Inside the Corner - June 2026

Lesson from Buffett applied to Adyen's stock. Norbit M&A. Insider purchases. Shift4 Rating update. Investor expensive (?) and a mispriced holding for the Wallenberg's?

Disclaimer: This newsletter is provided for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities. The author did purchase shares after writing this.

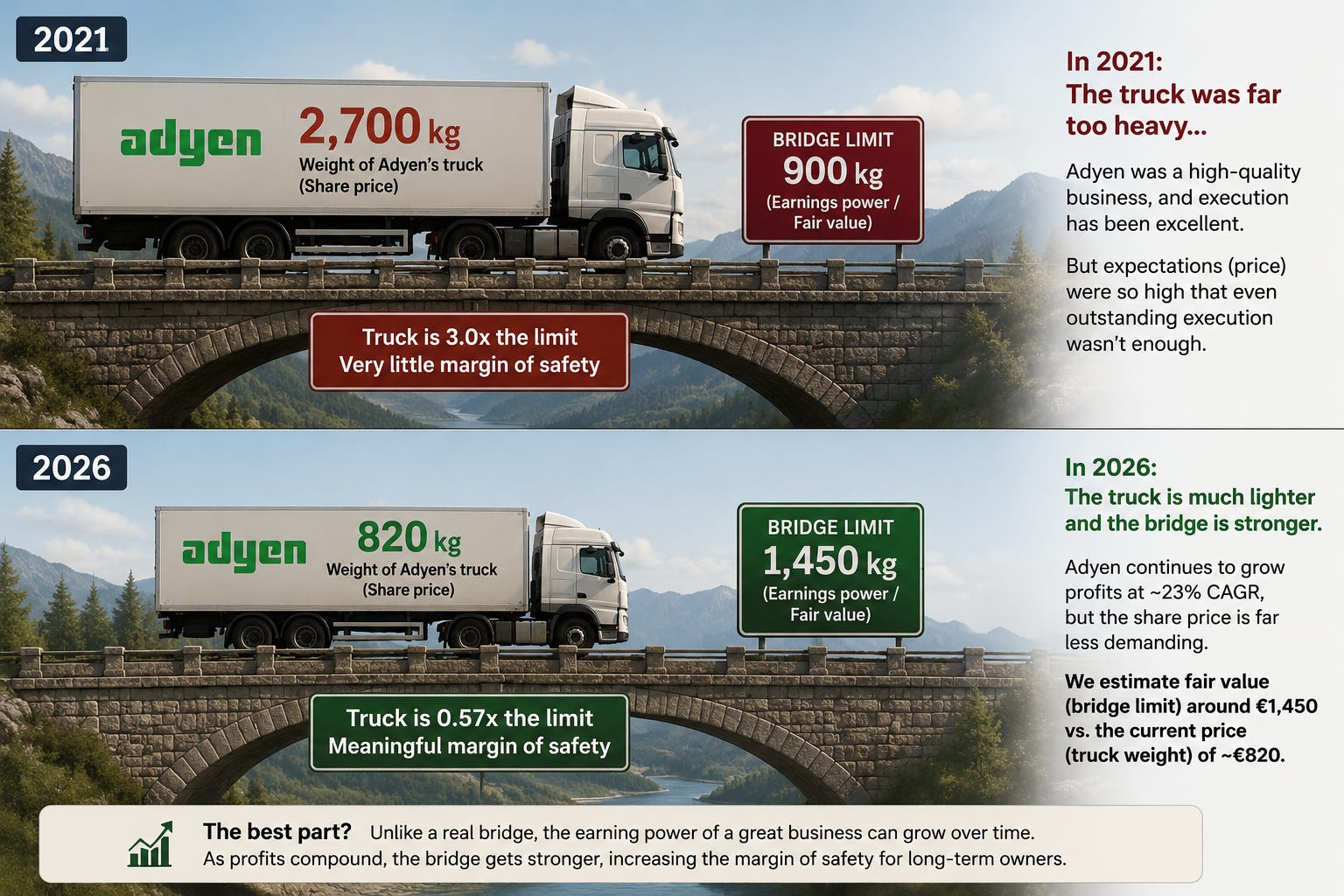

“A famous lesson about a margin of safety, is that you don’t drive a truck that weighs 9,900 pounds across a bridge that says limit 10,000 pounds, because you can’t be that sure about it” — Warren Buffett

We recently completed our write-up of Adyen, and Buffett’s analogy captures an important investing lesson relevant to quality investors: buying a great business isn’t always enough — you also need a sufficient margin of safety.

Think of the bridge as Adyen’s future earnings power, and the truck as the expectations embedded in its share price. In 2021, the truck was simply too heavy at a €2,700 price. Investors were relying on perfect execution to generate attractive returns. The still impressive 23% profit CAGR Adyen delivered was not enough.

Fast forward to today, and the business continues to grow at a similar pace. The difference is that the truck has become much lighter. At around €820 per share, we estimate Adyen’s intrinsic value to be closer to €1,450 (the limit of the bridge), providing what we believe is a meaningful margin of safety.

And the best part — we still see the fair value increasing — a margin of safety in itself, and the advantage of buying quality (the value can improve over time).

One important note is that the limit of the bridge is in the eye of the individual investor, and is a number that should fluctuate as the business develops positively or negatively. For those disliking Adyen’s recent acquisitions for instance, they may see the limit of the bridge decreasing. For those worried AI enables merchants like Netflix to do payments in-house, they may see a bridge far less supportive, and would perhaps even want an even larger margin of safety than the current ~40% we see.

That’s the fun part of investing, we can come to our own conclusion on what something is worth, and the answer will gradually unfold to us in the future.

Valuation

You may wonder how we got to that €1,450 number — we’ll share this and the usual Portfolio Update comes shortly after.

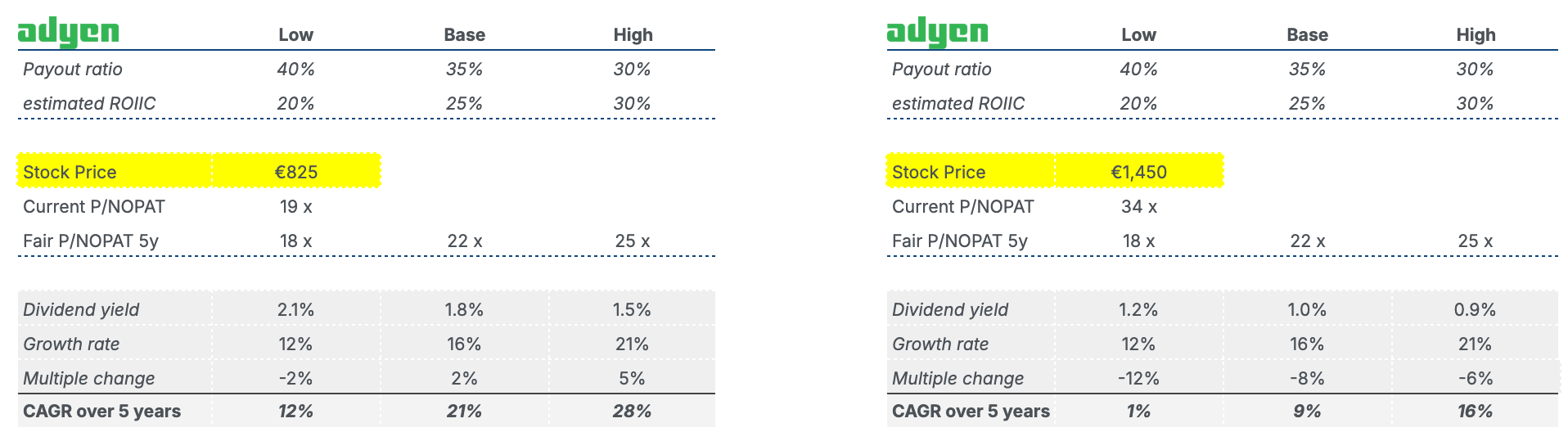

Below, you can see to the left: Today’s shareprice and our potential return scenario’s. And to the right: forward returns from a price of €1,450, around 9% CAGR on average.

Any investor will have different inputs to such a valuation framework. Some may wonder why we include a dividend yield here. That’s just Free cashflow accruing to shareholders — either as dividends, share buybacks or on the balance sheet. We only invest in management teams we think will allocate that capital well. And the recent acquisitions from Adyen made us lower the payout ratio (thus also higher reinvestments) and lower ROIIC (inorganic reinvestments typically yield lower ROI).

And if you wonder how we landed on around €1,450 as the fair value, it’s just where our base case delivered 9% CAGR (right picture) — a reasonable expected return given that most investors can generate 4-5% risk-free, and any attempt at investing in something else than that should yield a material upside given the higher risk.

For this month’s portfolio update, we’ll take a look at the portfolio as a whole, and also cover some key happenings — including acquisitions, insider buying, quality on sale (?) and (unfortunately) governance issues for a holding on our bench.