Investment AB Latour

Excellent Track-record shadowed by NAV premium finally being closed.

Disclaimer: This newsletter is provided for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities. The author did purchase shares after writing this.

For the first time in 8 years, Latour is priced at a discount to its Net Asset Value. Let’s look under the hood of this $14 billion Holding Company, and ask whether the market has handed us a good entry point into one of Europe’s finest compounders.

Latour was founded in 1985 by the Douglas Family, who remain the controlling shareholder to this day, with four decades of skin in the game.

With the press of a button, we have the chance to partner with these market-beating capital allocators and the portfolio they’ve quietly compounded for 40 years. 15% annually over the last 25, a return that puts most institutional investors to shame.

But perhaps just as impressive as the returns is the patience behind them. Look 20 years back, and you’ll find roughly 70% of today’s portfolio holdings there!

This is not a private equity firm with an exit mandate and a short-term horizon. Latour operates as a permanent home, predominantly for industrial businesses. And the crown jewel is Assa Abloy: the $40 billion global champion in doors and locks.

And yet here’s the detail that separates Latour from most holding companies: its outperformance has not been driven by its largest holding. The portfolio ex Assa Abloy has actually outperformed the market-beating giant itself — a dynamic that stands in sharp contrast to another Hold’co like Exor or Prosus, where the growth story has been driven more by their largest investment alone.

This, more than anything, may explain why this holding company has commanded a premium to NAV for the better part of a decade. That premium is now gone.

Content:

Management & The Douglas Family

Track-record

NAV Premium / Discount

Latour’s Portfolio with extensive Data Breakdown

Wholly-owned

Listed Holdings

Underlying Valuation

Relative to Investor AB & Lifco

Market Optimism turn sour

Conclusion for our own Investment Journey

Management & The Douglas Family

The irony of partnering with the Douglas Family is that it costs less than the average fund manager — despite a vastly superior track record. Latour runs a Headquarter of only 16 people, with management costs below 0.1% of assets. The family owns 76% of the company and the group is designed to empower decentralized operations.

Gustaf Douglas (1938–2023): The Architect

Gustaf is the man who engineered Latour. Pushed out of his CEO role at Sweden’s largest newspapers for running conflicting private investments, he pivoted to industry and in 1985 negotiated a corporate swap — exchanging his stake in the Skrinet group for a subsidiary (AB Hevea) that came with a 95% stake in Securitas and 25% in Trelleborg. AB Hevea was renamed Investment AB Latour in 1987.

His philosophy was clear: “My role would be an active owner — not to vote with my feet, but to take responsibility for governance and control.”

ASSA ABLOY is a key part of the Latour’s story, which Gustaf co-architected in 1994. Latour remains its largest shareholder today, and the stock is a 100-bagger since the early 2000’s. Such concentrated long holdings remains the backbone of Latour’s long-run returns, benefiting from compound interest.

Gustaf passed away in May 2023, aged 85, having compounded the share price at ~22% annually since inception — a 3,000-fold return over 40 years.

The Keys Pass to Eric & Carl

Gustaf didn’t hand over Latour suddenly — he handed it over slowly and deliberately. Eric joined the board in 2002 and Carl in 2008, both spending years learning the business alongside their father before Gustaf’s passing in 2023 marked the formal transition. Succession done well.

The brothers combined stake carries ~79% of votes, protected by a dual-class share structure common among Scandinavian holding companies. One meaningful distinction from Investor AB, however, is that the Wallenbergs hold their stake through family foundations — a structure explicitly designed to bind future generations to a common mission and prevent fragmentation. Eric and Carl own Latour more directly, which raises a legitimate long-term question: what happens in generation three?

On operations, the family governs — they don’t run the business. The previous CEO, Jan Svensson, ran Latour for 17 years and delivered ~1,500% total return during his tenure, nearly 3x the broader market. His successor, Johan Hjertonsson, was appointed in 2019 after running Fagerhult — a Latour portfolio company — for a decade. The family watched him execute with their own capital at stake before handing him the role.

CEO tenure of 17 years and insider hire says a lot about the culture within Latour. The Douglas family clearly thinks in decades rather than quarters.

A final encouraging signal: Insiders, including Eric and Carl, have been adding shares at current prices. Buying more of something the majority of your wealth is already tied into is a strong statement — and notably, these purchases came after the valuation premium collapsed, not during the frothy years of 2021.

Insiders might sell their shares for any number of reasons, but they buy them for only one: They think the price will rise (Peter Lynch)

Track-record

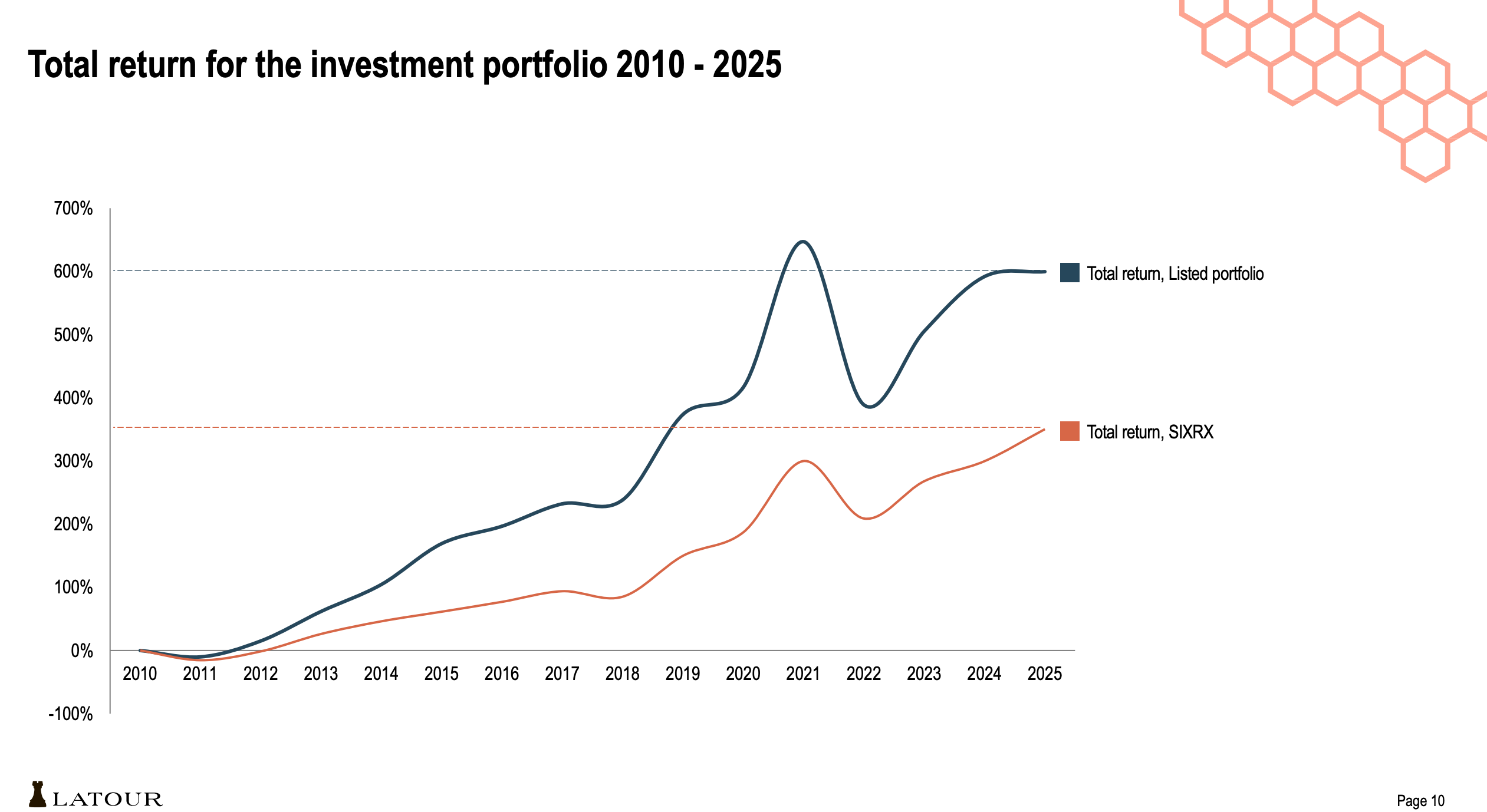

Similar to Investor AB, Latour has had market-beating results both from its Listed Investment Portfolio and Wholly-owned Portfolio over time. Remember, the majority of investors (both retail and professionals) don’t beat the index over time.

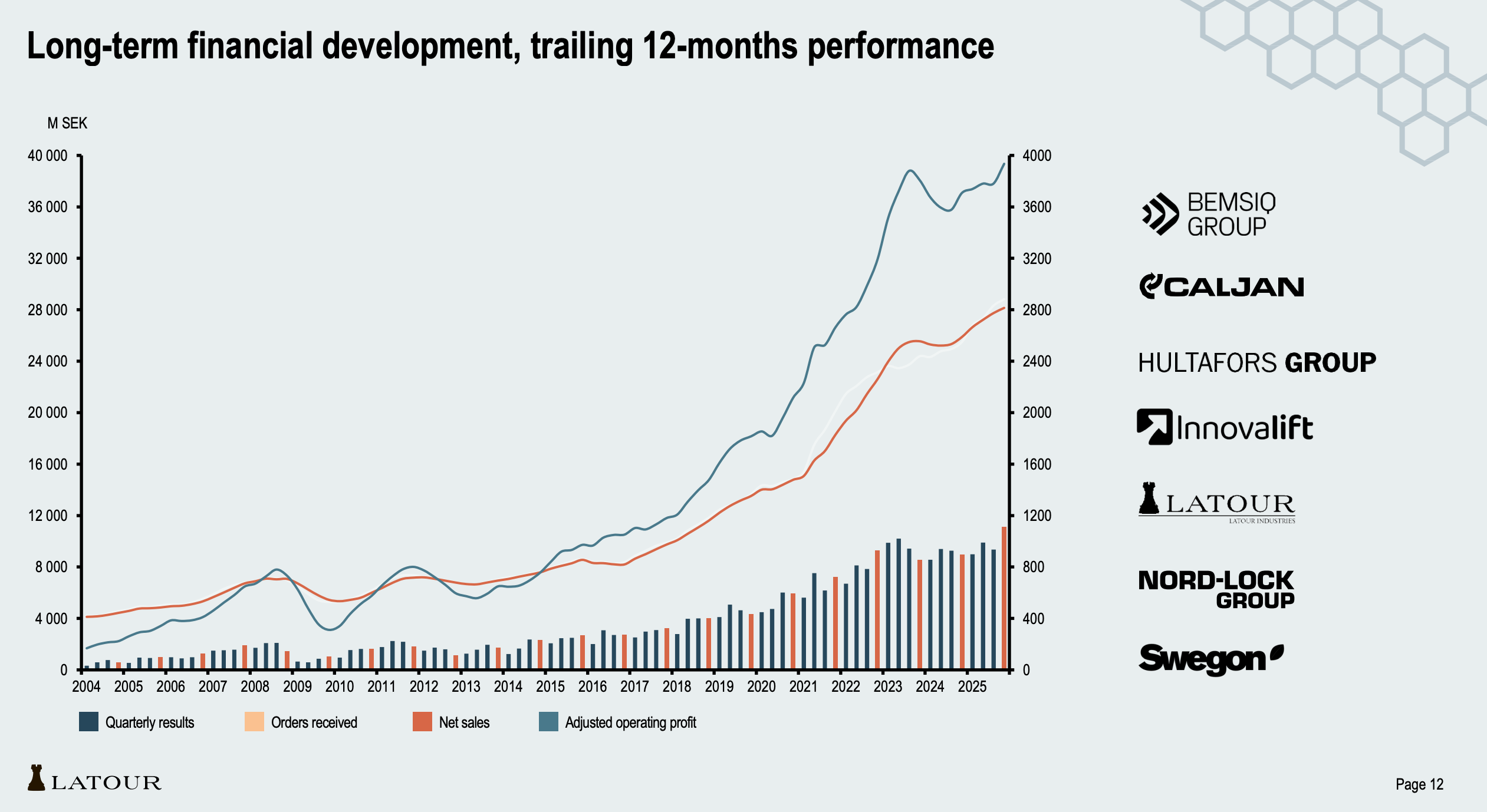

Below, you can see the Financial Results of the Wholly-owned Portfolio. Compounding sales at high rates with improving profitability over time.

These 2 charts combined show that Latour is both a great capital allocator and a good operator of businesses. Additionally, they’ve been able to partner with other great capital allocators / operators on the public stock market. This creates what we previously referred to as a Dual Engine for Growth for Investor AB back in 2024.

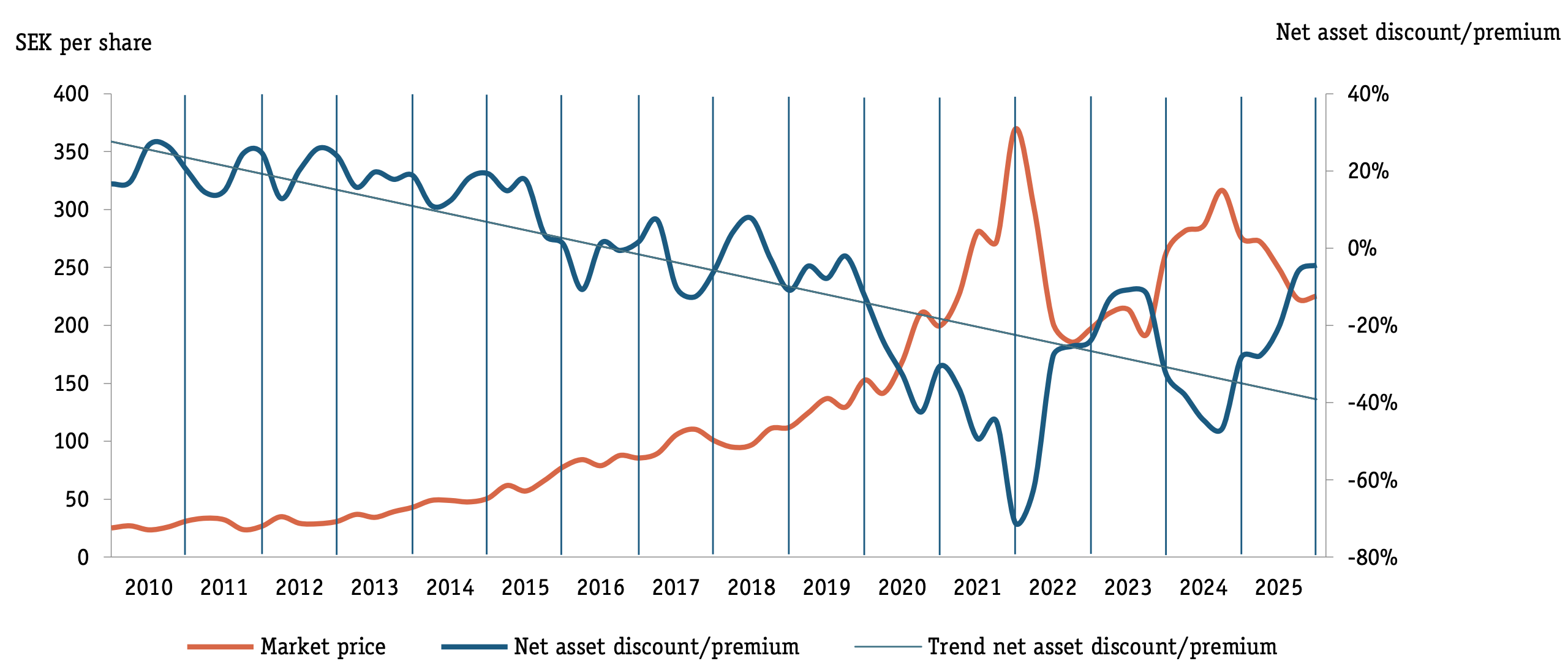

Net Asset Value Premium / Discount

Given this track-record, we think it could explain some of the unusual high premium the market has assigned to Latour’s Net Asset Value (NAV) in the past. While many Holding Companies trade at a substantial discount to its assets, the market decided to price Latour at a 70% premium late 2021!

That premium is now gone and the portfolio trades again close to NAV. This explains the poor 5-year returns for Latour stock.

A good argument for why the discount has closed, is that in recent years, the NAV growth have actually underperformed the SIXRX index, lastly at 2025 with only 2,4% growth vs the 12,7% increase for the index.

While a premium or discount to NAV usually gets most of the attention, there is little doubt that management and the controlling owner, The Douglas Family, has done an excellent job compounding the underlying profits of Latour over the long term.

Latour’s Portfolio

Wholly Owned Holdings (47% of NAV)

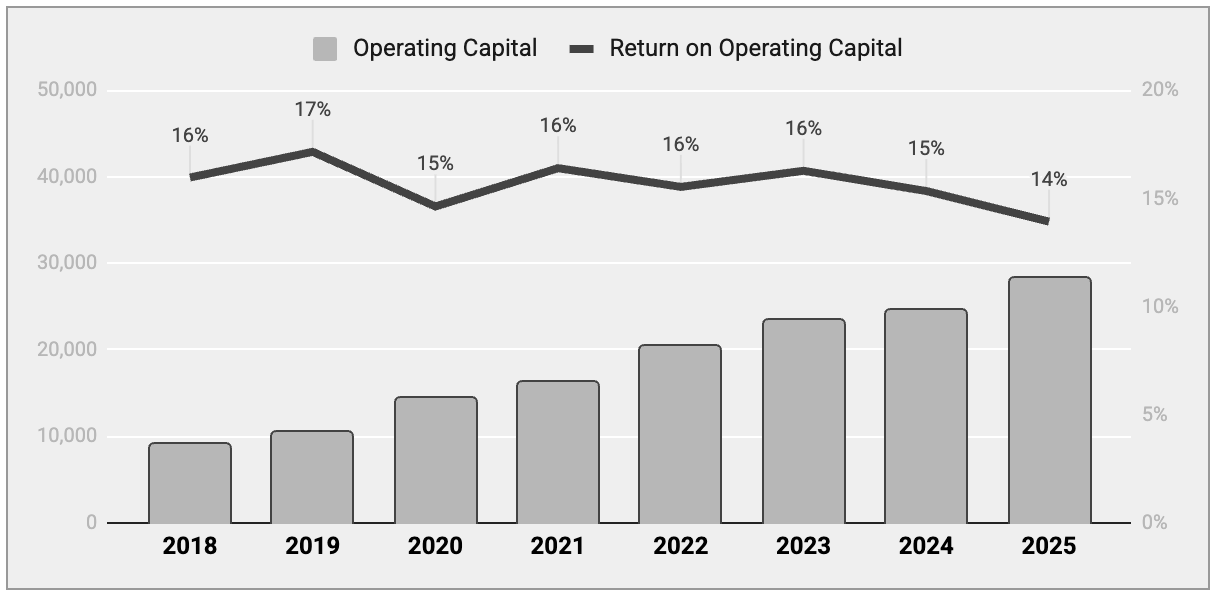

The main takeaway from the Wholly Owned Portfolio is that it’s a high quality Industrial. Organic growth averaging more than 5% combined with solid acquired growth, means this portfolio have compounded EBITA by 13% annually since 2018.

The organic growth has on average been 2% higher than the inflation rate in Sweden. Operating margins have expanded and Return on Operating Capital have been stable around 14 → 17% in this period. Note that the wholly owned companies also conduct acquisitions by themselves. This gives the Group a high reinvestment rate, which we can see in the growth in Operating Capital below.

The wholly-owned portfolio has been a growing share of NAV over time, but it’s still the publicly listed holdings held for decades, that is most meaningful for Latour.

Listed Holdings (64% of NAV)

Below, we break down the key figures for all the Listed Holdings. In the valuation section further down, we examine Latour’s share of these profits and how they have evolved over time — and the results were more surprising than we expected.