momentum Group despite the recent share price weakness.

Now to the newest bench holding, a defensively positioned UK small-cap at a 12x profit multiple and expected to grow at low double-digits this year. Following this, we share a watchlist idea trading at 10x free cashflows and recently announced a significant acquisition, perhaps the first of many.

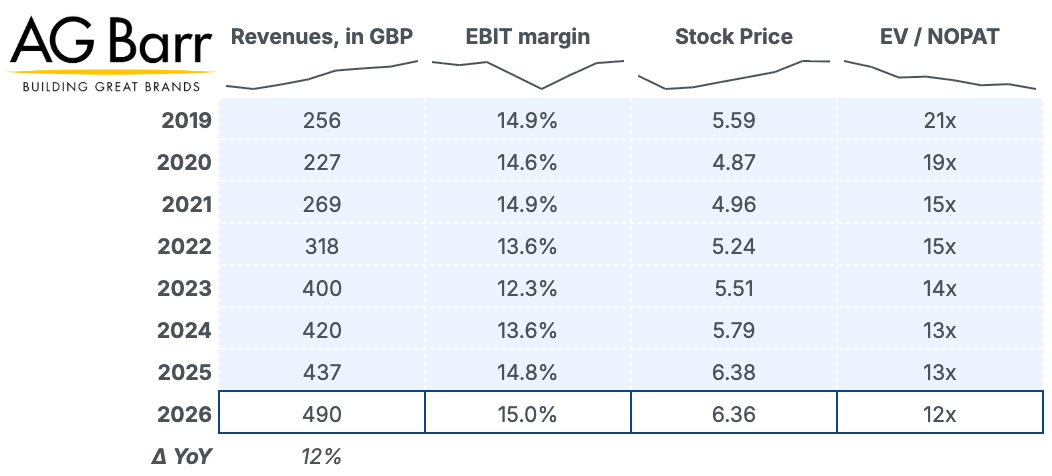

A.G. Barr (2% weight)

A portfolio of drinking brands in the United Kingdom, with Irn-Bru as the enduring standout - the only soda brand beating Coca-Cola in a developed market (Scotland). Today, they have 3 other key brands - Boost, Rubicon and Funkin - all acquired at attractive prices and grown organically since. Along with several smaller brands, and partnerships with famous products like Bundaberg, San Benedetto and Snapple.

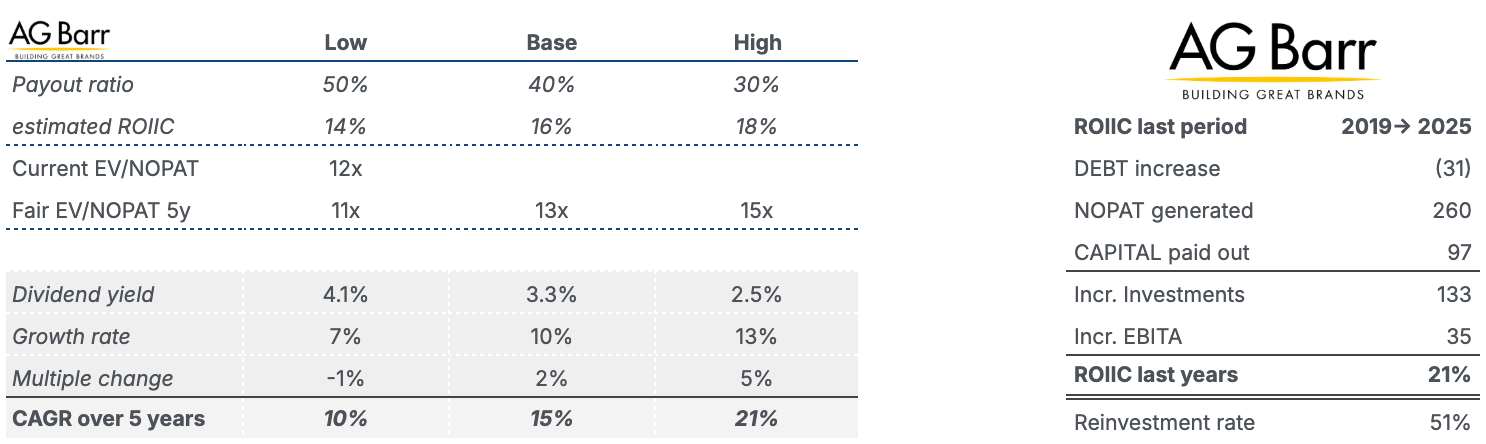

AG Barr has been a steady grower with low reinvestments around 50% of NOPAT since 2019 and dividend payouts of 40%, resulting in an increasing net cash position. However, the introduction of management compensation tied to EPS growth and relative Shareholder returns to the stock index, means the company now requires high reinvestment rates. The company has clearly stated the ambition to reinvest more.

Luckily, AG Barr has historically been a disciplined capital allocator, with a target of around 20% return on capital employed. Add double-digit EPS growth targets for the compensation to fully vest and 20% ROCE together, and you would have a compounding machine, not something the market is pricing in at 12x EV / NOPAT.

We believe AG Barr will continue increasing their reinvestment rate, and grow high single-digit to low double-digits. The table below does not take into account that the net cash position allows a higher dividend payout while reinvesting. At 12x EV / NOPAT today, around 21% ROIIC and the resilience of a well-tasting drink - we think AG Barr is a more defensive addition to the portfolio, but with upside.

Recent News: The 2026 acquisition of Fentimans at 1x sales, a low-margin century-run family brand, looks like a synergy-play, where AG Barr’s manufacturing scale may generate higher margins for the Fentimans products.

GCI Liberty (watchlist)

We’ve been following GCI Liberty for several months and came away positively surprised by its acquisition of Quintillion.

Quintillion adds a highly complementary network footprint, strengthening redundancy across GCI’s infrastructure in rural Alaska. In practice, this means improved reliability: where one network is vulnerable, traffic can be rerouted through the other. This also serves as a counter to the risk of loss of rural customers to Starlink.

(See video below for more on the transaction and its rationale.)

The deeper investment thesis here is not just about getting a complementary network, it’s about John Malone making this into an acquirer with durable cashflow streams, an advantaged tax-benefit following it’s spinoff in 2025 and a proven acquisition strategy of Malone & Co. Following the spin-off from Liberty Broadband, the small $1.3 billion company GCI Liberty benefits from the M&A knowledge from the broader Liberty Media Group and John Malone himself, as chair of the board.

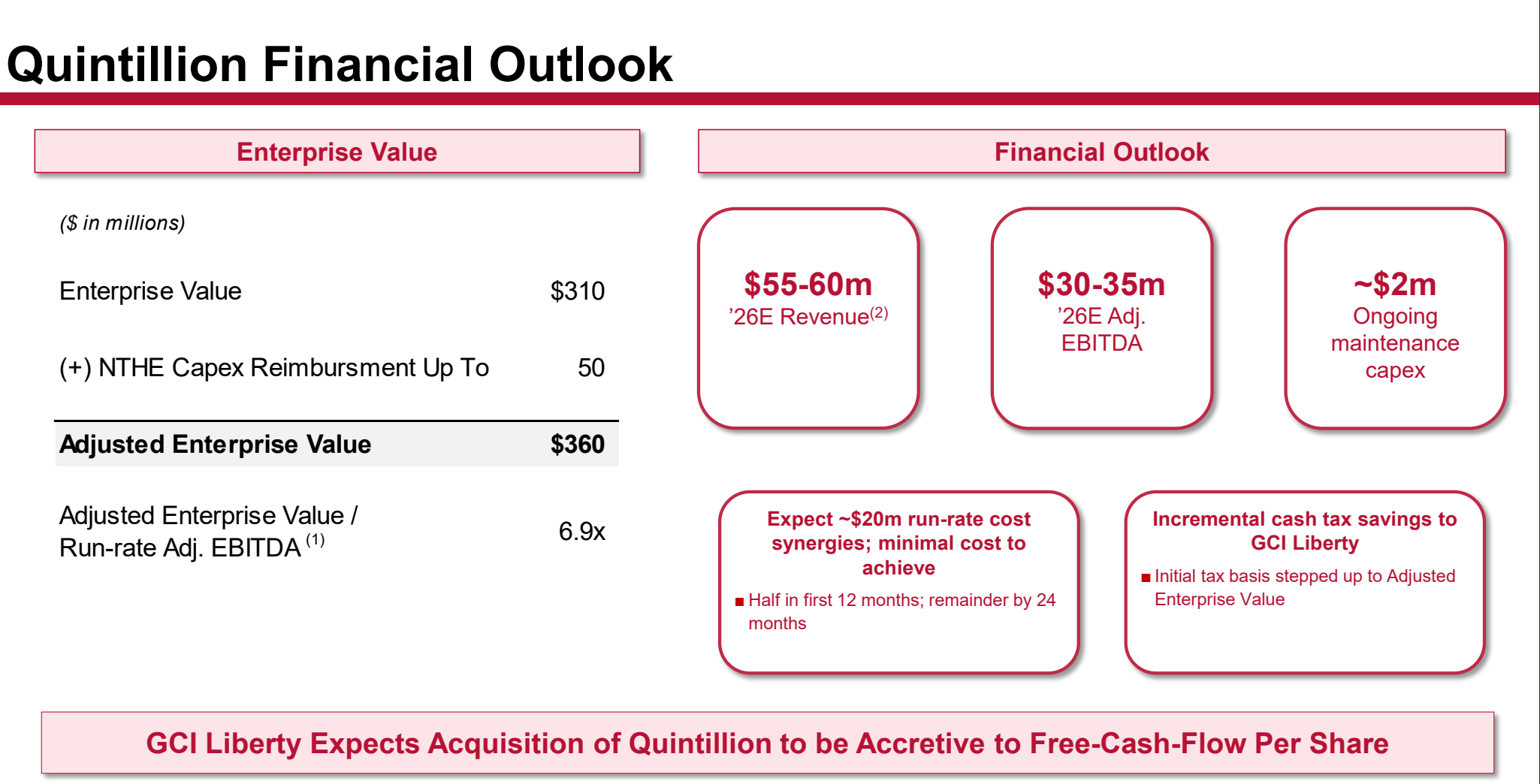

The stock is now down to $34 per share, or a $1.3 billon market cap. At an Enterprise Value of $360 million, Quintillion is a significant investment for GCI.

The deal is done at ~7x EV / EBITDA, and GCI expects $20 million of cost synergies over the next 2 years, plus the benefit of GCI’s advantaged tax assets being used.

Let’s apply some rough napkin math:

GCI Liberty generates approximately $400 million in annual EBITDA on $1,046 million in revenue. At a capex intensity of around 18% of sales (19–22% range last 3 years, guides lower) — pre-tax profit lands near $200 million. Strip out stock-based compensation and apply zero cash taxes given the company’s unique tax shield, and you’re left with roughly $190 million in pre-interest free cash flow from the core business.

Layer in Quintillion’s ~$25 million in annual FCF and approximately $10 million of first-year cost-synergies, and the post-acquisition run-rate lands around $225 million. Against an enterprise value of roughly $2.3 billion — inclusive of the Quintillion purchase price — the stock trades at approximately 10x EV/FCF.

That price seems low to fair for the defensability this business offers, but very low if John Malone succeed in his ambition of turning this into an acquirer. With the first acquisition underway, the next move may take GCI beyond Alaskan broadband. That would at least make the acquisition-story more compelling, given the lack of growth opportunities within Alaskan broadband.

We recommend Chris Waller’s substack if you are interested to read more about GCI Liberty.

That’s it for today, let me know if you have any questions or ideas to look into!

All the best,

Ole

Have been an Harvia shareholder since 2019. Great company, which will keep doing well for many years.