Inside the Corner - May 2026

AG Barr, Investor (ABB), MBB (DTS, Aumann), Shift4 and Adyen. + Lessons from Adnan (REQ) about Serial Acquirers.

When Charlie Munger told about never seeing Warren Buffett doing a discounted cashflow model, Buffett’s answer was strikingly clear.

“I mean it oughta just scream at you that you’ve got this huge margin of safety.”

Despite global indexes at all-time highs, we see many boring, stable businesses there now. Driven by their stock prices not being part of the markets momentum, despite their underlying businesses doing very fine (in some cases at least).

In this month’s letter, we’ll go through some things we learned this month, an update on a few key holdings and the Portfolio Update at last.

New Lesson for AG Barr

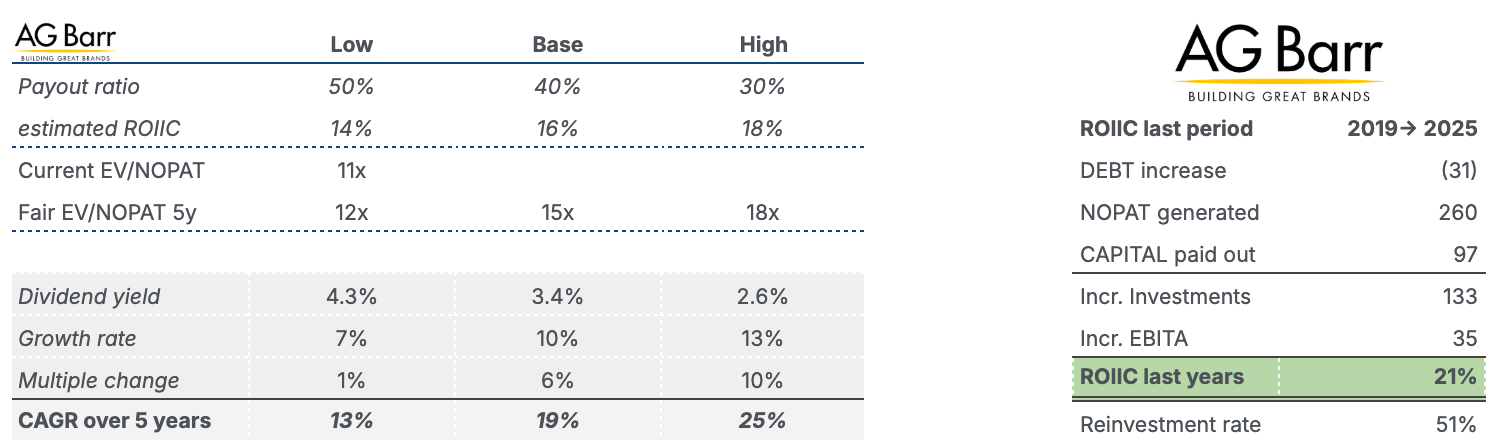

We recently called out AG Barr from the UK as an investable idea. With impressive incremental returns, a well positioned drink portfolio, net cash and a decade low earnings multiple (11x EV / 2026 NOPAT), we quite like AG Barr here.

That said, we typically avoid sizing positions up quickly. It takes time to learn the business and management well. As a result, AG Barr remains a small 1% holding for now, while we continue to learn more about the business and its durability.

One concern we’ve started to appreciate is recipe changes of Irn-Bru, as regulatory standards evolve — especially around sugar levels or certain additives. UK’s sugar tax could force Irn-Bru to another sugar reduction, which consumers did not like in 2018. With UK children’s sugar intake at twice what’s recommended, we can see why the government is pushing for such regulation. At the same time, there’s no doubt that AG Barr’s portfolio is gradually adapting to the changing demands over time, with more zero-alternatives and more drinks crafter with real fruit juice for instance.

Still, Barr is not in an industry with secular tailwinds, in contrast to several of our other holdings. That said, many beverage players seem worse positioned than Barr. With young consumers drinking less alcohol for instance, AG Barr’s exposure there is mostly their Funkin brand. And that category actually resonate well with young consumers, especially ready-to-drink cocktails.

Over the coming quarters, we’ll continue to follow AG Barr and learn more. For now, we think we’re being well compensated for the risks we can see. Another trait we like with AG Barr is that it’s more defensive than most of our holdings.

ABB driving Investor’s performance

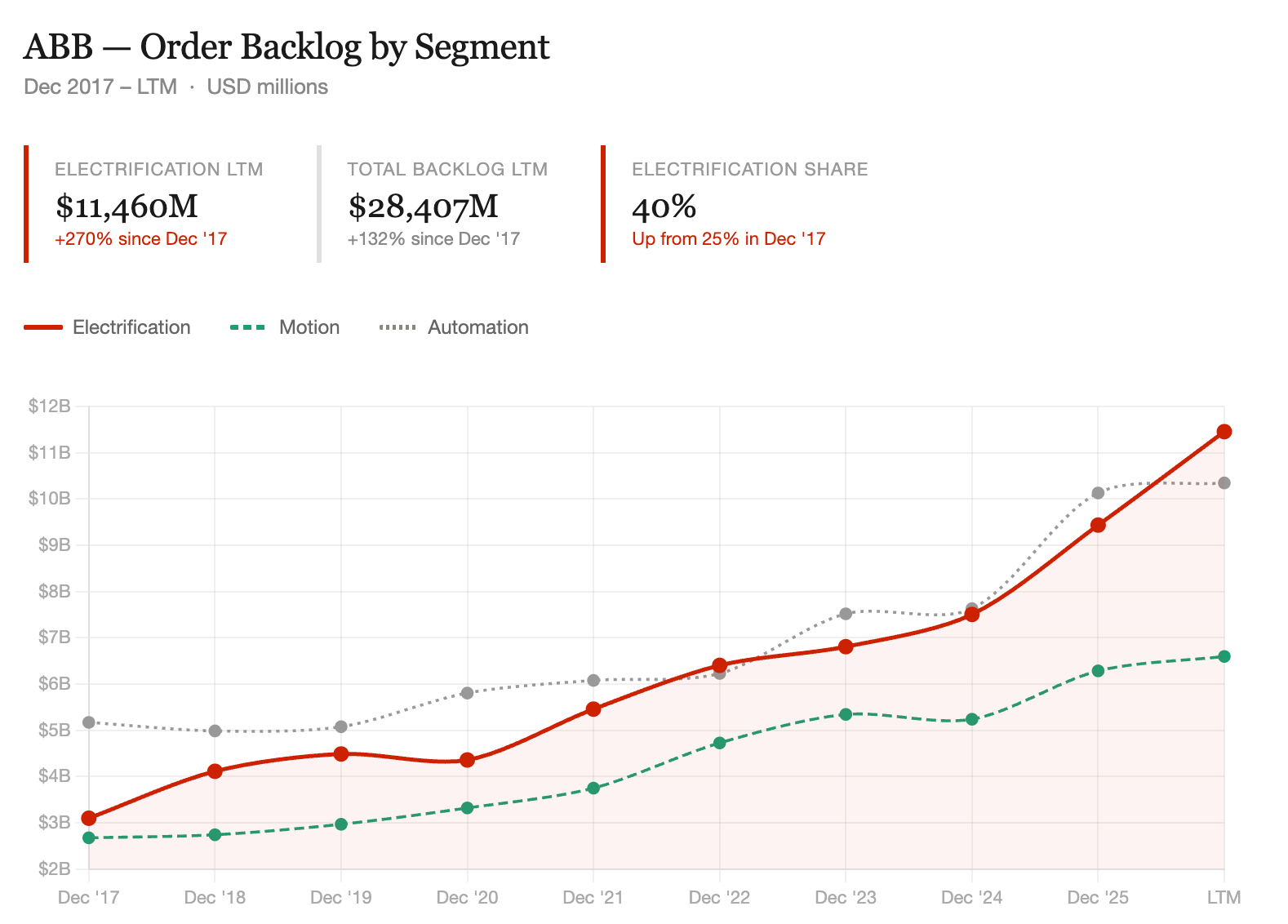

Since the end of March, Investor’s stake in ABB have grown from 199 billion SEK to 262. That means ABB currently occupies 21% of the Total Assets of Investor AB, almost double the weight of their second largest position, Atlas Copco.

A key reason for the growth in ABB’s market value is the Electrification segments Order Backlog. The chart below even understate the growth, as the LTM figure to the right only covers Q1, meaning that if growth was annualized, the red line will go through the roof. And their motion and automation segments, are still developing steadily up to the right, whereas their robotics segment was exited recently.

The catalyst behind the recent Order acceleration is AI infrastructure. The hyperscale data centre buildout requires vast amounts of power distribution and electrification equipment — precisely markets where ABB holds a leading position.

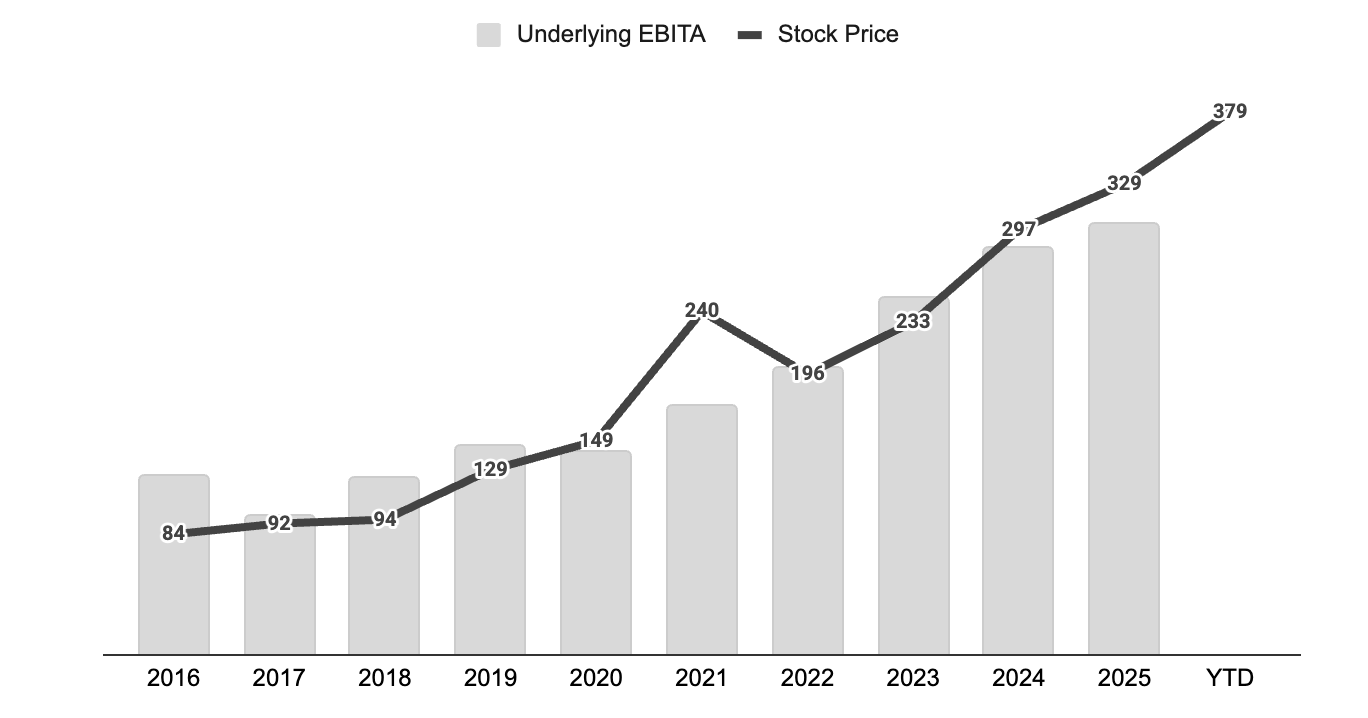

When it comes to Investor AB, this is another positive driver for underlying EBITA, which you can see illustrated below next to it’s shareprice. We continue to believe Investor’s portfolio is highly attractive longer term, and that the shareprice (black line) should follow the underlying EBITA (grey columns) over time. Let’s look at valuation.