Inside the Corner - Feb 26

Valuation models, Medistim attractive (?) and Portfolio Update

In the January Letter, we shared how we prefer to measure Intrinsic Value over time. Since then, we appreciated that buying stuff below that value is just one side of the coin, with the other being buying something that grows Intrinsic Value. Thus, we wanted to use this letter to share how we can value companies taking into account both these.

An approach we have not seen before, so we always welcome some feedback.

A north start to for quantifying Value Creation is Markel. They published their Annual Report this month, and the highlight below shows their methodology for doing so.

Markel use a simple 3-step framework to measure Intrinsic Value (adjusted profits x fair multiple ± balance sheet adjustments).

We believe this is the best way to measure a company’s success in the rear view mirror. While it can be used as a valuation tool, it’s one that only works of history repeats itself. To value a stock you usually have to look into the future, or at least see whether what’s priced into the stock sounds pessimistic or optimistic. And to be able to do any of this, you should have an opinion of Cyclicality.

Markel worked around their Insurance cyclicality, by multiplying 3-year averages of profits for an estimate of a fair multiple. This approach seem to work well.

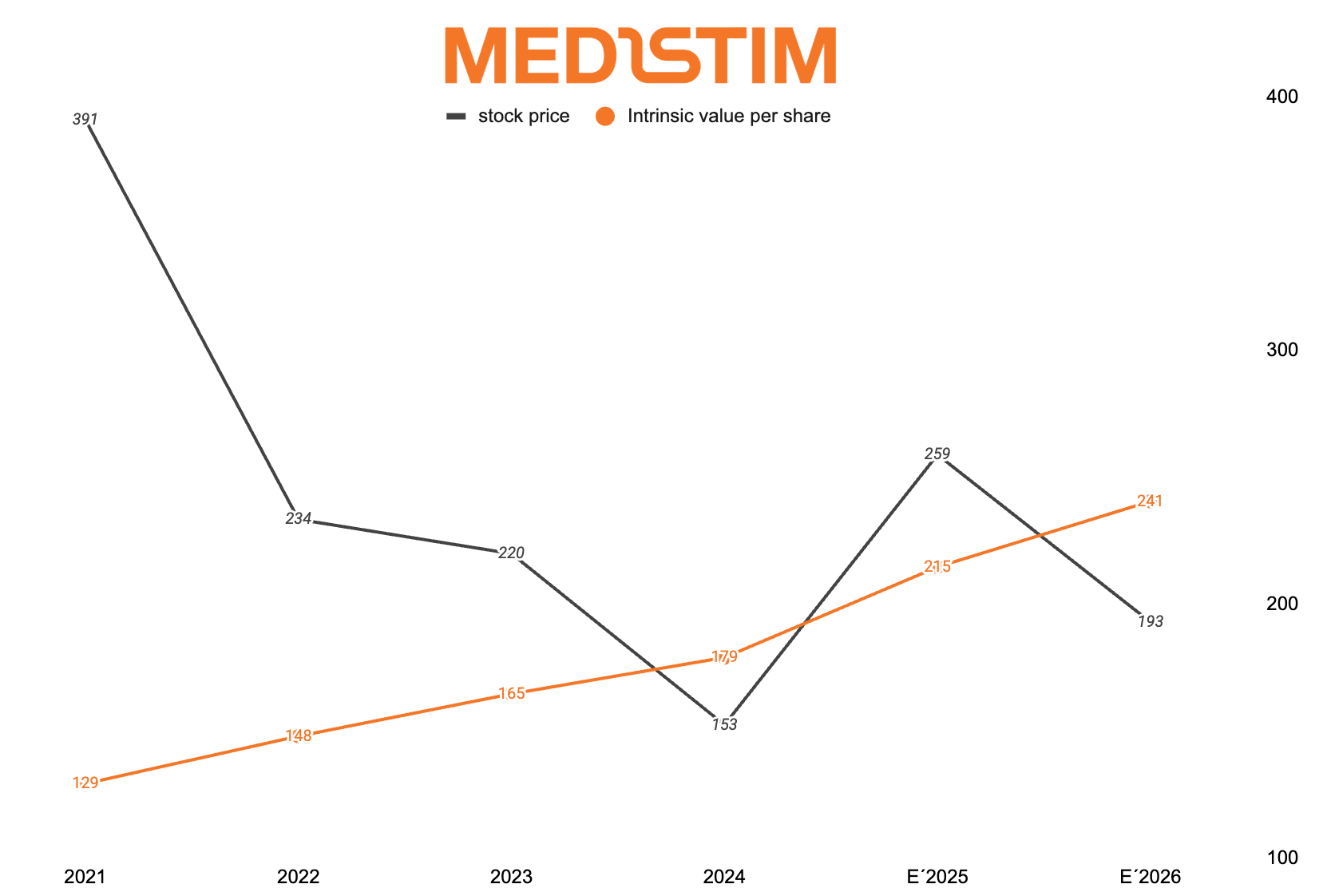

Below you can see we’ve done something similar with a company we own, called Medistim. While Medistim is among the more stable topline companies, their operating expenses and capital expenditures fluctuate somewhat, distorting the view.

However, we believe an investor trying to buy companies simply below Intrinsic Value would have a bias towards cheap companies not growing. They would miss the direction of that orange line, which in the case of Medistim, means long-term owners have time to their advantage, as their business keeps getting better (for now).

The problem of buying a dollar for 50 cents

A low purchase price can serve as downside protection, but as we illustrated with Medistim, so can a business compounding its’ value. Although, owners buying the stock for 80x business profits in 2021 may still disagree there...

We learned after researching Exor that buying something at a discount to NAV (in that example) is alone not very attractive, given the uncertainty around when (and if) that discount closes. If it occurs within one year, great — but then you may have to look for something else (if there aren’t other return drivers there).

The good thing about Exor is that they have grown NAV over time. The problem we have with Exor today, is that we do not know how to value it, nor estimate future compounding rate. The mix of cyclicals, high-priced luxury and other assets with minimal transparency makes it to hard for us.

Investor AB is a different beast. They have focused on stable profitable companies being good at reinvesting capital themselves, and reinvest their own cashflows continoussly at good returns into their wholly-owned Patricia Industries, in addition to some rare additions to their Listed Portfolio of Quality Companies. This makes it easier to value the underlying profits, and compare it to other opportunities.

Link below, to how we track Investor’s Intrinsic Value development over time.

But the question remains, why don’t we use a traditional method like DCF or just slap a multiple on today’s profits?

Why Not a Discounted Cash Flow Model or Multiples?

A DCF can work well, but most of the value usually comes from assumptions far out in the future — especially the terminal value. Change a growth rate or discount rate slightly, and the valuation moves a lot. We find estimating a decade out to hard.

Slapping a multiple on today’s earnings is quicker and can also be useful. But a single number doesn’t tell you much about durability, reinvestment opportunities, or how strong the business will look a few years from now. Cash conversion and how much cash can be distributed while growing are also key topics to keep in mind.

A Reverse DCF, trying to measure what today’s stock price implies about of future growth, can also be very helpful. Still, we prefer another way to look at valuation.