Top 10 Ideas - 3 Holding Companies

Going through 3 more of our top 10 ideas. Our thesis in Investor AB available for all readers.

Hi there,

This week, we’re following up last week’s Industrial start of our top 10 holdings. This time — the three Holding Companies within our portfolio.

The full PDF will be available exclusively to paid members, but the thesis on Investor AB is free for all — more on that one shortly.

Before we dive in, a quick personal note:

This autumn, I’ve decided to scale back my regular work commitments a bit. For the rest of the year, I’ll be taking Thursdays and some Fridays off to spend more time on what I truly enjoy: independent research, discussing ideas with like-minded investors, and sharing what I learn here with you.

It’s not a financially motivated decision, just a recognition of where I find the most energy and meaning right now. And honestly, the recent growth in both free and paid subscribers has been incredibly motivating. Thanks for reading, engaging, and being part of this little corner of the investment world.

And if you have been considering becoming a paid member, I believe the full 20-page long PDF which is delivered later this week will be something special, uncovering probably well over thousand hours of research over several years into top holdings.

Cheers,

Ole

Disclaimer: This newsletter is for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities. All investments involve risk, and past performance does not guarantee future results.

Holding Companies

Holding companies, whether serial acquirers or conglomerates, represent one of our favorite investment "ponds." However, over time we've identified several things we watch out for.

Limited Transparency in Private Holdings: If private assets form a significant NAV portion, and fundamentals aren't disclosed, investors rely solely on management's judgment to validate developments (e.g., Exor vs. Investor AB's detailed reporting of privately owned assets).

NAV is not Fair Value: NAV is influenced by market sentiment. We believe we should also consider the underlying profit behind the hold’co, like we would with any other business.

In a market downturn, like we for example are seeing in many healthcare names now (multiples falling), the price of assets are going down. One example of this is Patricia Industries within Investor AB. But, since profits are growing (see below), we believe the deal gets better, despite a declining Asset Value.

Thesis relies on Discount Narrowing: Deep discounts are appealing, but they often obscure true value drivers. If value realization pathways are unclear, it's just speculation on an uncertain "reversion to the mean." Operators (often family-owners) may lack incentives to unlock this perceived value for shareholders. Find operators who are aligned with minority shareholders.

Positive Indicators ("Green Flags"): Conversely, we consider the following as strong positive indicators:

Proven track record of shareholder value creation: One trait we have learn to appreciate is a business’ ability to shrink, in order to grow. Examples are share buybacks or spinoffs in opportunistic times.

Commitment to long-term ownership of business units: While divestitures has their time and place, we prefer owners who treat most business units as permanent holdings, fostering a more win-win relationship in our opinion.

Transparent financial reporting: Ideally we prefer when holding companies enable investors (or management) to translate complex financial data into a few critical metrics, like free cash flow available to shareholders, underlying profit, or discretionary free cash flow (all trying to describe the same thing - progress).

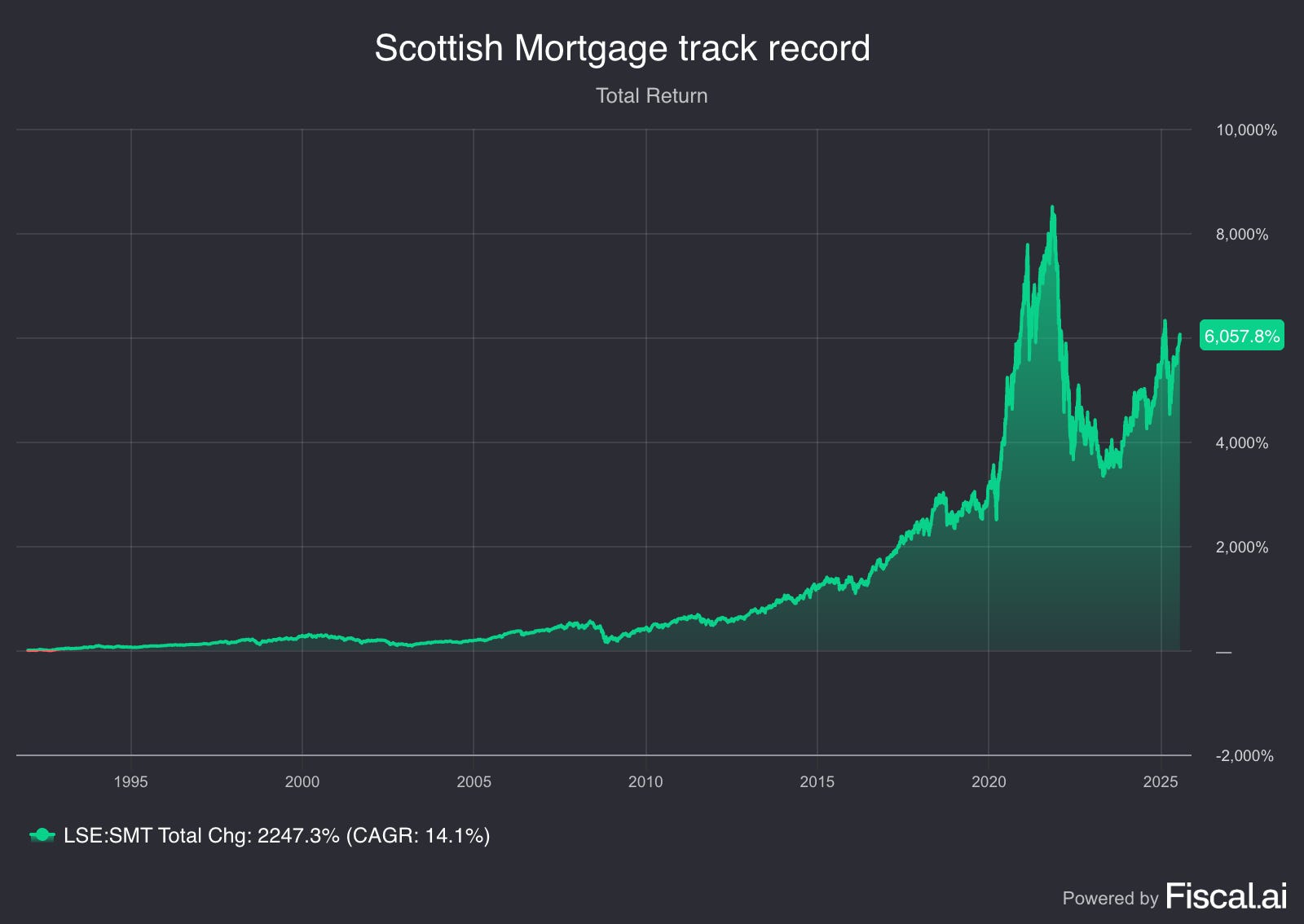

One who doesn’t check this for us is Scottish Mortgage Investment Trust, despite their excellent long-term track-record. For us to invest here, we would have to just sidecar with management’s track-record and believe their picks will do fine. The plus with this one in particular, is some very interesting exposure to some of the worlds most valuable private businesses, like SpaceX.

Let’s dive into the Thesis & developments in 2025 for our 3 picks in more details. On average, these 3 holding companies, has earned us a 44% return over our 1,6 years average holding period, which varies from one to three years. This is in what we believe are relatively low-risk businesses. For paid members, you can find full PDF below Investor writeup.

Cheers, Ole

TOP 10 IDEAS - Our 3 Holding Companies

🇸🇪 Investor AB

The Wallenberg family controls over 50% of the voting rights and 23% of the capital in Investor AB. We believe the way Investor is structured creates at least 4 enduring competitive advantages for its subsidiaries — both listed and wholly owned.

🏛 Access to Capital

Investor AB’s role as a long-term steward means it can support its companies through difficult times. Historically, they stepped in to save Atlas Copco during WWII. More recently, in 2025, they co-invested with EQT AB to take Fortnox private — a notable move, as CEO Cederholm mentioned this was the first time Investor structured a deal like this.

Note: Investor’s stake in Fortnox will be reported under investments in EQT.

🧠 Access to Talent

Investor’s dividends to their largest owners, the Wallenberg Foundations, fund research and education programs. Interestingly, most of these programs align well with Investor’s strategic focus areas — creating a strong pipeline of aligned, well-trained talent for its portfolio companies.

🤝 Access to Deals

The Fortnox deal with EQT underscores Investor’s growing toolkit for deploying capital. We believe they have an advantage in finding deals and being a preferred owner in such cases. A few channels they can deploy capital into include:

Organic and inorganic investments via Patricia Industries — such as Mölnlycke’s factory expansions or Atlas Antibodies’ $2.2B merger with Nova Biomedical

Increasing stakes in listed companies (e.g. recent Atlas Copco purchases)

Investing in EQT funds

Co-investing with EQT in selected deals (e.g. Fortnox)

🌲 Long-Term Mindset

Perhaps most importantly, Investor AB thinks in decades, not quarters. This patient capital approach means their companies are willing to sacrifice short-term pain for long-term gain — positioning their companies in resilient, growing sectors.

Some notable examples we believe most companies wouldn’t do, include:

SAAB exited automotive to focus solely on defence

Atlas Copco pivoted to industrial niches, away from diesel engines

Electrolux spun off its higher-margin Professional segment

ABB divested low-margin units like its power grid business to Hitachi

AstraZeneca refocused from broad pharma to targeted specialty medicine

Showcasing the ability to shrink in order to grow exceptionally well.

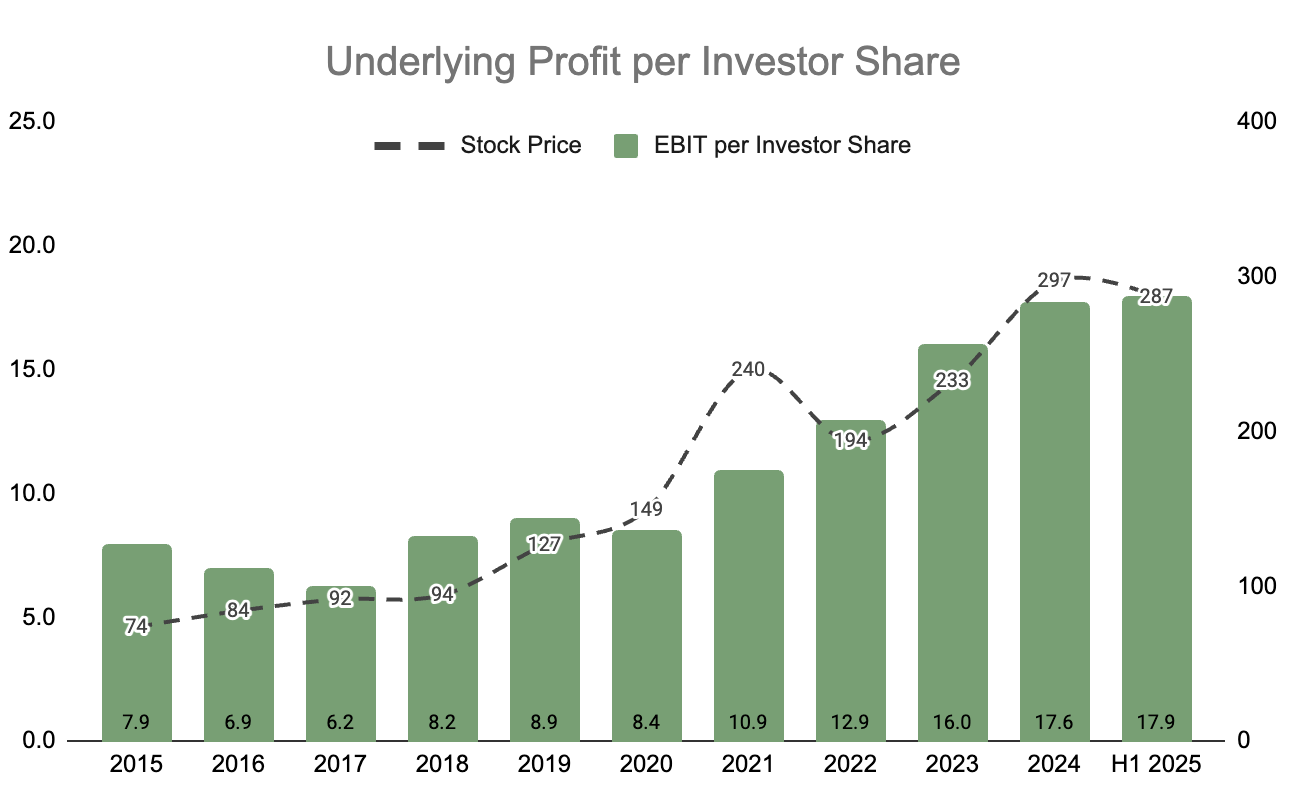

Performance

Over time, the Underlying Profit growth has been followed by a similar, though slightly higher growth in share price. We believe the key thing to focus on is the collective growth in those green columns (EBIT).

Investor – Fundamentals 2025

Importantly, Investor’s leverage ratio is in its lower range of 0-10% of NAV. What does that mean? Optionality. Over the next decade, we believe Investor is likely to have more (relative) capital able to reinvest than in the last decade, both from taking on some more leverage in times of opportunity, but also from the growing cashflows from wholly-owned subsidiary Patricia Industries (which was the main rationale for setting up Patricia in the first place).

Typically, Investor distribute the dividends from Listed Companies directly back to shareholders (including the Wallenberg foundation), and reinvest capital from Patricia / EQT. However, like we have repeated before, reinvestments within the Listed Companies, not touching Investor’s financial statements, are crucial as well.

Over the next decade, we believe we will see:

Market-beating returns from Investor’s Listed Portfolio, due to its high quality, prudent capital allocation discipline, and positioned well in sectors with durable tailwinds (most also with competitive advantages & EBIT margins ~20%).

Double-digit growth in profits from both Patricia & EQT AB - driven by mid- to high-single digit organic growth + some inorganic growth as well.

2% dividend yield to us owners. We believe dividends from the Listed Portfolio will continue flowing straight to us owners, and slightly grow over time.

Investor own reinvesment. Finally, even if Patricia and EQT cashflows are fully recycled back into themselves, we believe there will be additional capital able to invest, from upping their leverage ratio. Especially in times of opportunity (fear).

Combined, this gives potential for a compounding rate of 10-12%. We have trailing EV / EBIT of 16x today (~21x PE), which sounds attractive for such a high quality diversified asset, given what we know today.

Discount to NAV

Investor AB currently trades at a 10% discount to NAV. While this is the official figure, we think it understates the opportunity.

Investor applies this discount entirely to Patricia Industries in its reporting. But we believe that’s the wrong place to apply it. Patricia — effectively a high-quality serial acquirer — deserves no discount, in our view. If anything, the listed portfolio should be discounted slightly, since we could theoretically handpick those ourselves.

But more importantly, we believe the real opportunity lies beneath the surface of reported NAV, helped by a selloff inn the listed peers of Patricia Industries (healthcare), probably related to tariff worries.

More specifically, we have heard “earnings growth was more than offset by multiple contraction” several times. In practise, NAV continues to decline, even though the underlying fundamentals are growing.

We love setups like this: Where valuation compression masks operating performance. It creates a mismatch that contrarian investors can take advantage of.

And one more thing, while it’s hard to precisely quantify the value of a capital allocation track-record, we think getting the Holding Company’s advantages touched upon earlier for free, is nothing short of excellent.

We believe Investor AB can compound at low double-digit rates from here including dividends (290 SEK). Investor is also the only company we could sleep well having 100% of our assets in. We would however not expect the decade-long 20%-return to continue, due to a unique mix of both growth, multiple & margin expansion + currency tailwinds (weakening SEK). Perhaps less upside than many of our other picks, but we believe Investor AB has also much less downside risk - warranting it to continue being our largest position.

We would think about parting ways with Investor, if either of these happen:

Capital Allocation we can’t get our heads around (like overpaying for bad assets)

Even higher dividend payout ratio (reinvestments is key for sustained high growth)

EV / EBIT over 25x (16x today), especially if we find better alternatives elsewhere). We may trim if price goes above 20x EV / consolidated EBIT.