Inside the Corner - August 2025

Portfolio Update and a look into a Medical-oriented Holding Company for Ideas.

Disclaimer: This newsletter is for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell securities. All investments involve risk, and past performance does not guarantee future results.

Before we dive into our portfolio this month, we would like to show what we are currently researching. Our recent Nordic Industrial Sector Writeup made us more aware of both the quality existing within the Medical field, but also that they seem to be on sale, at least relative to the last decade and to other Industrial sectors.

This Month’s Inspiration – A Medical-Focused Hold’co

When we study companies, we always pay close attention to ownership structures. Where we previously mostly looked for aligned operators with real skin in the game, we think the true differentiator is evidence of a long-term horizon from management.

Our deep dive into Investor AB’s subsidiaries showed how a long-term mindset within subsidiaries, supported by their owner, can compound value over decades. Backed by Investor’s patient capital, many of Investor’s subsidiaries successfully allocated capital well, exited commoditized sectors, acquired and even spun off parts and repositioned themselves in areas where they could build durable advantages.

All strategic decisions and capital allocation moves which would have been very hard to predict in advance, but which in total, where crucial for the value creation.

We doubt any analysts in the early 1900’s modelled out Atlas Copco to deliver double-digit CAGR in profits between 2015 and 2025 (incl. spinoff).

Back to our Industrial Sector Writeup, we were intrigued to see repeatedly the largest owner of several high-scoring businesses being a Holding Company we hadn’t heard of before: William Demant Invest.

In our view, there has rarely been a better time in the past decade to explore the portfolio of this medical-focused holding company.

William Demant Invest

While we can’t invest in William Demant Invest directly, they do publish their holdings, most of which are publicly listed, and more interestingly, their thoughts around these companies quite closely.

2024 was characterised by stability for the companies in the William Demant Invest portfolio. In a year of continued geopolitical uncertainty, we once again saw consistent performance from the companies in the portfolio with sustained positive growth trajectories. (Niels Jacobsen, CEO)

We believe it’s worth taking a closer look at some of their holdings, not just because of the mentioned “attractive growth trajectories”, but also because they have, on average, fallen out of favor with the market. Today, they trade at far more reasonable valuations, despite showing all the hallmarks of quality businesses.

William Demant Portfolio

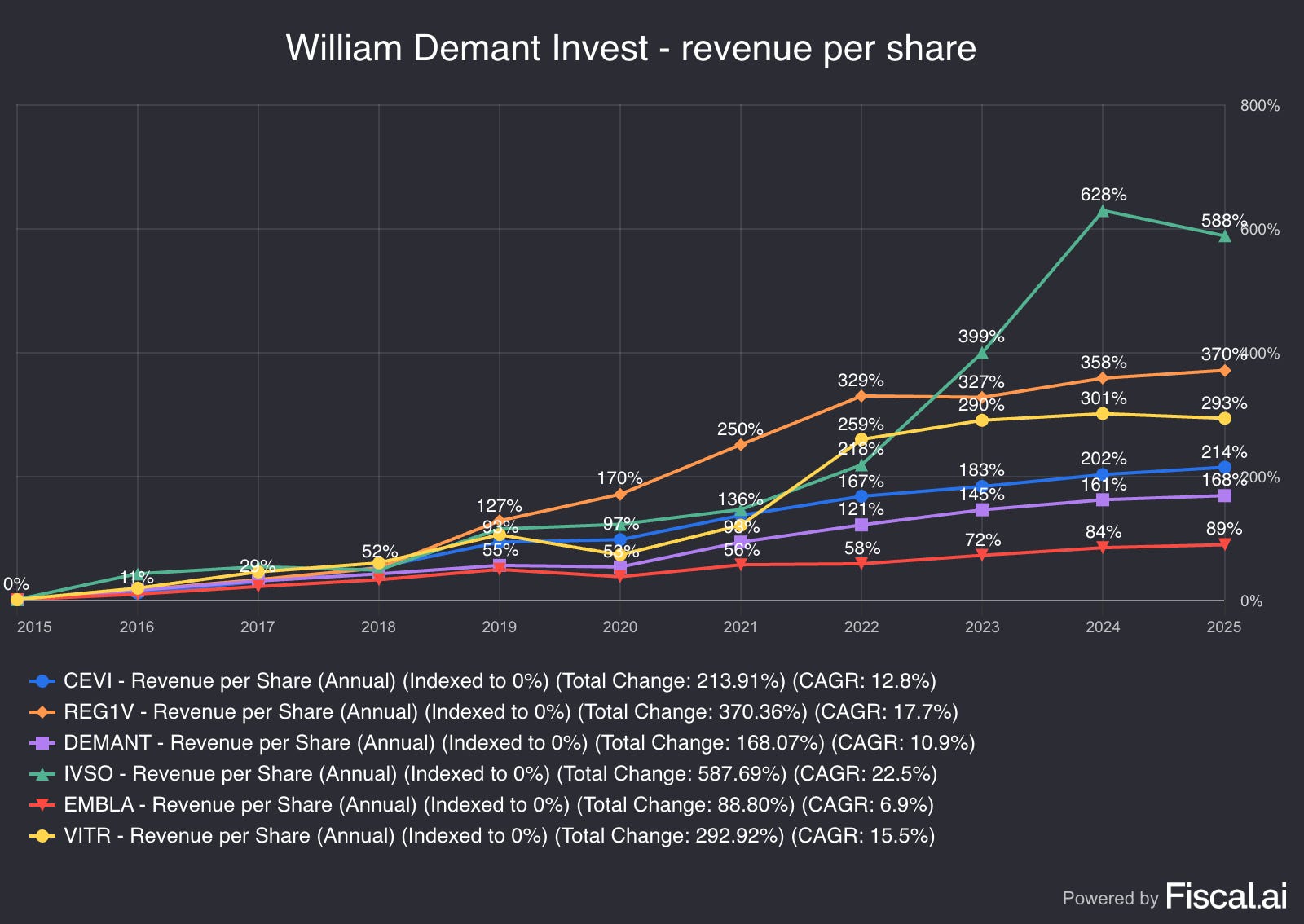

On average, we can see that all the publicly listed Industrial companies within William Demant have grown quite nicely over the last decade, ranging from 89 → 588%.

Invisio stands out with their growth in recent years, driven by their defence exposure, but even the average company here have compounded at 12% annually.

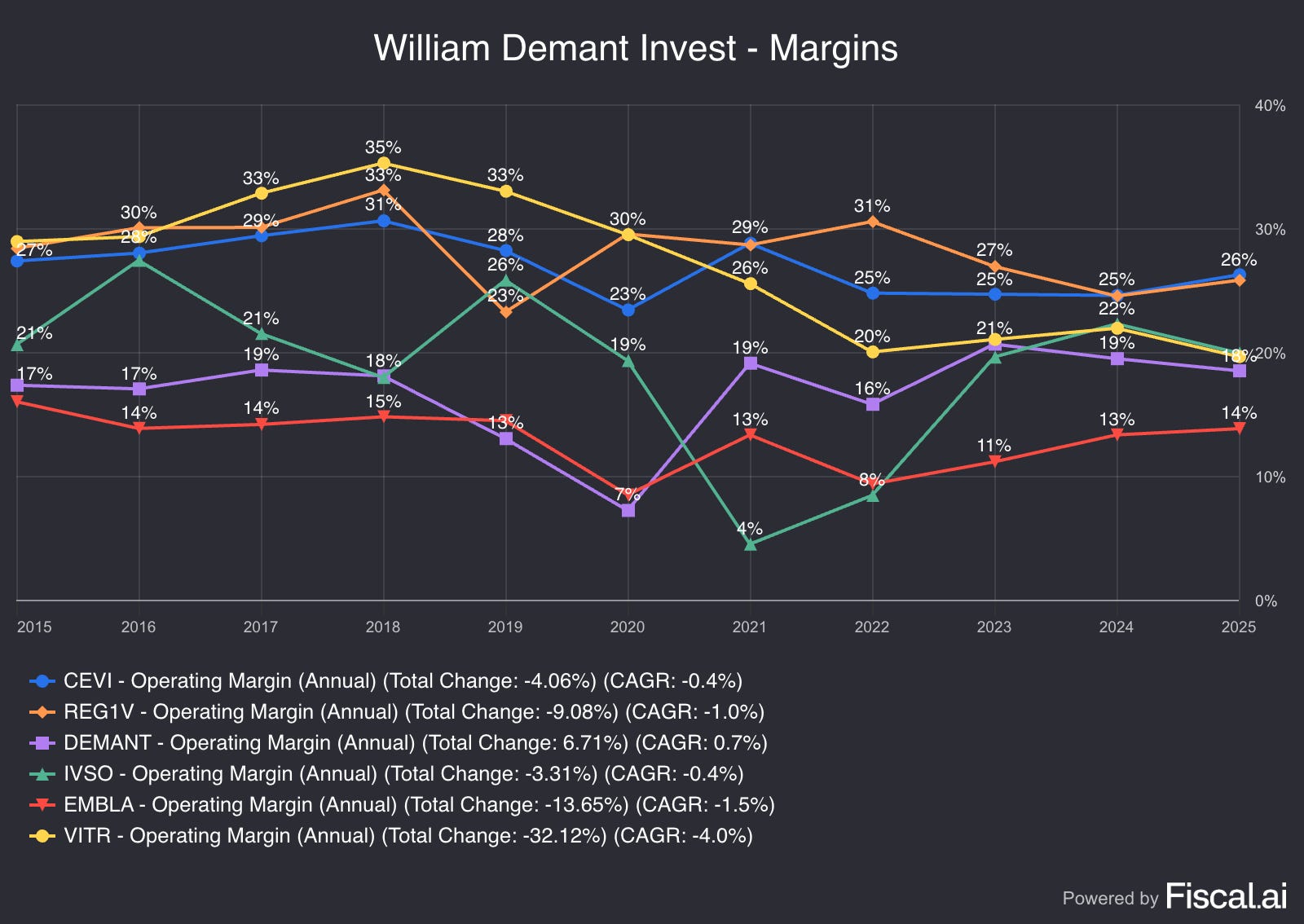

Combine the growth with the below operating profit margins, and we can probably conclude that these companies are of high quality. Average operating margins around 20% is nothing to be ashamed of in the Industrial context.

While the fastest-growing company, Invisio, excelled on growth, it came with volatile margins. In contrast, companies like Cellavision and Revenio Group stand out for their margin stability combined with double-digit growth.

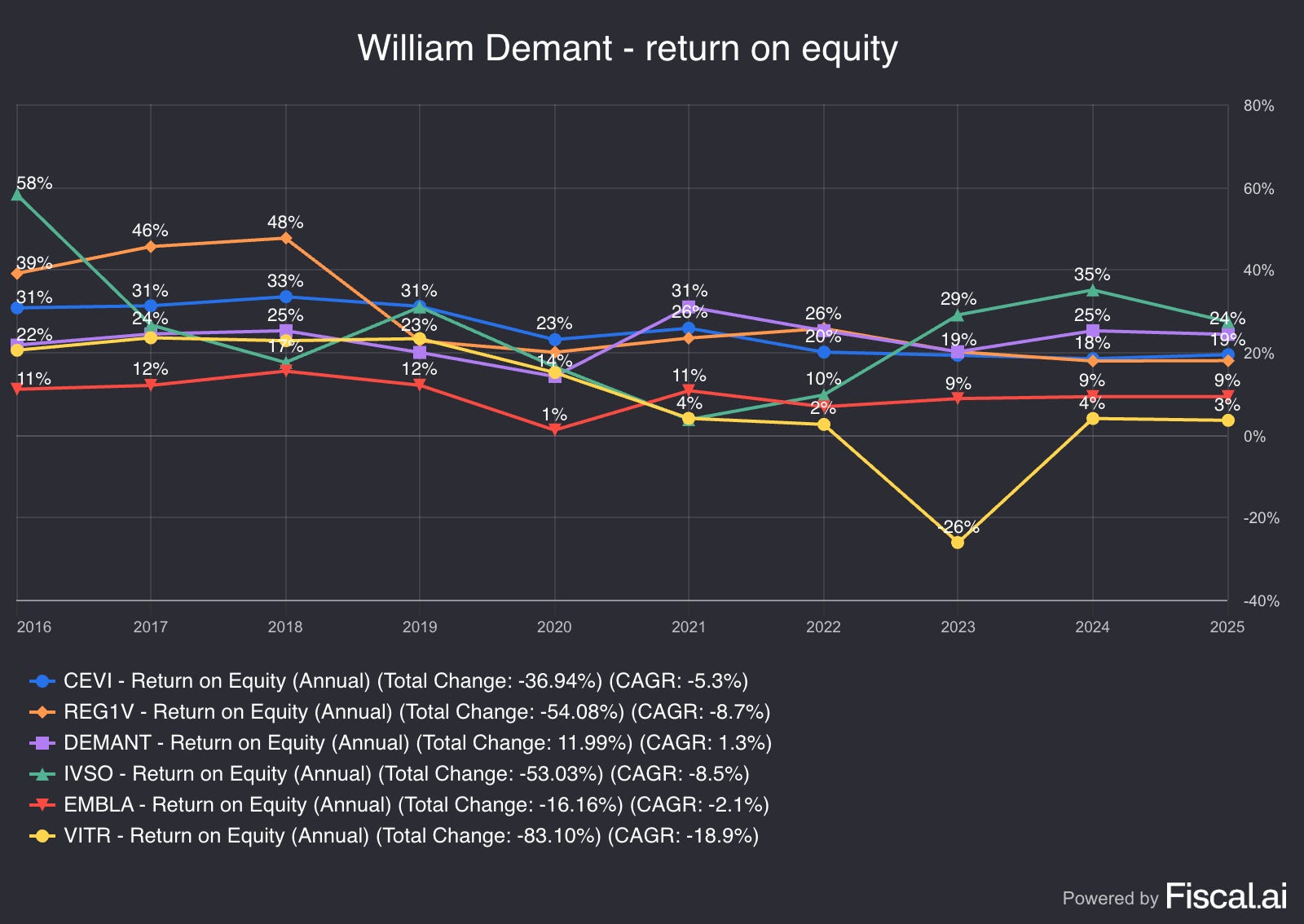

The final piece of the quality puzzle is how much capital was required to generate these fundamentals—essentially, the value creation efficiency.

One way to measure this is through Return on Equity (ROE) and leverage ratios. Ideally, a company combines high ROE with low leverage, meaning it generates substantial profits without taking on excessive debt. Across Demant’s portfolio, they carry roughly 1x net debt to EBITDA on average (ranging from -1→3x), while their ROEs are summarized below.

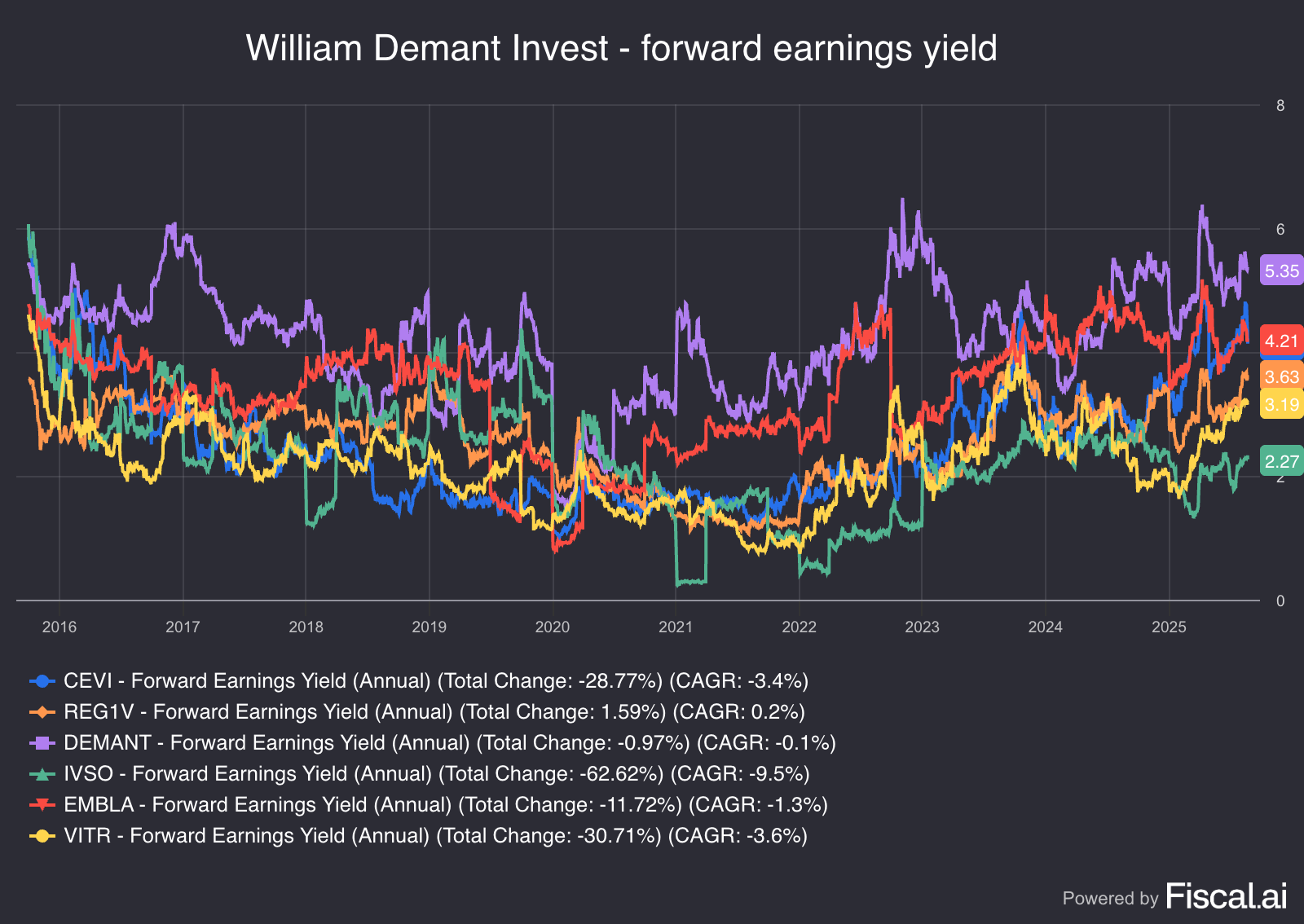

The final piece in this surface-level analysis is valuation.

As shown below, earnings yields are rising—equivalent to lower prices. While the market may be correctly pricing in a weaker outlook, we like this setup because even under conservative assumptions, the companies can still generate attractive returns.

Of course, only time will reveal how things unfold going forward.

Our take on William Demant

We can’t invest in William Demant Invest, so why bother looking at this?

Just from this simple and surface-level analysis, we would say 3 ideas here in particular, Cellavision, Revenio and Demant, all deserve a closer look.

Key Figures Cellavision, Revenio & Demant last 10 years:

Topline CAGR : 13%, 18%, 11%

EBIT margin: 26%, 29%, 18%

ROCE: 25%, 30%, 20%

Net debt / EBITDA: -0.6x, -0.2x, 3x

Forward Earnings yield: 4.2%, 3.6%, 5.3%

Forward EV / EBIT (10y margin): 19x, 19x, 16x

We are currently digging deeper into these companies, and if we uncover something worth highlighting, we’ll share a write-up. Before then, we are in the midst of our next Company writeup, which will be made available to all subscribers, so stay tuned.

But until then, let’s turn to our own portfolio for this month. (This section is exclusive to paid subscribers.)