5 Quality Companies at a <1 PEG

5 under the radar quality companies trading at profit multiple's less than their growth expectations for this year

Disclaimer: This newsletter is provided for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities. The author may hold shares in the equities discussed.

PEG ratio

Peter Lynch popularized the term price/earnings-to-growth, or PEG. The logic is simple: investors are willing to pay a premium for more growth.

The PEG ratio is typically calculated one of two ways:

Forward PEG — one-year forward earnings growth estimates, priced against today’s earnings

Trailing PEG — last-twelve-months earnings growth, priced against those same earnings

We prefer stable businesses, those relatively easy to predict this and next year. A PEG ratio for a cyclical like Equinor, seeing 90% growth in 2021 for instance, would not make much sense to put into a PEG ratio exercise. Thus, other tools works better for cyclicals. Given that the ideas below are all stable, predictable businesses, we price them against 2026 earnings estimates and the growth compared to 2025.

You’ll also notice we use an EV/NOPAT multiple alongside PEG. It’s conceptually similar to price/earnings, but instead of net income, it uses operating profit (NOPAT). That strips out noise from things outside the company’s control — interest rate swings, one-off tax items — leaving a cleaner read on the growth of the underlying operating business.

EV / NOPAT = Enterprise Value (Market Cap + Net Debt) / (EBIT + amortization of acq. int. - tax normalized)

The first company out is a firm we’ve owned for more than 3 years, and is a market leader within it’s niche, and has the unique combination of earning excellent returns on historical investments and still reinvest a healthy portion of profits every year.

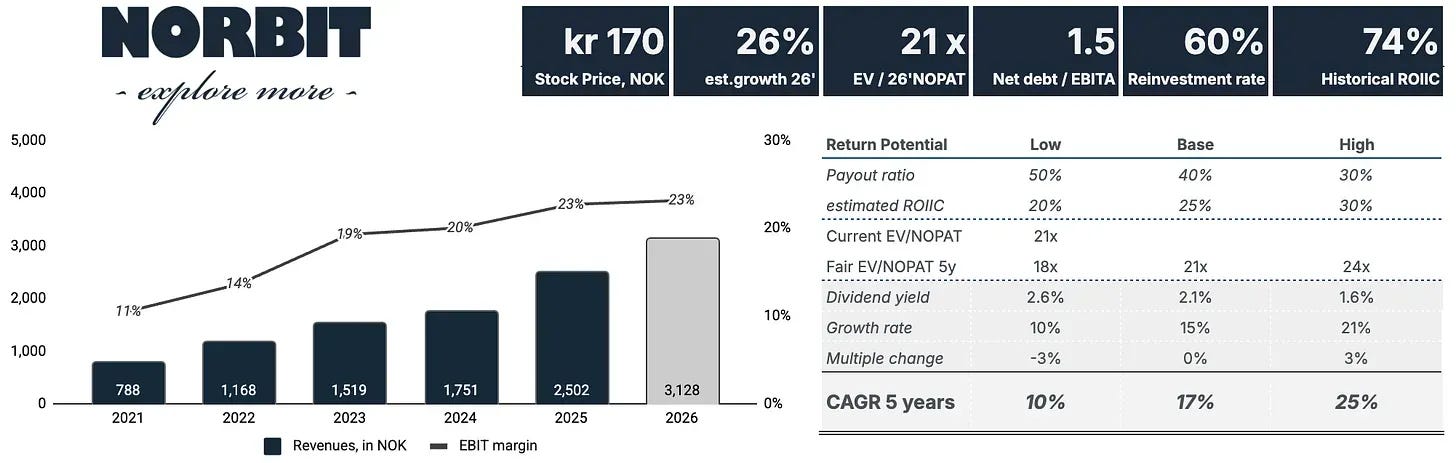

NORBIT — 26% growth vs 21x price

The graph above clearly show the strong years NORBIT have behind them. Growth has been supported by several tailwinds, with increased defence spending receiving the most attention recently. This has transformed NORBIT’s Product Innovation & Realization (PIR) segment from a relatively low-margin contract manufacturing business into a faster-growing and more profitable operation, as defence customers increasingly prioritize local electronics manufacturing and higher-value products.

A closer look at NORBIT's two best segments — Oceans and Connectivity — shows that the company is also solving increasingly complex challenges through its own proprietary products. Whether supplying sonar technology underwater to support security during the Paris Olympics or enabling Toll4Europe's interoperable tolling solution, which allows truck drivers to use a single on-board unit across multiple European toll domains. Across both segments, the common denominator is that NORBIT delivers mission-critical technology in niche verticals.

And if you ever wonder what’s the competetive advantages are for Norbit to earn such high returns on capital, the word niche is key here. We remember Per Jørgen calling this out some years ago, when he mentioned that a company like Huawei would not be interested in the small niches Norbit operates in.

The irony, is that the same argument could also be a bear case longer term.

Consider a surveying vessel previously having a couple of Norbit camera’s and tens of employees, now being able to replace this with twenty unmanned drones being remotely controlled by the employees by land. Such an automation upgrade, would not only lower the cost and likely increase the amount of missions (jevsens paradox), but also result in a massive demand for such sensors. And if the end-markets Norbit operates in grows enough, they may ultimately catch the interest of larger players — thus increasing competition.On the other hand, reality today still show a company delivering exceptional topline growth and expanding margins. And perhaps just as importantly, Norbit allocating capital to expand into more of these niches. They just completed the acquisition of WaterLinked, another company with 20%+ margins and similar topline growth as Norbit. This follows the acquisition of Innomar in 2024, which also expanded the problems Norbit could solve, and importantly for investors, generated an attractive return on incremental capital invested.

Given this, we think Norbit again trades below Intrinsic Value (given what we know today). It trades at a roughly 21x multiple, while being expected to grow more than this in 2026. Resulting in a PEG ratio less than 1. You can see the financial KPI’s we track for Norbit below, in measuring the EV / NOPAT, and measuring returns on capital.

The second company out is one we recently covered in a detailed writeup.

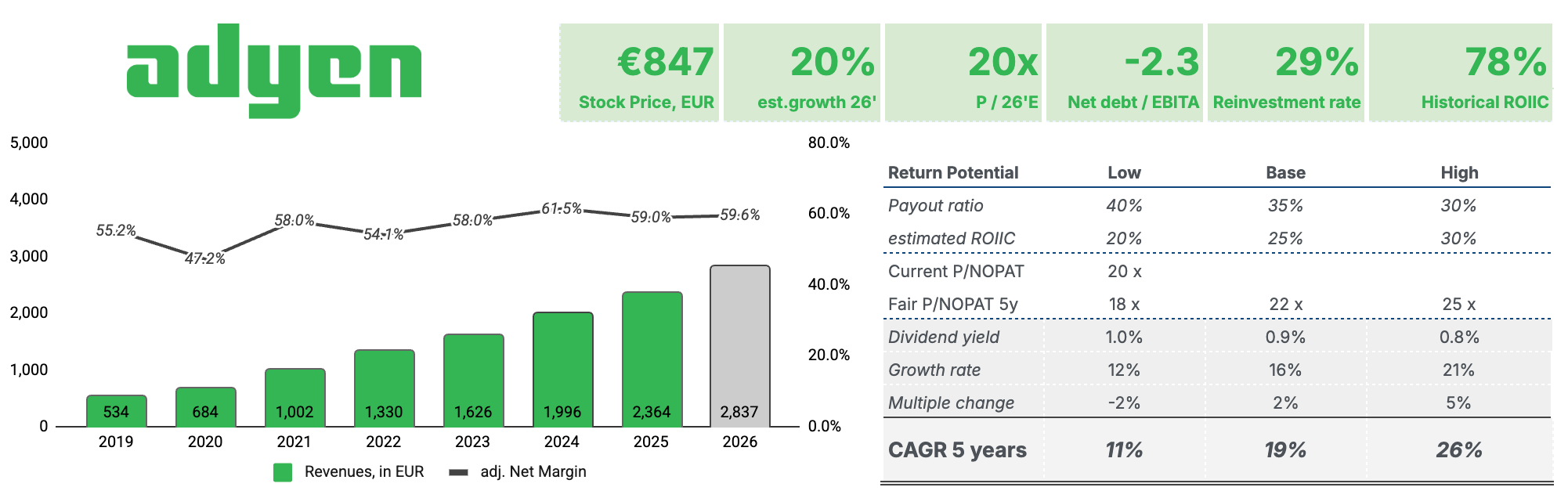

Adyen

We just covered Adyen in our recent writeup.

After years of being valued as one of Europe’s most expensive growth companies, the Dutch payment giant has derated significantly as investors became concerned about slower growth and increasing competition.

However, the underlying business remains highly attractive: Adyen continues to grow around 20% per year, maintains industry-leading margins and benefits from strong customer relationships with some of the world’s largest merchants.

The market appears to underestimate the durability of Adyen’s competitive advantage. While many investors view payments as a commodity, Adyen’s value comes from its global infrastructure, higher authorization rates and ability to simplify complex payment operations for large enterprises.

At today’s valuation, investors are paying a much more reasonable price for a business with software-like economics, strong returns on capital and a long runway for growth. If Adyen continues compounding earnings while maintaining its margins, the current multiple leaves room for attractive long-term returns.

The next company, is a family-owned company with 20% operating margins, similar high returns on capital, net cash, structural growth tailwinds and a 9x profit multiple!

To us, it seems like the market is mistaking this niche market leader for competing in the wider more commoditized market of it’s larger peers. With a 9x profit multiple, we ask ourselves — Is the market really extrapolating that last year’s margin contraction from a one-off cost item and investment in opening new locations will continue forever?

This, and the next 2 companies is reserved for paid subscribers.

If you consider becoming a paid subscriber, the cost is €75 per year or €12 per month. Subscribers receive a monthly letter covering lessons learned, portfolio changes, and exclusive updates on existing holdings.

The content is not AI-generated, nor will it ever be. I genuinely enjoy doing my own research, and one of the most rewarding parts is sharing our ideas while also receiving ideas from you readers.