Inside the Corner - September 2025

A look into the Constellation Software Universe and our September Update.

This month we take a look at how we value the complicated holding companies Constellation Software and Topicus. After that, we go over our Portfolio Update, which is exclusive for Paid Members. We’ve already covered both CSI and Topicus, first in our Serial Acquirer Writeup 2024 and then the Topicus writeup earlier this year.

Part I: The Constellation Model

Constellation Software and its European spin-off, Topicus, share a rare feature: decentralized capital allocation. Unlike most holding companies, where operations may be decentralized but capital allocation remains centralized, Constellation has evolved into multiple layers of capital allocators. We think this significantly lengtens their runway to continue deploying capital at their historic exceptional ROIC. We covered this in the writeup of Topicus earlier this year (link below).

Operating groups execute smaller acquisitions independently, while head office typically focuses on larger, more complex transactions — several of which we have already seen this year. This model is the underappreciated engine of value creation, but it complicates analysis: tracking reported revenue and margins is not sufficient. Investors must also consider subsidiary ownership, minority interests, and ultimately how much economic value flows to shareholders. And with this model, it may make sense that we could see further spinoffs in the future, like that of Topicus or Lumine.

To cut through the noise, we maintain detailed tracking models — similar to those we have built for Investor AB and MBB — focusing on distributable cash flows before growth investments.

Capital Deployment — The Core Driver

The durability of Constellation’s acquisition engine is the single most important factor for long-term value creation. Organic growth in their vertical market software (VMS) businesses tends to be low- to mid-single digits, but they consistently delivers high ROIC by buying companies cheaply.

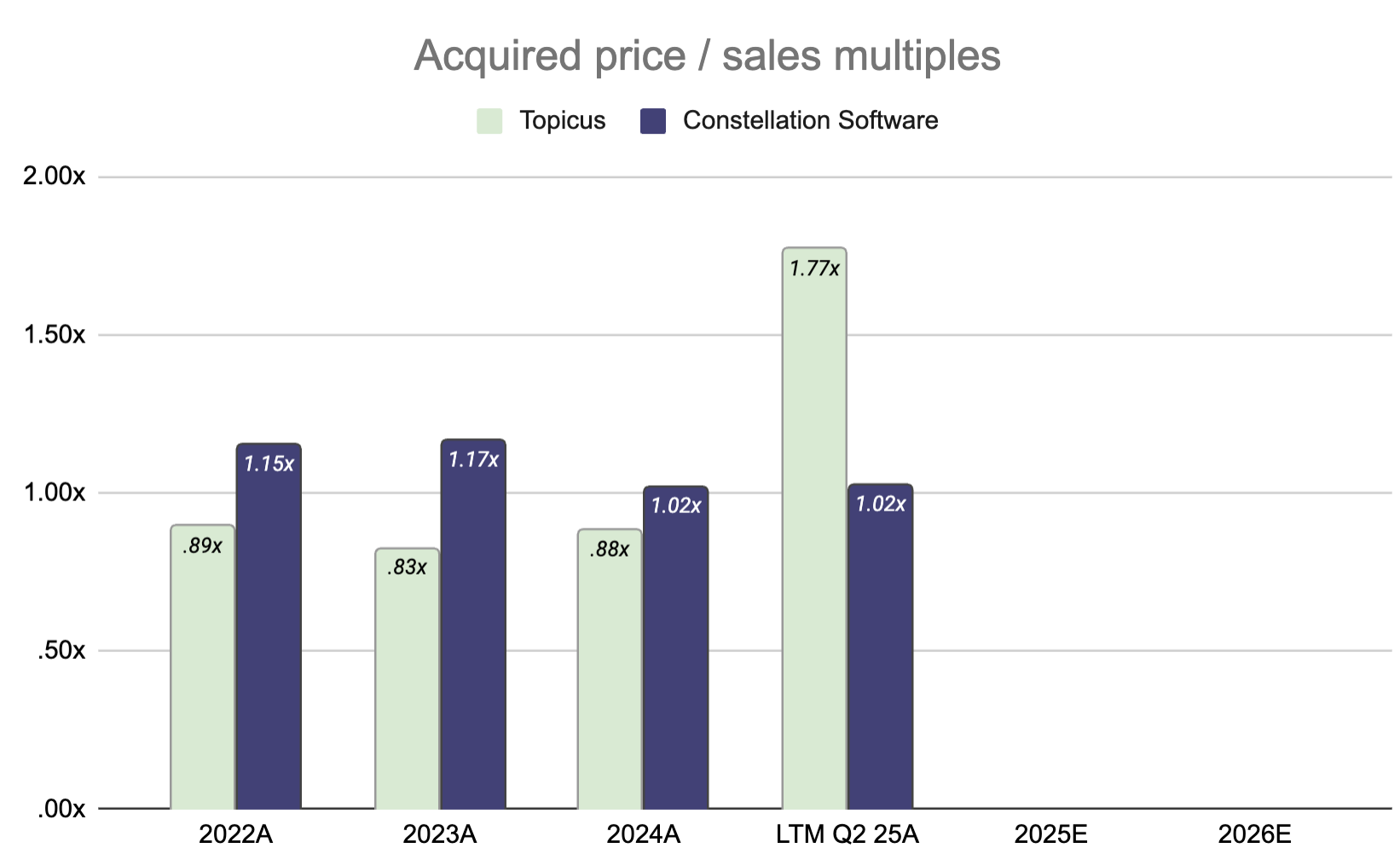

In Exhibit I below, we’ve illustrated just how cheap. Historically, Topicus has paid slightly lower multiples than CSI, despite stronger margins. This changed in 2025 with Topicus’s purchase of Belgian software company Cipal Shaubroeck, at nearly 2x sales - more than double its usual entry multiple. It should be noted that despite CSI paying slightly more for their average deal, they have maintained a more consistent high-reinvestment engine, despite being significantly larger.

The bear case would be that multiples paid go up or/and reinvestment rates fall. Or perhaps that organic growth detoriate and turn negative.

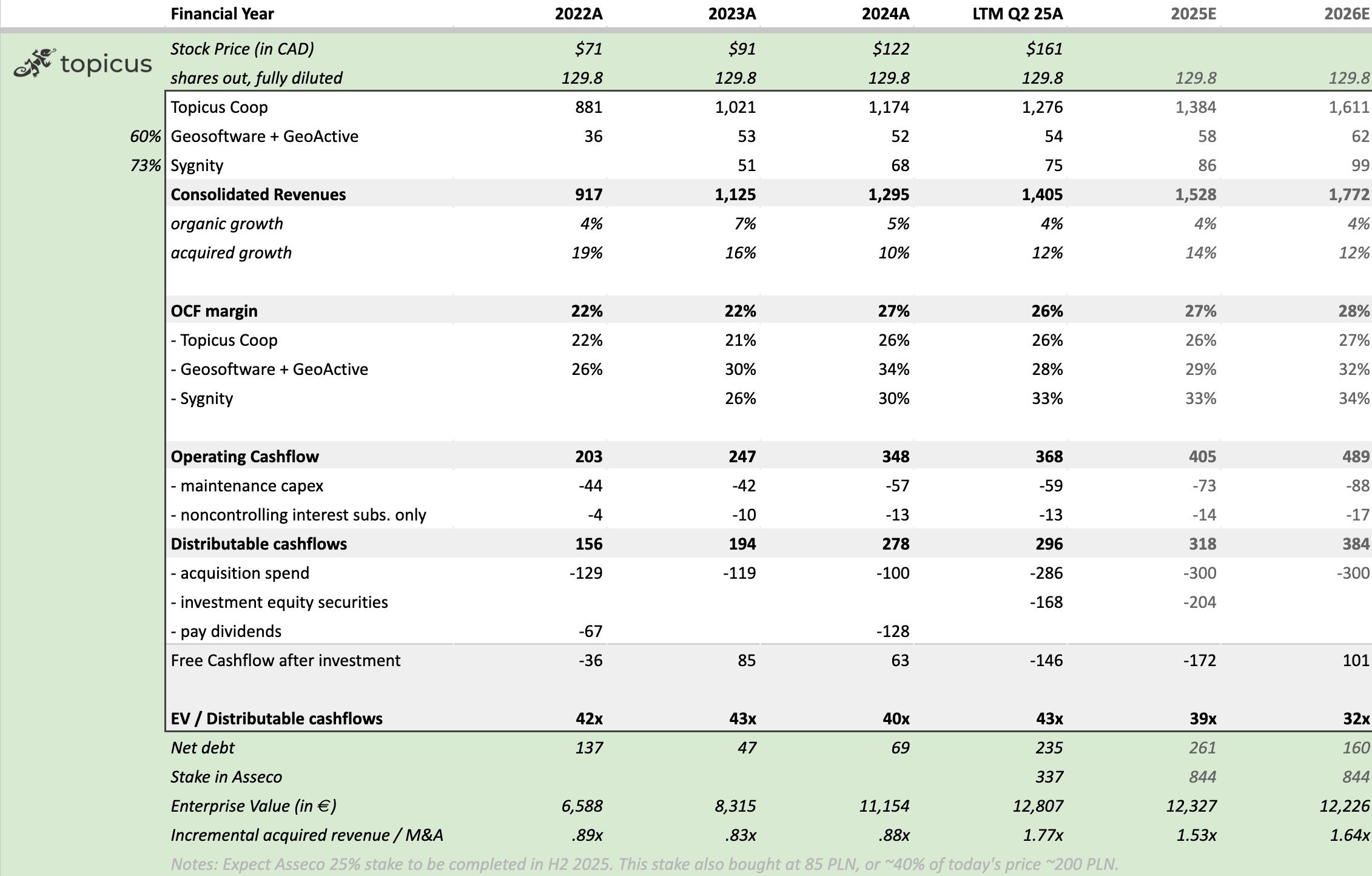

Topicus ($160 CAD per share)

Topicus has two layers of non-controlling interests we need to consider:

Subsidiary level — in entities like Sygnity, GeoSoftware, and GeoActive.

Holding-company level — through other Topicus shareholders, such as Joday Group.

Following its minority investment in Asseco Poland, we prefer to calculate the market cap for Topicus using fully diluted shares outstanding. This eliminates the need to adjust for holding-level non-controlling interests (e.g., Joday), while still accounting for subsidiaries. We could also use basic shares (~65% of diluted), but then we would have to deduct the ~35% non-controlling interest as well.

The Asseco investment is a good example of the capital allocation skills at work. Topicus acquired a 10% stake early this year at 85 PLN per share, roughly 60% lower than the 200 PLN its trading at today. And, pending regulatory approval, this stake may raise to 25%, also at PLN 85/share. If completed, the value of the stake would rise from €337m to ~€844m, making Asseco a material part of Topicus’s value.

In Exhibit II, you can see the metrics we keep track of for Topicus.

Given we are already in September 2025, we find forward estimates for 2025 and 2026 more relevant than trailing results when assessing valuation.

On a distributable cash flow basis, Topicus trades at roughly 43x LTM, 39x 2025E, and 32x 2026E. Importantly, both Topicus and Constellation report free cash flow available to shareholders more conservatively than peers.

Where the general operating cashflow less physical capital expenditures is commonly used to calculate operating cashflow, Constellation also include other cash outflows, like interest paid on lease and debt obligations. They also pay employees’ bonuses in cash, where parts of it is required to be invested in company shares. This in contrast to most, who issue stock-based compensation, diluting shareholders and overstating actual operating cashflows, as the alternative would be paying employees in cash. Either we have to include it as a cost, or we have to look at per-share value.

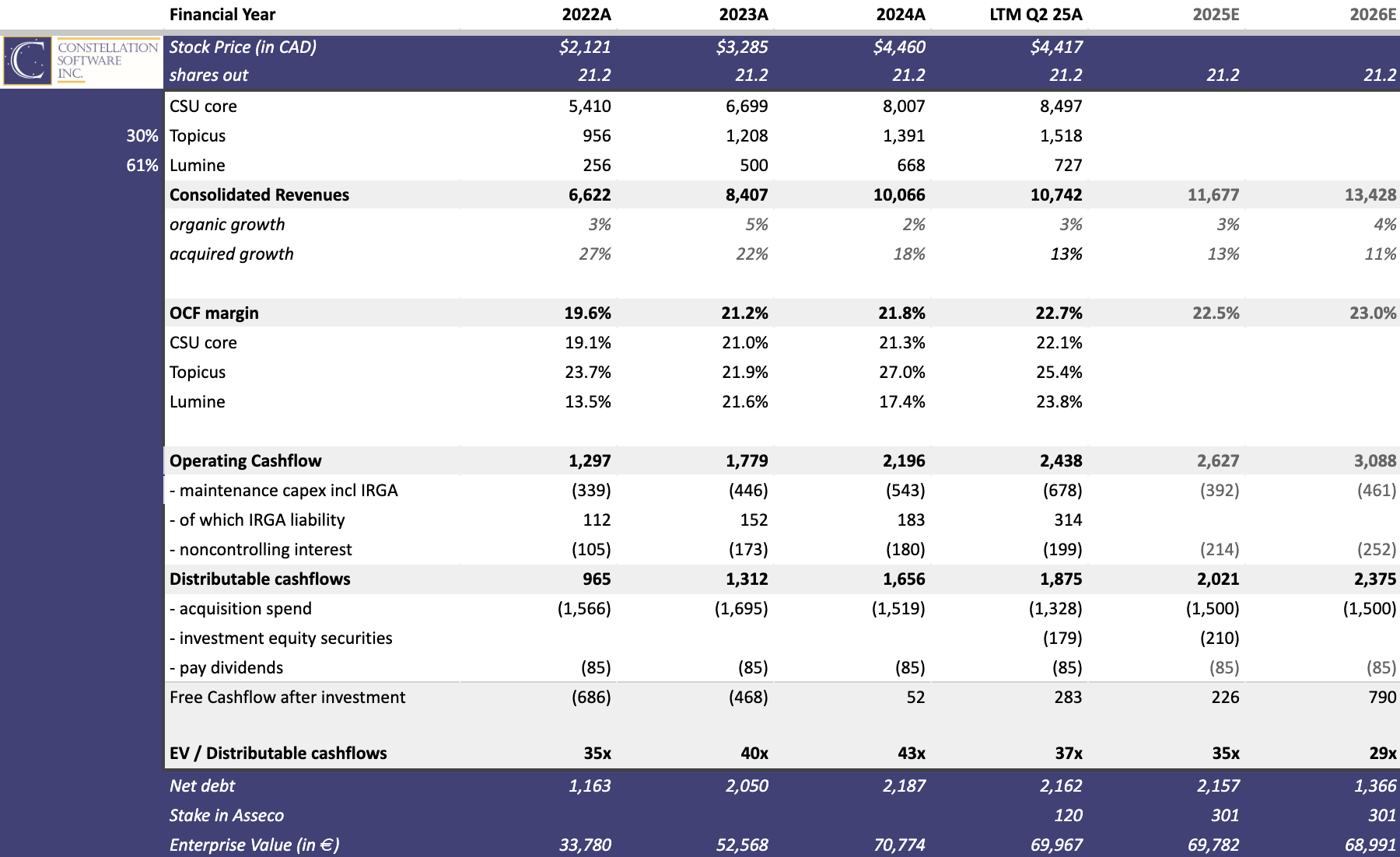

Constellation Software ($4400 CAD per share)

For CSI, we adjust reported FCFA2S by adding back the IRGA liability (USD 1.0bn at June 30, 2025). While booked as a liability, it effectively acts as a strategic asset.

The IRGA gives Joday Group the right to sell Topicus Coop units to CSI at a formula-based price tied to revenue and tangible assets, not market value. This means that as Topicus grows, the liability increases, but CSI gains the ability to acquire more Topicus shares at a steep discount. In practice, the IRGA represents embedded optionality, not a burden.

On this adjusted basis, CSI trades at ~35x 2025E distributable cash flow and 29x 2026E, roughly 10% cheaper than Topicus. We see reasonable arguments for either deserving a premium: CSI for its scale and track record, Topicus for its earlier stage and runway. So far, we have leaned toward Topicus, whose smaller market cap means each acquisition moves the needle more meaningfully.

AI — Management presenting their thoughts

On September 22, Constellation Software management will present its perspective on how Artificial Intelligence may affect their business. The discussion could have important implications for assumptions around long-term organic growth rates and the pipeline of acquisition opportunities.

At present, it remains unclear whether AI will be a net positive or negative for vertical market software. On one hand, it could challenge established niches; on the other, it may unlock opportunities previously unavailable, potentially also creating room for greater returns on organic capital deployment alongside acquisitions, either by need (competition) or to increase the value proposition for sticky software customers.

Given CSI’s track record, we are eager to listening to management’s view on this, but also how they view the terminal value of the average VMS business in their portfolio.

Part II: September Portfolio Update

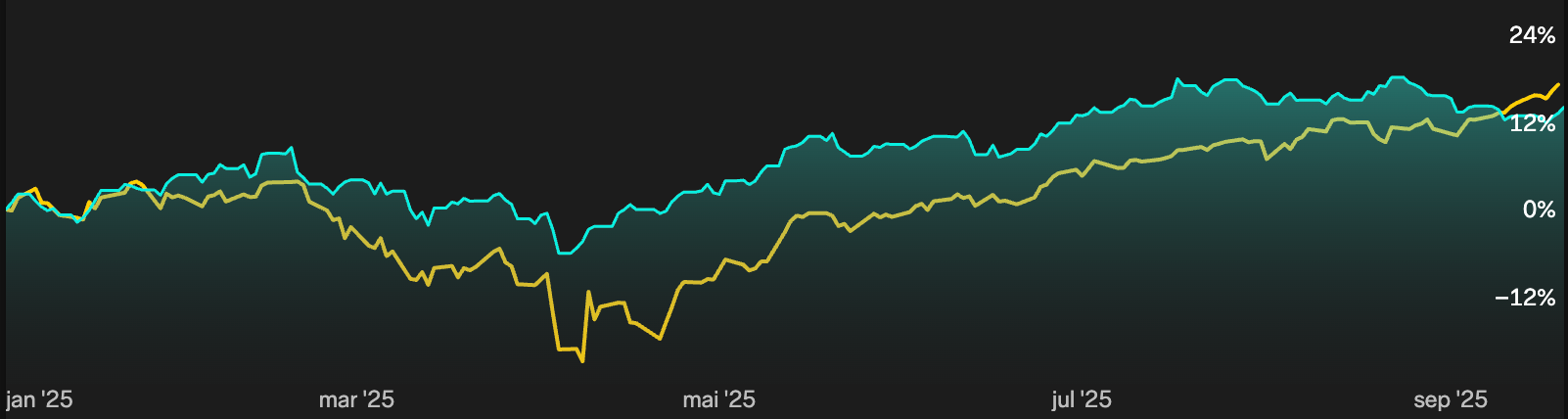

This month, we exited one position and added to key holdings we found attractively priced. Our portfolio is now up 14% YTD, recently being surpassed by the Nasdaq, as shown below. While we will admit we can feel some FOMO from time to time, seeing many megacaps continue to rise, we cannot do other than congratulate those of you who’ve held onto recent winners like Google and ASML (among many others). While we haven’t participated in those gains, we have been positively surprised with the stability of our portfolio over the last couple years.

Today, we will go over our Portfolio, and cover a couple ideas of ours. At the end, we will publish our investment thesis on a holding we haven’t discussed much before.

This part is exclusive for our paid members, if you consider becoming one, it costs $8 per month or $60 per year.