Inside the Corner - November 2025

2 New Ideas within a Secular Tailwind, Portfolio Update and 3 Top Ideas in Portfolio

It appears to us that pockets of the market we really like are showing small signs of capitulation — even in companies we consider outstanding.

We like such environment as it provides long-term investors the opportunity to own durable companies, at attractive prices. When you don’t overpay for a good asset, you are less likely to have multiple contraction as a headwind going forward. Still, getting the business right often matters more than getting the price right.

In this month’s letter, we will go over:

I. Two watchlist Ideas solving the same problem, but with different solutions

II. A review of our own portfolio (for Premium members)

III. 3 companies we continue to add capital to currently

Investing behind long-term secular tailwinds can be powerful. When a business operates in a market where demand keeps expanding, its existing assets often generate higher incremental returns — provided the company is competitive enough that customers continue choosing its products and services.

Ageing Population, Screentime & 2 European Companies

Few trends are as strong as an ageing population. But, within eye-care, this trend is accelerated by the high screentime we’re seeing today. For every additional hour of screentime daily, the risk of myopia increases by 21%. Additionally, screen time has shown to reduce blink rate by ~66% on average, leading to dry eye. This is especially a problem for those using contact lenses, and perhaps also, those selling them.

I: Fielmann Group & Clinica Baviera

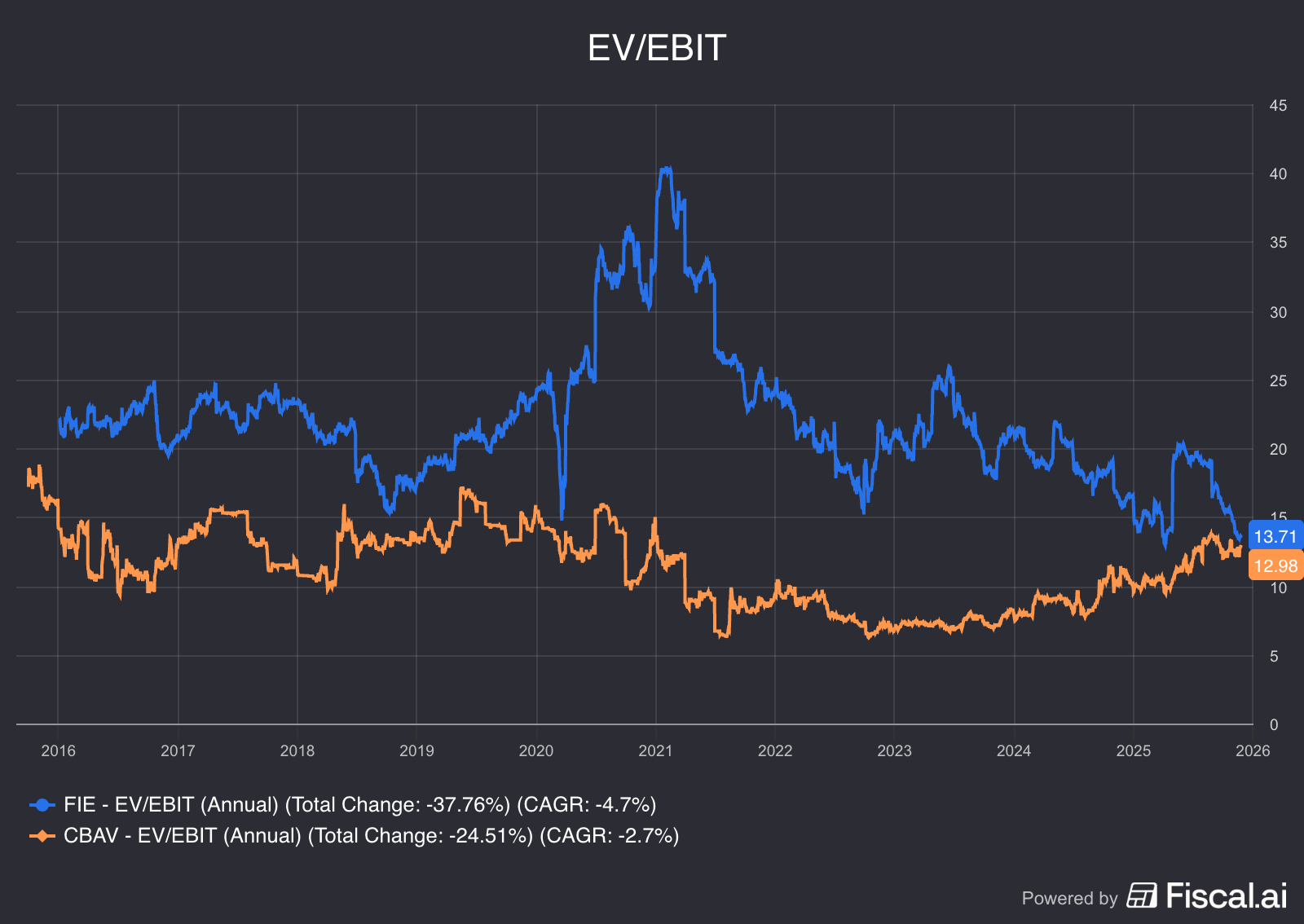

Fielmann Group, a European market leader in prescriptive eyewear and lenses, are a company positioned in the middle of this secular tailwind. However, as Exhibit II below highlights — the market has rarely had less faith in the future of this company.

Clinica Baviera, another European market leader, but in vision correction, also benefits from this secular tailwind. But in contrast to Fielmann who is selling a solution to your eye problems, Clinica tries selling a fix to your problem.

Exhibit II shows that the market is pricing both business at ~ 13x EV / EBIT — a price not expecting much growth from these tailwinds going forward.

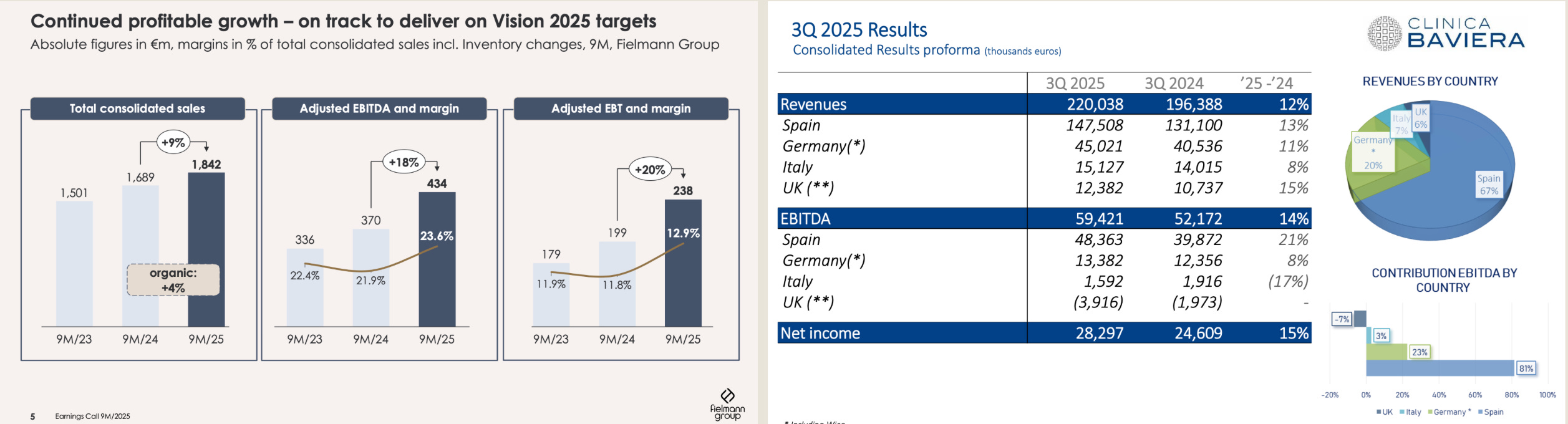

Looking at both companies updates for Q3 2025, shown in Exhibit III below, there is little evidence suggesting these businesses are struggling much so far.

Their recent results tell a different story.

Fielmann: +9% revenue, +18% adj. EBITDA

Clinica Baviera: +12% revenue, +14% EBITDA

Both have faced margin pressure due to international expansion (Fielmann in the US, Clinica in the UK), but trends are diverging. Fielmann’s US EBITDA margin improved from 7% to 14%, closing the gap to its European margin of 25%, while Clinica’s UK operations continue to weigh on profitability.

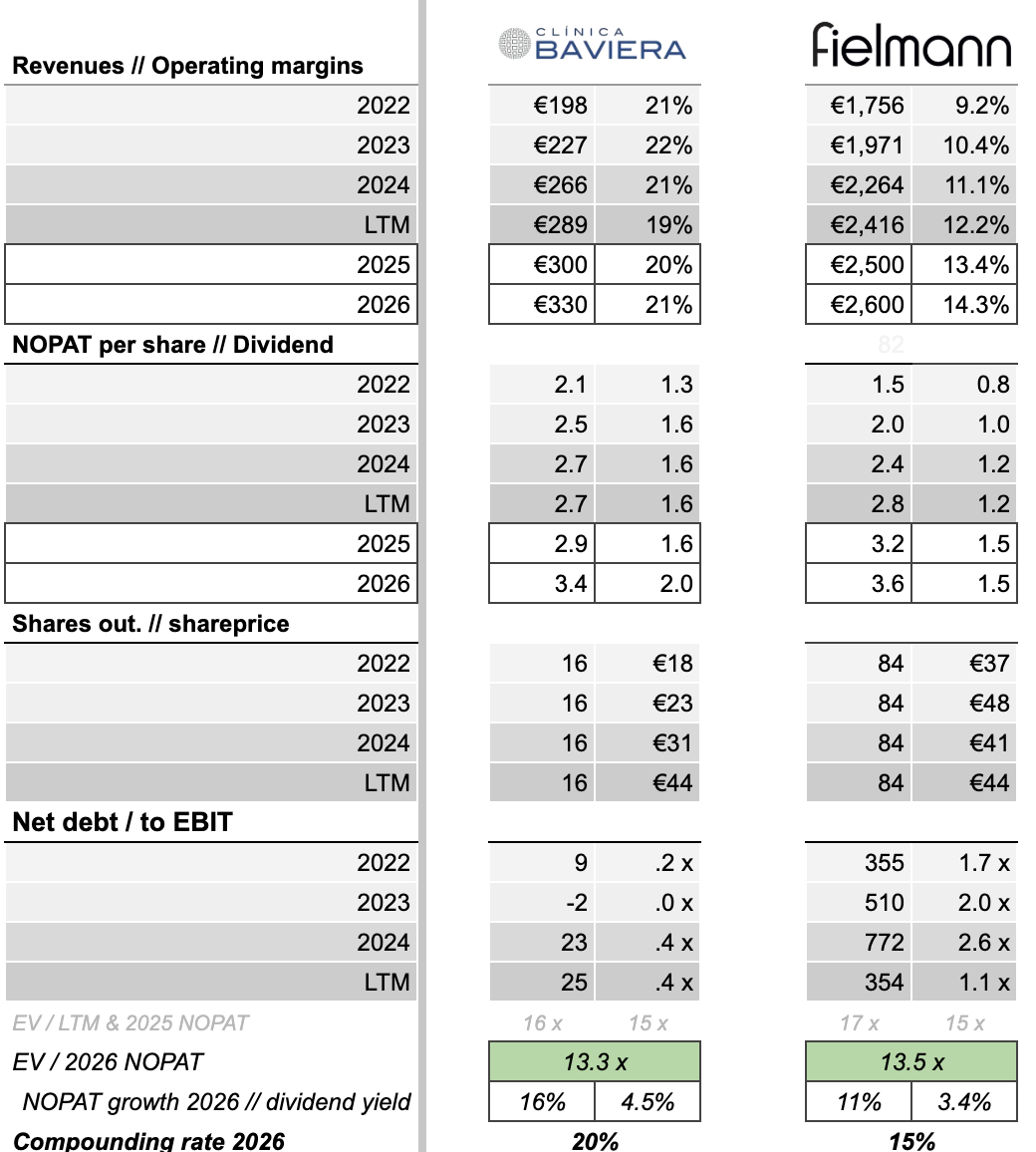

Financial KPI for Clinica & Fielmann

Below are the key figures we track for all our watchlist companies.

We view growth in NOPAT per share + dividend yield ± changes in the valuation multiple as a practical framework for thinking about forward return potential.

We believe this overview highlights that both Clinica and Fielmann are:

1) Growing faster than their underlying markets, thus taking market share

2) Reports strong margins, with recent margin improvement

3) Are able to both grow NOPAT per share while paying out dividends (good ROIC)

4) Low Net Debt to EBIT levels.

5) Rather low expectations for future performance, despite improving fundamentals.

In conclusion, we like both ideas — but there are a few points we think about.

First, both companies have controlling shareholders owning roughly 75% of the business. In Fielmann’s case, this is the Fielmann family. That’s not an issue for us; in fact, we generally prefer to align with family or owner-operators, as with MBB.

But for Clinica, which perhaps looks like the most intriguing case at first sight, the company is 75% owned by a Chinese giant called Aier Eye Hospital Group. However, we were less skeptical when we saw the fundamentals of this Chinese giant — topline growing 20% annually with operating margins and ROCE around 20% for the last decade. There are simply not many companies in the world with such figures.

To us, Aier’s majority stake in Clinica looks like part of their strategy to expand into Europe — while for Clinica, it provides access to the market leader’s expertise, capital, platform, and cutting-edge technology. Clinica’s shareholders, including the founding family still holding ~10%, have clearly benefited since Aier’s acquisition in 2017. With Aier behind them, Clinica has also shown the ability to expand into new geographies.

Another question we consider is durability: is the most robust model selling recurring solutions to a chronic problem, or solving it once and for all with a high-priced procedure? While Clinica’s “fix-the-problem” model is appealing, cost matters — the upfront price of surgery versus simply buying a new pair of glasses.

In our view, there is room for both models, each addressing different customer needs, painpoints and price sensitivities. Fielmann’s may be more stable during tough economic times, given the lower price points. Additionally, Fielmann have succesfully expanded into hearing aids as well — with good results so far.

We think both of these businesses look like interesting investment ideas, which we will look further into. (Note to new readers: We usually follow a company roughly 1 year on average before buying).

Disclaimer: This newsletter is provided for informational and educational purposes only. The analysis shared is based on my personal research and is not tailored to individual circumstances. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities.

II: Portfolio Update

As mentioned earlier, we are beginning to see signs of capitulation in several interesting names — including some we own, one of which we will detail shortly. By capitulation, we mean situations where share prices fall far more than fundamentals would justify. Mr. Market tends to overshoot both on excitement and on pessimism.

That said, we can always be wrong — the market may be correctly pricing a deterioration we have not yet identified. This is why position sizing is crucial, arguably the most important skill in investing. If you size positions so aggressively that you cannot withstand volatility or losses, you are playing the wrong game. The power of compounding only accrues to those who survive to play the next day.