Investor - NAV discount gone

22% YTD return. Breaking down forward CAGR scenarios, the case for more debt, and a look at Capital Allocation.

Disclaimer: This newsletter is provided for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities. The author may hold shares in the equities discussed.

Investor AB shareholders have been well rewarded again in 2026, with the stock up 22% YTD. We will take a look at potential scenario’s for what future returns could look like. We’ve owned and covered Investor’s development closely for many years, we’ll leave some of our writeups here: Jan 24, Oct 24, Feb 25, July 25, Nov 25, Feb 26

Stock vs Fundamentals

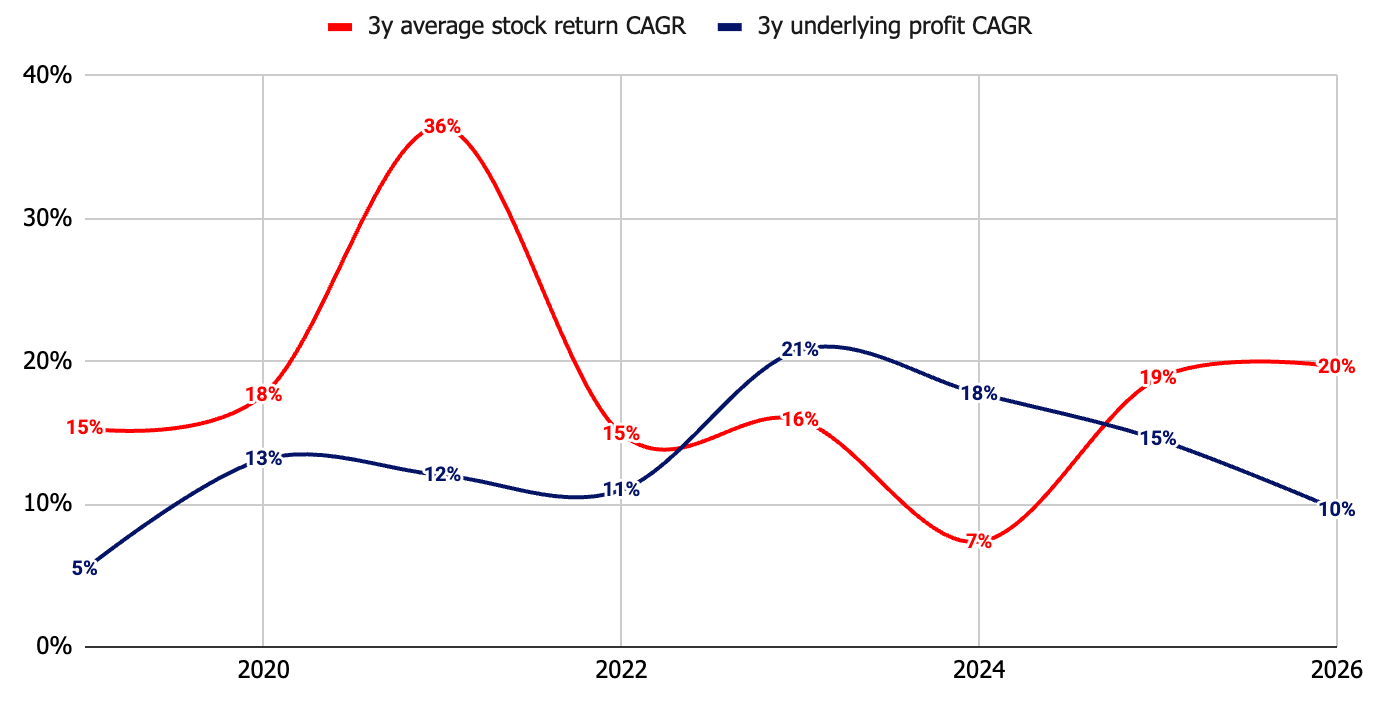

If we compare Investor’s stock returns compared to the fundamentals, shown in red vs blue line below, we can start to see that Investor’s stock price is running ahead of it’s fundamentals. Something it also did from 2019 to 2021 in particular.

While most focus on this valuation gap, it’s hard not to overstate how impressive Investor’s underlying profit growth have been (blue line). That is the key reason for Investor’s outperformance.

If we add the roughly 2% dividend yield per year, we can quickly see that the 15% compounding rate does not match the stock’s 21% CAGR for the last decade. This is explained by multiple expansion — the market being willing to paying more today.

The key question we wanted to dissect here is therefore, is Investor now priced for subpar returns going forward or will (arguably) Europe’s best holding company continue outperforming?

Valuation expanding

It’s important to note that there’s nothing particularly dramatic about Investor’s Valuation getting higher. If Investor continues compounding earnings at more than 10% annually and the valuation multiple gradually normalizes again, the stock may simply need a year or two for fundamentals to catch up with the share price.

That’s perfectly normal — even for exceptional businesses. Great stocks do not move up to the right forever, and share prices often fluctuate far more than the underlying business performance. Investor shareholders experienced this in both 2017 and 2021, when the stock delivered essentially no returns for roughly two years despite the company continuing to grow its intrinsic value.

The challenge, of course, is that valuation changes are almost impossible to time. Many investors have hurt their long-term returns by selling their highest-quality holdings simply because they appeared expensive. A good example was 2023, when many sold Investor after its NAV discount narrowed to its lowest level in more than a decade. What they overlooked was the rapidly growing earnings power of Investor’s largest holdings, which went on to drive exceptional share price performance over the following years. As it turned out, the NAV discount also continued to narrow from 2023 until today, allowing patient shareholders to benefit from two powerful return drivers simultaneously: rising intrinsic value and multiple expansion.

Given that the probability of continued multiple expansion from today’s historically expensive levels, we view it unlikely that this multiple expansion tailwind will persist. However, that does not necessarily mean Investor is a bad investment.

It simply means we don’t think it’s possible seeing the 20% CAGR again from here, as there is just one driver of positive returns — fundamentals.

Forward CAGR scenario’s from today’s price

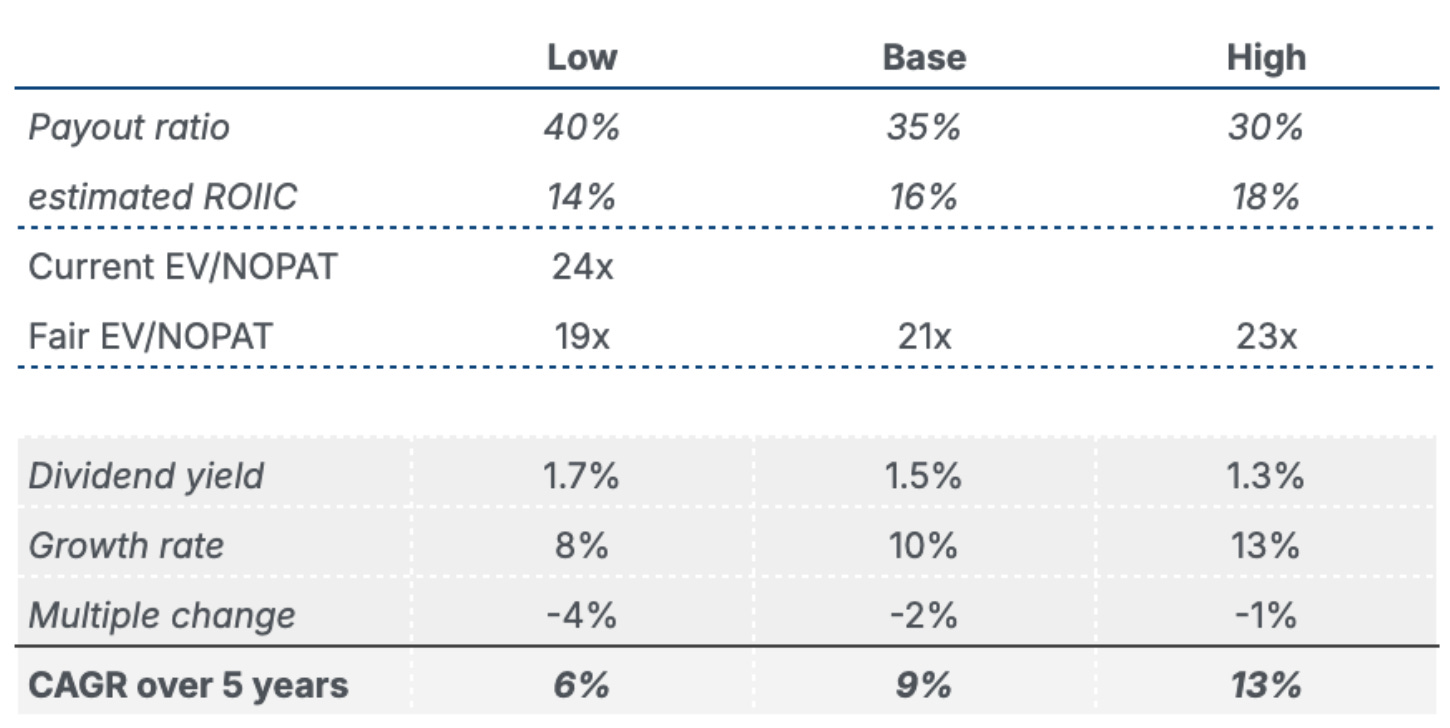

As of July 8 2026, the price of an Investor A share is 392 SEK per share. The adjusted EPS if you like is closer to 16,5 SEK — implying a profit multiple of 24x today. You won’t find these figures in your stock brokerage, as it’s a complex calculation.

Below, you can see our implied return potential for Investor stock today.

In our Base Case, we assume that Investor’s portfolio companies, on average, reinvest 65% of earnings while distributing 35% as dividends. Over the past seven years, the split has averaged roughly 70% reinvestment and 30% dividends, so our assumptions imply a modest shift toward higher shareholder distributions.

We further assume that these incremental investments earn an average 16% return on capital, below the 19% average achieved over the past seven years. This reflects our view that the portfolio is unlikely to benefit from the same degree of margin expansion that supported returns during the recent period. But it also reflects our opinion that management of both Investor itself and their underlying businesses will continue allocating capital well.

Finally, we assume today’s 24x EV/NOPAT multiple is modestly above a sustainable long-term level. Our Base Case therefore assumes the multiple gradually compresses to 21x, creating an annual valuation headwind of approximately 2% for 5 years.

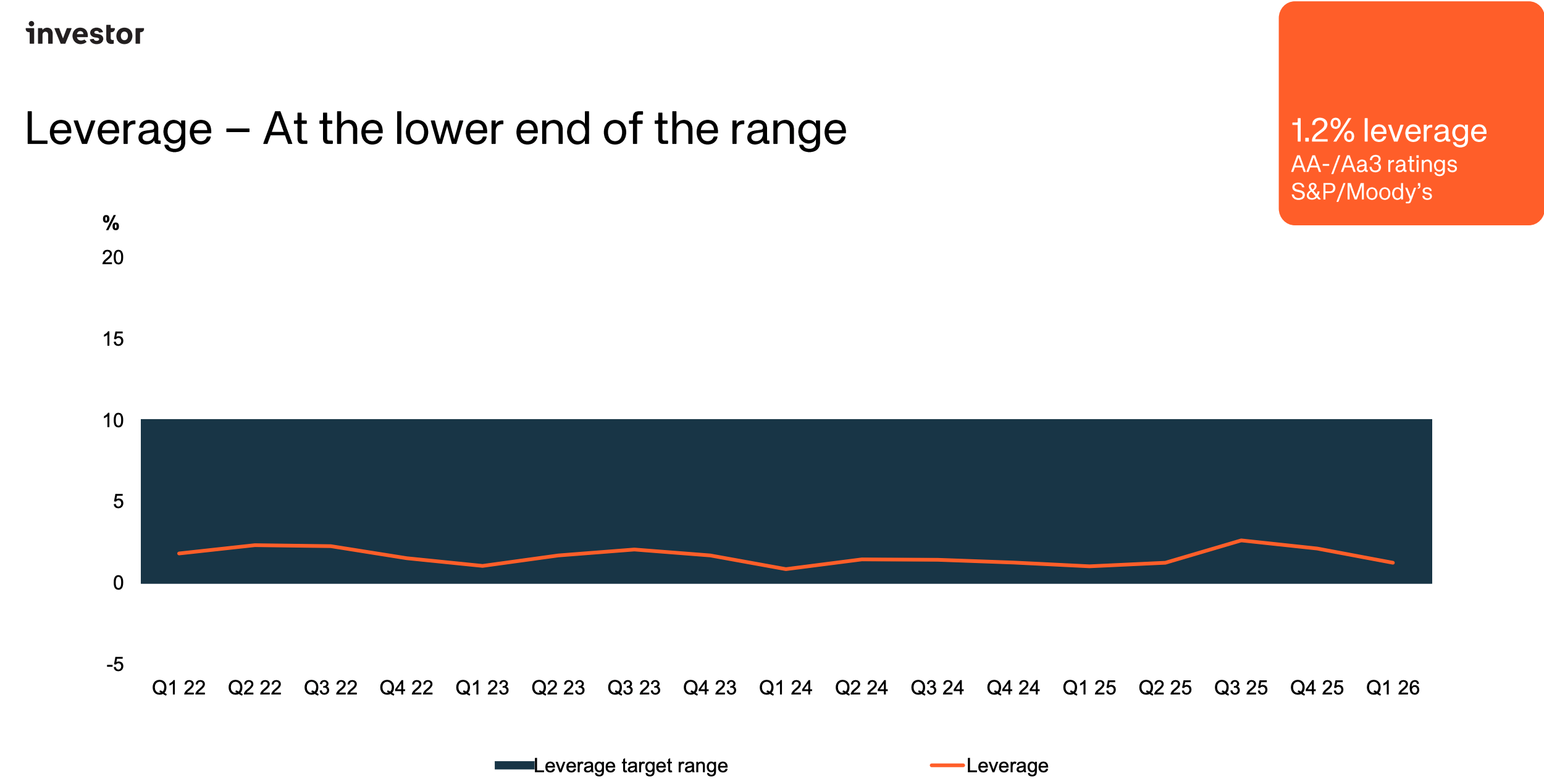

The Joker — Debt

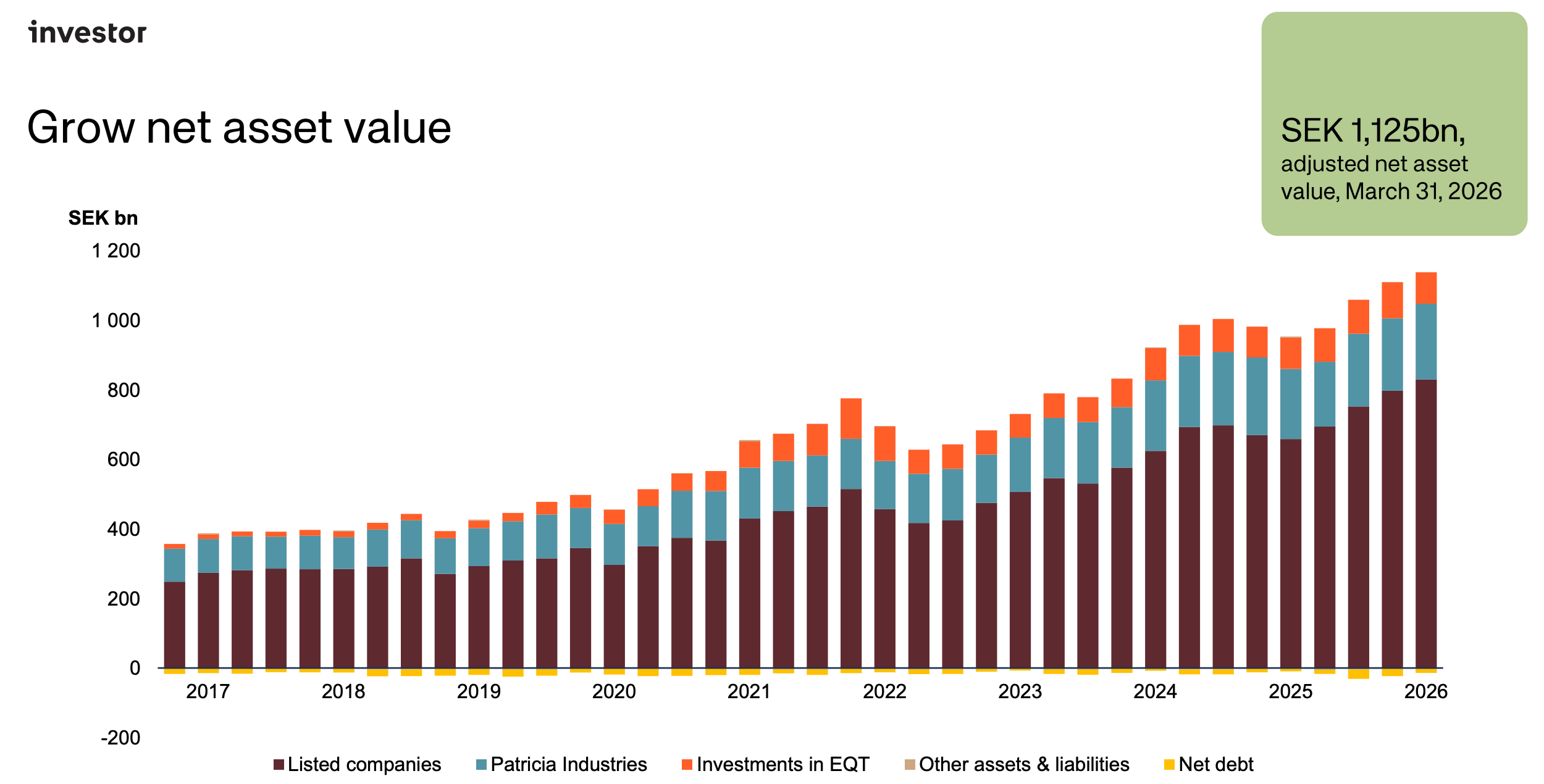

Investor’s historic NAV growth is truly impressive, but a figure that stands out in the table below is how small the net debt (yellow bars) is relative to their assets value.

We think of Investor’s low Net Debt to NAV (1,2%) as extremely conservative. Given that Investor is primarily an investment vehicle, they can always sell assets if they have liquidity issues. They also have their own cashflow within Patricia, dividends from listed portfolio and fluctuating cashflows from EQT.

Given this, we think Investor could tolerate a higher net debt ratio than most companies. And especially when you see their investment returns. For the last 7 years, we’ve measured the underlying ROIIC to be roughly 19%. That’s quite a jump from the 3,8% they paid in interest expense on their debt last year.

Consequently, we think Investor taking on more debt when seeing opportunity would be clever. During our time following the company, we don’t see Investor as a turnaround investor. Instead, they look for high quality durable assets, exemplified by them purchasing Piab Group for 20x EV / EBITA in 2018 from EQT.

We’d hope Investor would be more aggressive in the future, especially in times of volatility. We were a bit dissapointed not seeing Investor reinvest more capital during 2022, as that year presented many great buying opportunities for quality companies in our opinion — like those in Investor’s portfolio.

Holding Company Compensation

Considering that Investor consistently reports and discusses NAV as its primary measure of intrinsic value, one might expect management’s compensation to be tied directly to NAV growth. Interestingly, it is not.

Instead, long-term incentives are primarily linked to Total Shareholder Return.

We think this is an elegant design for Investor and Holding Companies in general. Rather than rewarding management for simply growing the asset base or maximizing reported NAV, it aligns them with the experience of shareholders. The objective becomes creating a portfolio that the market values highly and that delivers attractive long-term returns — not building a larger investment empire for its own sake. This also explain why Investor and it’s subsidiaries are so active in spinning off businesses.

Over the long run, succesfull reinvestments would either way result in a growing NAV per share, but by having an attractive portfolio, shareholder returns should follow that number closely. By linking incentives to TSR instead of NAV, Investor encourages management to focus on what ultimately matters: creating lasting value for shareholders, not merely increasing the reported value of the underlying assets.

NAV premium or discount?

Most holding companies trade at a large discount to their Net Asset Value (like Exor). Investor is almost priced at a premium, with just a 1% discount. A reflection of investors’ confidence in management’s ability to allocate capital and compound value over time. Investors are willing to pay the same as the underlying portfolio is “worth”, because they trust Investor to create additional value through future capital allocation.

That premium, however, is far from guaranteed. If major holdings such as ABB, EQT, or Atlas Copco were to decline materially, Investor’s NAV would fall alongside them. Most of the time, you would then expect a similar drop in Investor’s shareprice.

However, given that Investor is a seperately traded vehicle, we often see that the shareprice of Investor can fall more or less than the value of their holdings (NAV). From a starting point with no NAV discount, the short-term downside risk is more material, as investors may sell their Investor shares to a greater extent than the likes of ABB, Atlas and EQT in times of panic. Thus, leading to the NAV discount returning.

There’s nothing dramatic in this either, it’s just a result of trading a vehicle that has two layers of trading — the underlying stocks beneath it and the stock itself. This is different to buying a fund for instance, where the price of the fund is directly tied to the assets they own. It’s a distinction to be mindful of, especially if Investor trades at a large premium. As of today, Investor’s discount is at 1%.

Latour shareholders in 2021 still have scars from trading at a 50% premium to NAV in 2021. If that scenario occurs, a rational capital allocator would issue more of those expensive shares of their own currency, in order to make more attractive investments.

Conclusion

We still like Investor AB, their management team and their investment portfolio. At the same time, we acknowledge that today’s starting point is less attractive than it have been for the previous years (lower underlying multiple and NAV discount).

The bull case is simply that companies like ABB, SAAB and EQT’s strong current earnings momentum will drive the underlying profit figure more up and to the right.

Capital allocation is where we’re focused most right now. Investor AB recently increased its stake in EQT — and we’re preparing a writeup on them, out in July. Perhaps their alternative asset manager is an interesting opportunity currently?

Among other holding companies, MBB stands out to us. We’ve covered them several times before, and while their portfolio doesn’t match Investor’s business quality, management is more opportunistic and flexible with capital allocation. Combined with a much smaller starting base, a massive net cash pile, a steep discount to NAV, and an excellent track record, we think readers will find our MBB writeups worthwhile too.

Links to both below.

Similarly, both Constellation Software and Topicus have excellent track-records and trade at historically low valuation points. You can find our writeups of Topicus and it’s recently acquired stake in Asseco Poland below as well.