Q1 26 Key Holdings Update

Cover: Topicus, Medistim, Shift4 and Harvia.

Disclaimer: This newsletter is provided for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities

Q1 2026 was an eventful quarter for our portfolio, with a lot of shareprice volatility. However, the underlying fundamentals continue to be much more stable.

But before we’ll go through the recent developments, we just want to say a big thank you to the 57 new paid members who’ve signed up in the last year and all the 3,500 Substack followers in total.

Our inbox is always open for feedback or to discuss investing-related topics.

We’ll go through the development last quarter for some key holdings. These writeups are exclusive for paid subscribers, but the update for Topicus will remain free.

Expectations: Topicus stock is down by 46% in the last year. Going into the report, a big overhang on the stock was Artificial Intelligence.

With improvements in AI reducing entry barriers to code, a new risk is that customers code their own software, reducing the need for a typical Topicus subsidiary. Thus, a key number to watch is organic revenue growth, as this number growing would contradict with that hypothesis over time.

Going into this report, we thought the AI risk was overblown for Topicus. Mostly, due to the fact that horizontal software has some unique properties, including deep knowledge within a vertical’s workflows, often low cost and the challenges of maintaining such systems individually. For mission-critical software, you don’t want to risk not being able to operate your business to save a few bucks in annual expense. However, we also acknowledge the speed of development is fast, and that some of Topicus’ many subsidiaries are probably in more risk than others.

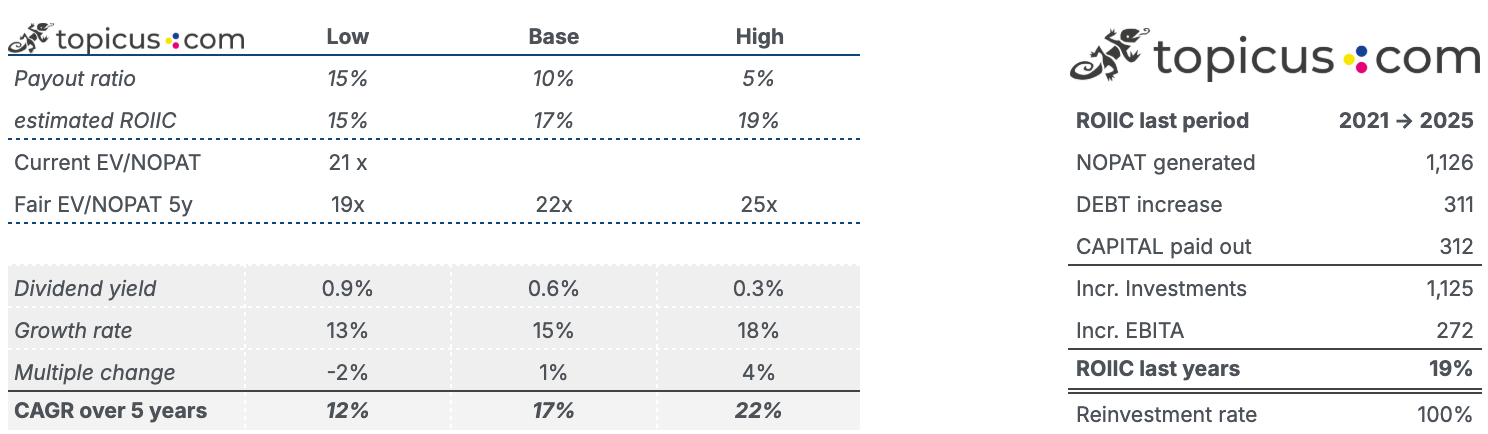

Another thing that helps Topicus, is simply their business model. At their reinvestment rate of the last 5 years (100% at 19% ROIIC), roughly half their revenues and profits would stem from new businesses within 5 years. This is a strength of Topicus’ (and big-brother Constellation Software) acquisition playbook — their high hurdle rate (low acquisition prices) is a protection against future disruption.

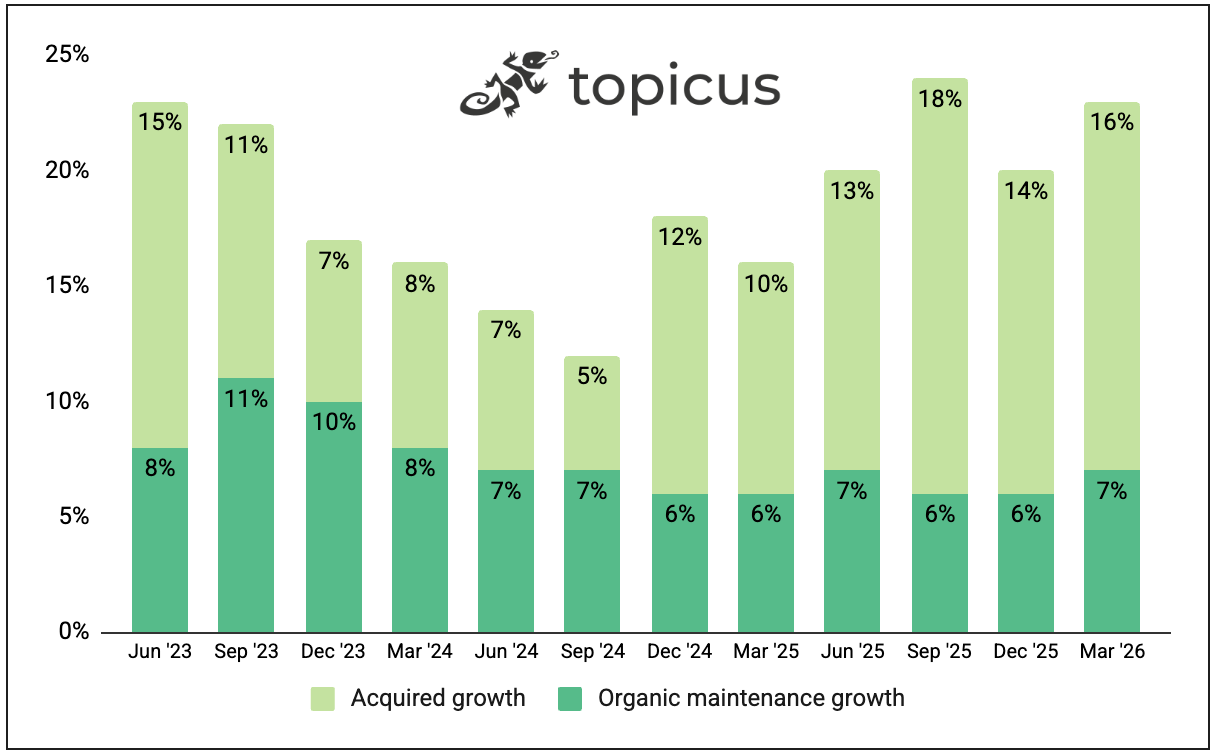

In Q1 2026, the key number to watch, maintenance organic growth, was up 7% (5% total organic). This means there are still no signs of AI disruption in the numbers yet.

Despite this, the stock went down after Q1. We think the likely answer are these two.

Acquisition spend was low this quarter, only €18 million (~15% reinvest. rate annualized).

Net Income down by 21% to €55 million (€70m).

We find both to be not meaningful, first one due to the fact that Topicus acquisition spend is lumpy, and they just had a record year of deployments in 2025. Second, the Net Income was not driven much by fundamentals, and rather some lumpiness in working capital changes, reporting of their Asseco Poland stake and higher interest payments, as they invested a lot of capital last year (and increased debt).

A third reason could be that it’s too early to tell whether the AI risk is real. This is understandable, as the multiple of Topicus stock has fallen from very high levels. At such prices (50-60x profits) you don’t have much headroom for things going wrong.

However, a day later (May 7th), Topicus stock went up 6%. Most likely from news of another acquisition in the US, of Keypoint Intelligence. Just a couple days later following the acquisition of Desyde in Netherlands. Acquisition timing can be lumpy, as they should be.

At $90 CAD per share, you can see the potential for different growth assumptions. We deducted the Asseco Poland stake from enterprise value.

Medistim

Medistim has spent more than four decades refining technologies that give surgeons real-time guidance in the operating room. This writeup aims to cover the runway for this Medical Equipment leader to…

Expectations: Since 2024, Medistim’s growth has surged from normalization of capital sales, increased market penetration, equipment upgrades and price increases. Their razor-blade-like business model delivers exceptional financial figures with 80% gross margins and 40% Return on invested Capital.

We believe the growth runway extends more than a decade out, driven by: