Investor AB - FY2025 Update

Underlying EBITA growth in a record year, Key Contributors and our thoughts on Valuation.

Investor AB had a total return of 12,9% in 2025, which impressively was the 15th consecutive year they beat their index, surpassing another record! We dive deeper than the surface numbers, which in our opinion, contain a lot of noise.

The way all the numbers below is calculated is by multiplying all individual subsidiaries fundamentals with Investor’s ownership share. We think the NAV discount popularly used to value Holding companies has its value, but think a better way to value a hold’co is to measure the underlying profitability of the group. If there’s a lot cyclicality in there, probably best to do 3- or 5-year averages.

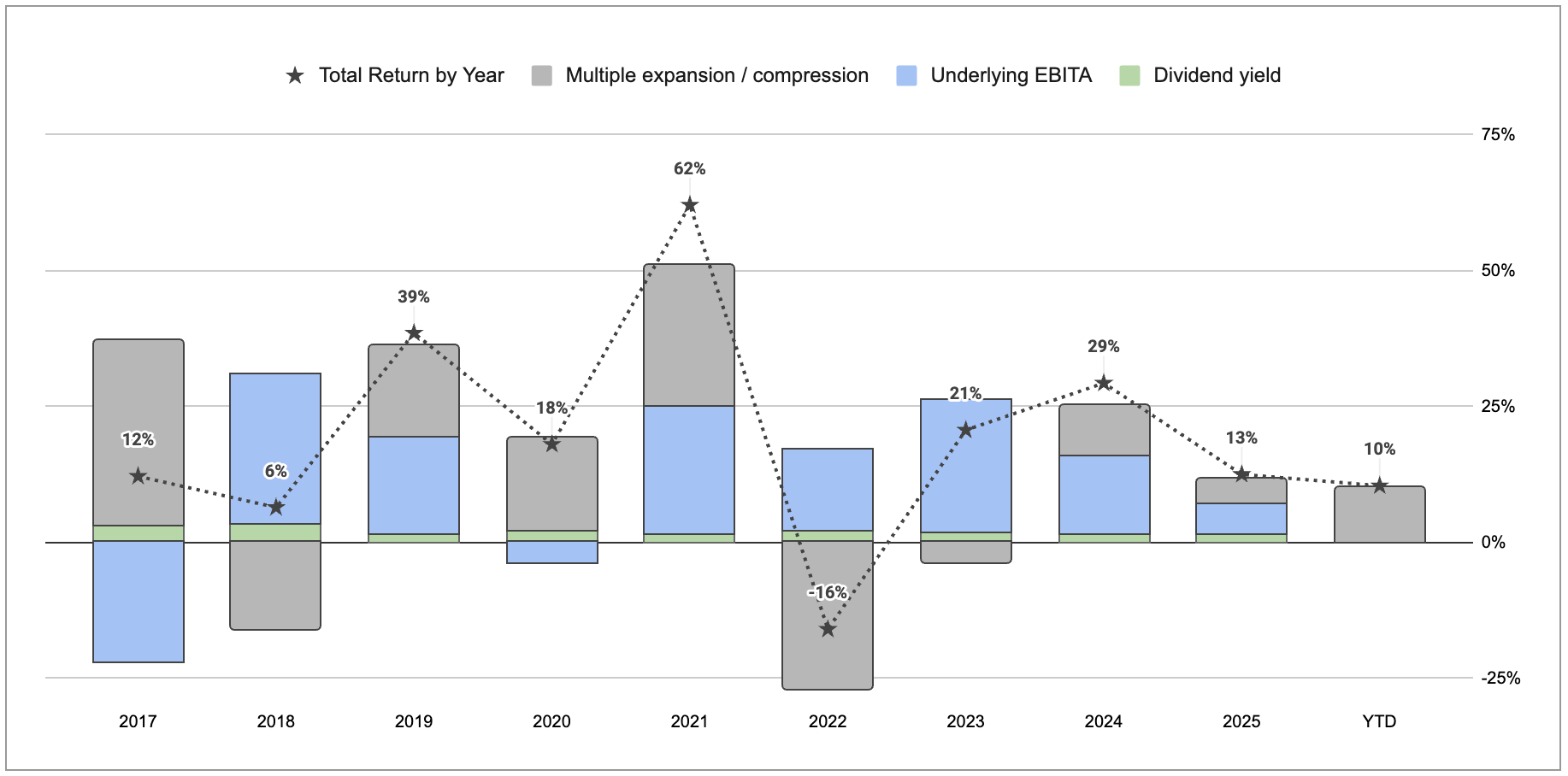

Exhibit I, show the drivers behind the 2025 returns, which comprised 2% dividend yield, 6% growth in underlying EBITA and another 4% multiple expansion.

With another 10% shareholder return since year-end 2025, the multiple expansion is about to expand 3 years in a row. The market efficiency theory would suggest fundamentals are to improve further, in an attempt for the stock to price in improving fundamentals. But when looking back historically, we wouldn’t say the market have had much success doing this in the past. If anything, the conglomerate may have been consistently undervalued, given Investor’s market-beating returns.

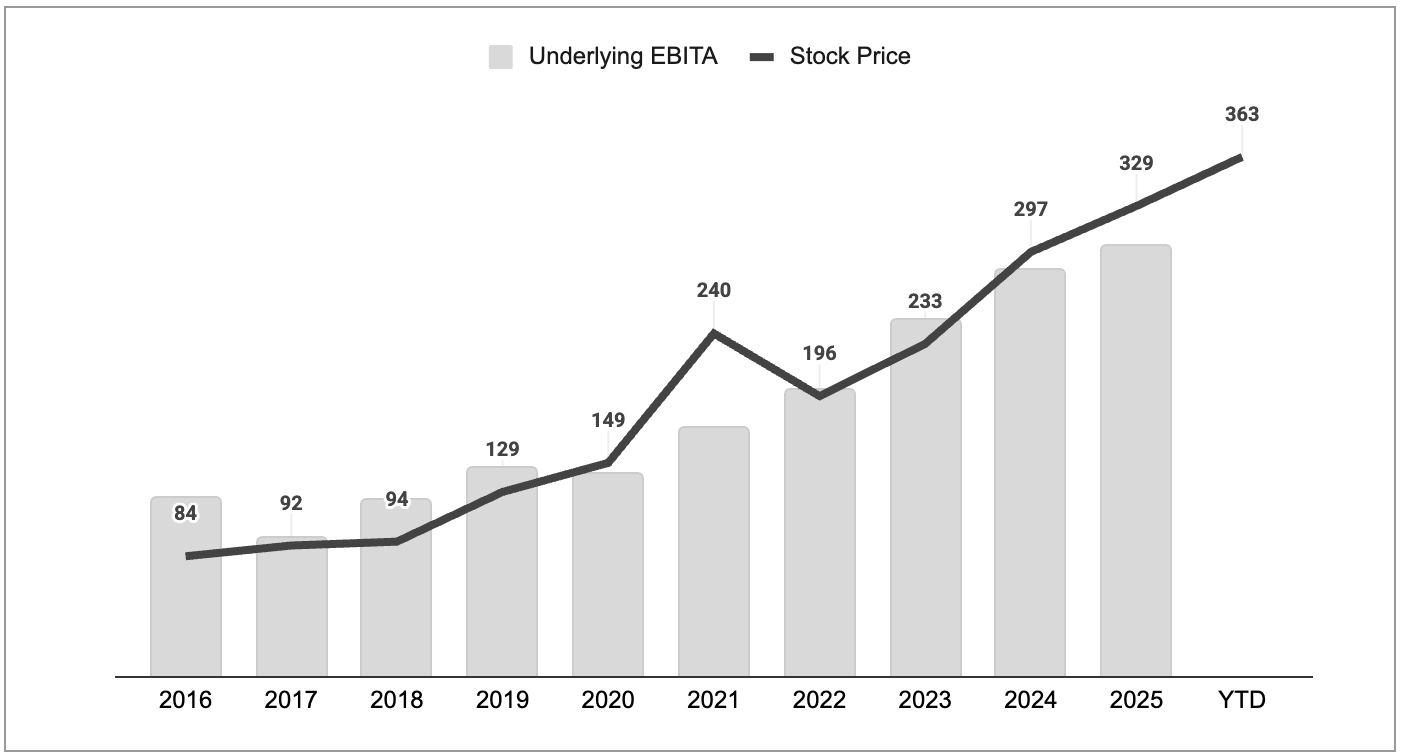

The key number we look at for Investor is the Underlying EBITA. We think this number should correlate well with shareholders returns over long time, as you can see in Exhibit II below.

The 6% growth in EBITA, was driven positively by Ericsson (3% contribution), ABB (2%), Saab (1%), Sobi (1%) and EQT (1%). Negative contributors were SEB (-2%) and Atlas Copco (-1%). Note that currency was a headwind for many in 2025 with weakening USD in particular (eg. AstraZeneca).

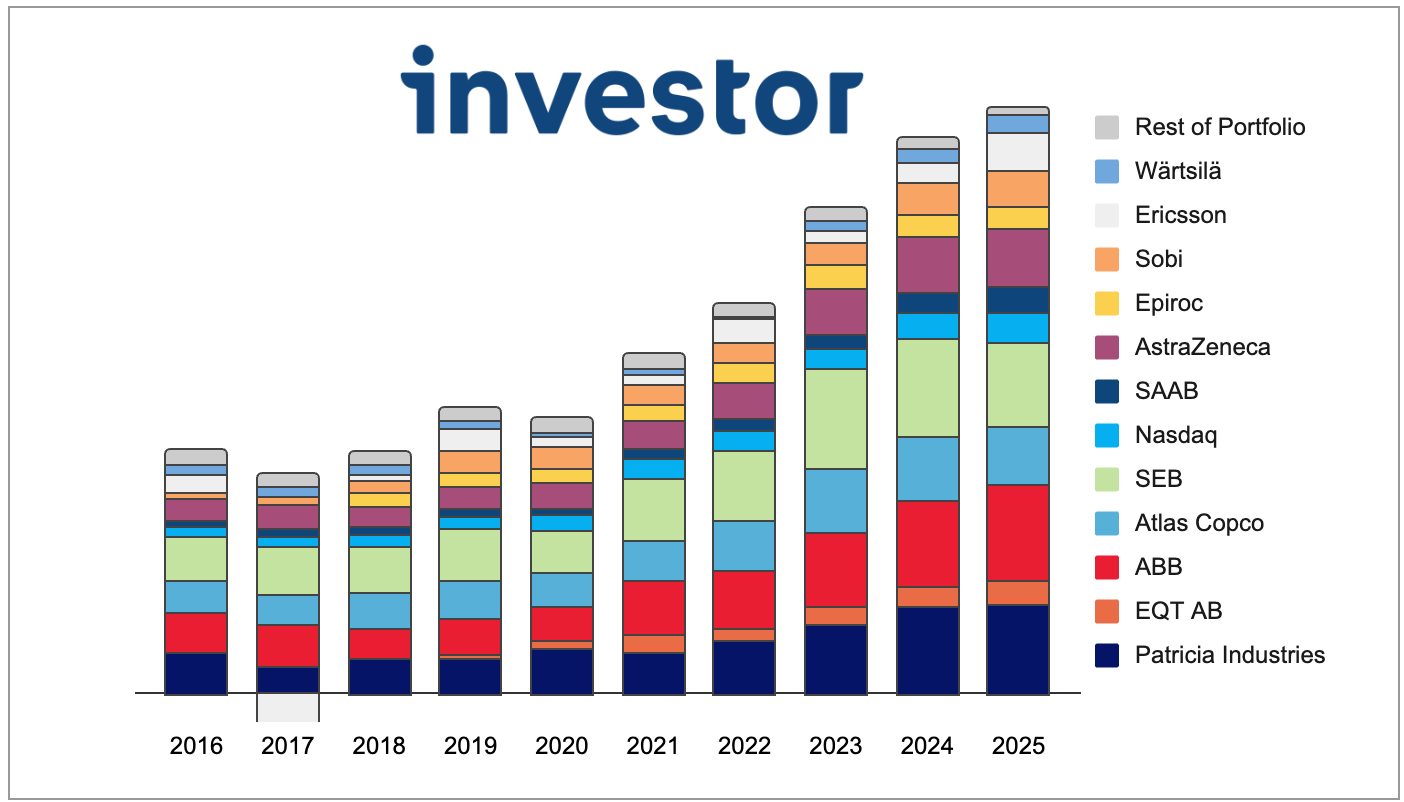

Exhibit III show the underlying EBITA by company over time.

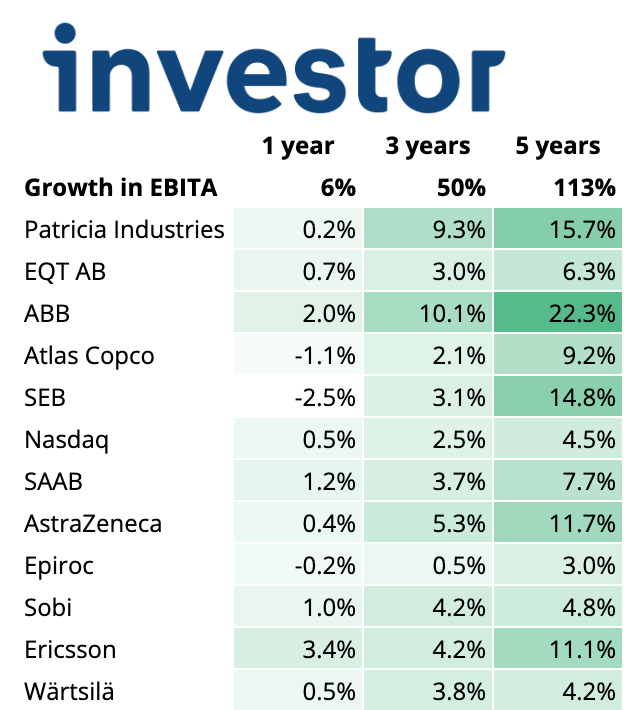

Exhibit IV show growth contribution by company for different time periods.

The table below highlights well why Investor does not deserve to trade at a large discount to Net Asset Value. Most of it’s companies are steady growers.

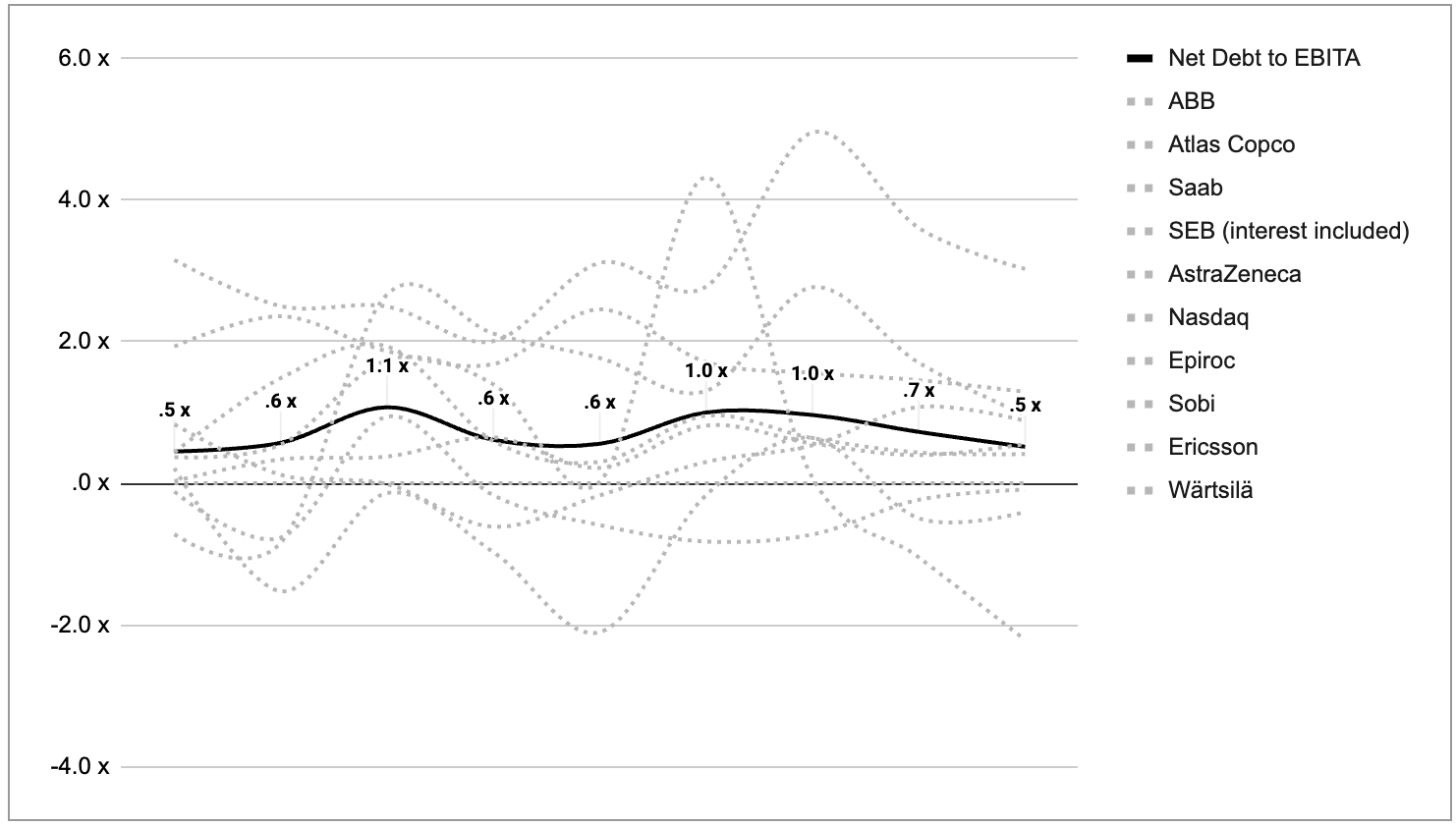

Leverage

Investor AB had 23 billion SEK of Net Debt in 2025. That’s at the lower end of their target range (0→10% NAV), which gives them a lot of optionality going forward. However, what is the leverage of their Listed subsidiaries?

Since we’ve used EBIT (earnings before interest and tax) before to value Investor, and valued this against the Enterprise Value of Investor (calculated using market cap - net debt - EQT funds).

The problem we realised with that calculation is it doesn’t include interest expense or the debt from subsidiaries is excluded. Thus, we have now included the subsidiary net debt in measuring the Enterprise Value of Investor AB.

In Exhibit V, you can see the leverage ratio for key Listed Subsidiaries of Investor.

Leverage went down in 2025 on average, only at 0,5x Net Debt to EBITA. If we multiply this weighted average figure with the Underlying EBITA, we arrive on 30,9 billion of underlying Net Debt. The last component of the Enterprise Value calculation we use to value Investor, is the 39 billion of EQT funds.

Valuation

This section is exclusive to paid subscribers.

The figure below is not available on most brokerage platforms, or even in Investor’s reported financial statements. It requires extensive work to calculate.We use EBITA, in line with elite serial acquirers, to better reflect the economics of businesses with acquisitive growth models — an approach particularly relevant given the acquisitive nature of many of Investor’s holdings. A subscribtion only costs $8 per month, or a $60 per year price.