Inside the Corner - April 26

20x variance in returns from same growth? Portfolio Update, Estimated CAGR for Holdings and our new idea to replace our defensive Canadian Waste Infrastructure.

Disclaimer: This newsletter is provided for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities

Two events shaped the portfolio this month: we trimmed our position in Investor AB, and exited Secure Waste Infrastructure following a bid from GFL Environmental.

Investor AB: Our estimated CAGR going forward now at mid to high-single digit.

Secure Waste: Full exit at a 36% IRR over 1-year following GFL’s bid for the business.

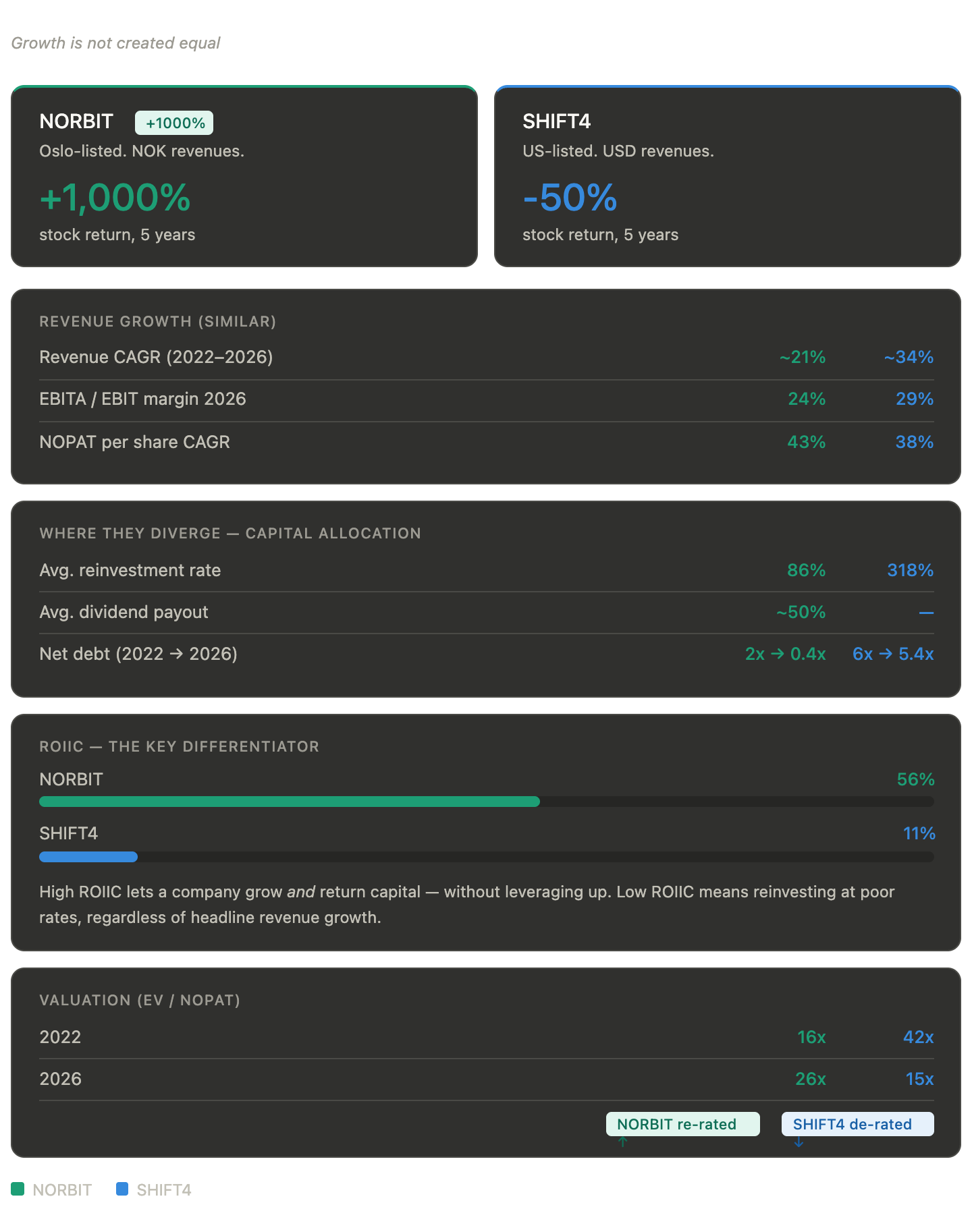

And to the lesson of this month. After we studied the Serial Acquirer space again, we appreciated more that growth is not created equal. We illustrate this with two key holdings - Norbit and Shift4 - and why their stock returns turned so different in the last 5 years (1000% vs -50%), despite similar growth (~40% profit CAGR).

The advantage of a high return on incremental invested capital (ROIIC), is that it allows growth + distribution of capital to shareholders, while avoiding leveraging up. A high growth company reinvesting more capital than they generate, either needs to issue equity or debt to keep the growth going.

NORBIT vs SHIFT4

We gave Claude access to our detailed spreadsheets on both companies to generate the illustration below. The core takeaway is simple: the difference in ROIIC led to very different capital requirements — and the market responded accordingly. Norbit was re-rated from 16x to 26x EV/NOPAT, while Shift4 was punished from 42x down to 15x.

Two similar growing companies had a 20x variance in shareholder returns!

While the answers today are glaringly obvious Norbit was the winner, we think timing of investments are an underappreciated factor in both cases.

Norbit’s elevated ROIIC today reflects sector tailwinds and prior years of groundwork bearing fruit — including a decision to invest in their Norwegian manufacturing facilities at a time when most peers were outsourcing. Shift4, by contrast, are currently within their heavy investment phase: acquiring key assets for future cross-sell opportunities (including the massive acquisition of Global Blue) and securing new contracts by subsidising merchant onboarding.

That last point deserves more attention in understanding ROIIC. Buying out a merchant’s residual commissions to accelerate a switch, or giving away hardware for free, are upfront investments that drag on near-term returns. But once a merchant is on Shift4’s platform, that cost disappears into the rear-view mirror — and the toll-booth kicks in, quietly taking a small share of every transaction the merchant processes, year after year, with limited maintenance investments. The stickiness is the point. Shift4 has deliberately focused on verticals where switching is painful: stadiums with hundreds of software integrations, hospitality, and complex environments. We think that’s a moat built through years of patient investment — not currently reflected fully in trailing ROIC. Thus, once Shift4 slows down on growth spending, the ROIC should expand.

The thesis for Shift4 is therefore relatively simple: Key investments for success in the coming decade has been made, and as a result, debt is at a record 5x NOPAT level and ROIIC is at record lows, scaring investors. But, behind the ugly ROIIC and debt level, is a business ready to generate a ton of cashflows going forward — enough to pay down much of their debt, buyback stock and reinvest a healthy portion going forward too. The first proof was the North American Business in Q4 2025, not impacted by acquisition impact, expected to grow mid-double digits in 2026.

We may be wrong, which is also why we don’t size up positions more than the low double-digits for individual businesses. That’s still meaningful positions in our portfolio, representing almost half a years’ salary for ourselves.

Portfolio Update

The past year has been challenging for the portfolio, with a -11% YTD return — largely driven by our decision to concentrate into Constellation Software and Shift4 at a time when software and payments became some of the most disliked sectors in the market. That said, zooming out we’re still up 102% over 3 years, and since inception in late 2021, we’ve compounded at a money-weighted CAGR of 13%. Albeit with more volatility than most indices, a price we’ve paid for concentration.

Activity has been relatively limited in recent months, aside from adding to a few key holdings. To better visualize our highest-conviction ideas, we revisited our models and estimated forward CAGRs with a ±1 standard deviation range. The goal is simple: be prepared to act decisively when opportunities arise — and focus on ranges of outcomes, with the aim of being directionally right.

This framework highlighted volatility in names like Norbit, Medistim, Eurofins, and MBB earlier this year — allowing us to increase our ownership at what we thought was attractive levels. Below, you’ll find our estimated CAGR for each of our holdings.